Image generated by Gemini

This roundup breaks down seven risk intelligence platforms built for banks and fintech companies. You’ll find comparisons on latency, pricing, and integration so you can pick the right fit for your fraud stack.

| Name | Photo | Pros | Cons | Pricing |

|---|---|---|---|---|

| Maptive |  |

|

|

Subscription-based (free trial) |

| Feedzai |  |

|

|

Quote-based |

| ThreatMetrix |  |

|

|

Quote-based |

| Quantexa |  |

|

|

Quote-based |

| Trustmi |  |

|

|

Quote-based |

| VALID Systems |  |

|

|

Quote-based |

| Eftsure |  |

|

|

Quote-based |

How Financial Fraud Is Changing (and What to Look For)

Digital fraud is evolving faster than most banks can keep up. Deepfakes, synthetic identities, and coordinated account takeovers pose new threats, and AI-driven theft could reach $40 billion in the US by 2027.

A Federal Reserve report highlights increased malicious activity across all payment channels. As a result, banks are replacing static systems with behavioral profiling, ending end-of-day transaction reviews.

Criminal operations now launch coordinated assaults across multiple accounts, devices, and identities simultaneously. Even JPMorgan Chase recently committed $14 million to next-generation anti-scam initiatives, a pretty clear sign that legacy systems can’t keep pace. Graph-based machine learning and adaptive data pipelines are now table stakes for identifying hidden relationships across IP addresses, geolocations, and transaction patterns.

So what should you actually look for when evaluating a platform? Here are the core criteria that separate strong fraud tools from outdated ones:

-

Behavioral AI and statistical fingerprinting: The platform should track how a user types, swipes, and navigates a digital application to spot anomalies in real time.

-

Spatial and geographic context: Can the system visually map and verify where transactions are physically occurring? That’s critical for catching cross-border account takeovers.

-

Real-time processing latency: Sub-second decisioning is non-negotiable if you want to freeze malicious ACH or wire transfers before funds settle.

-

Orchestration and integration: The tool needs to integrate with your core banking ecosystem, CRM, and payment gateways via REST APIs without a painful migration

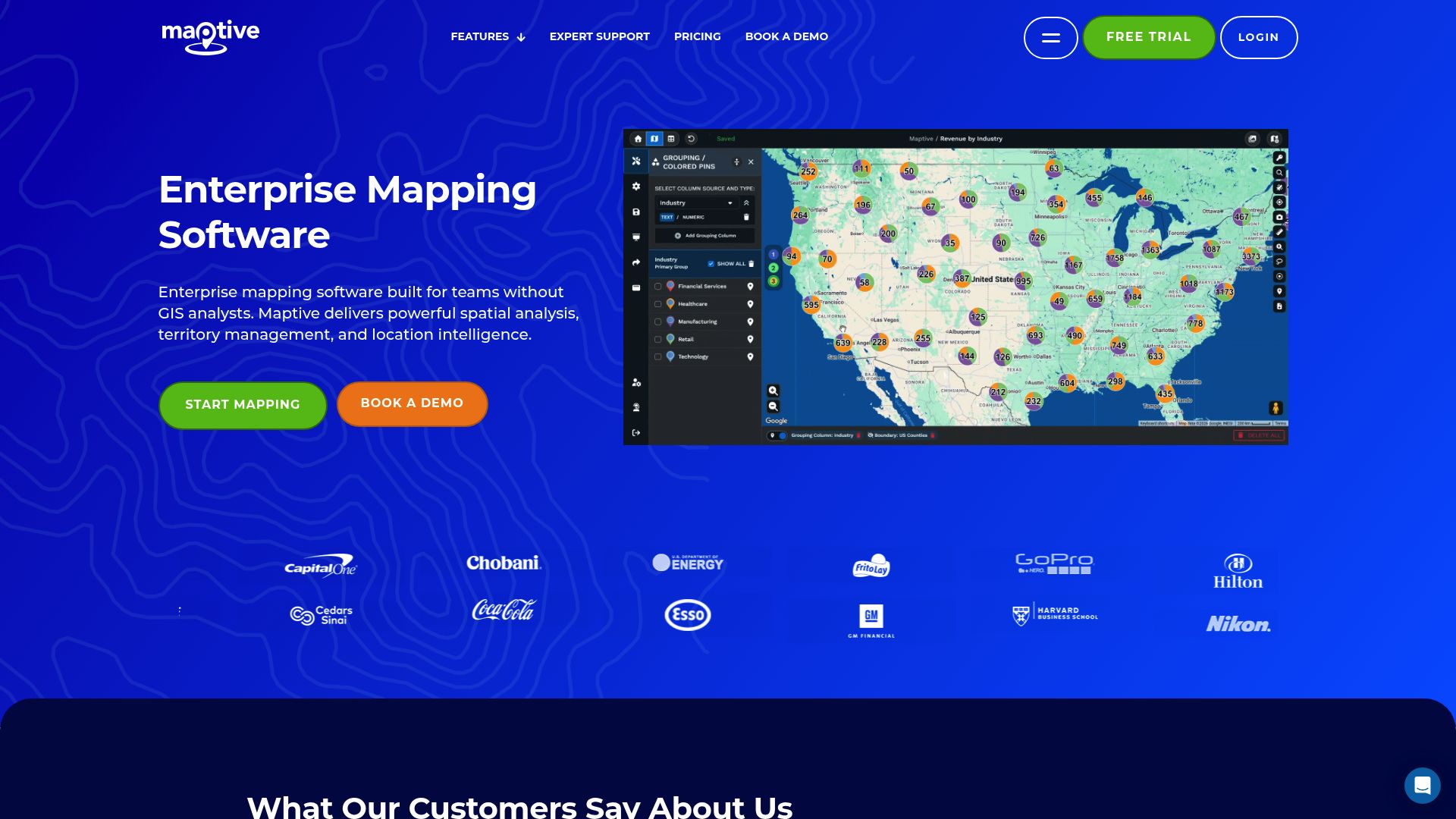

Maptive

Geographic context matters a lot when you’re trying to identify synthetic identities or organized crime rings running cross-border account takeovers. Using capable location intelligence software lets financial institutions turn massive arrays of transaction coordinates into interactive, visual maps. Built on Google’s enterprise mapping architecture, the platform helps risk management teams visualize complex spatial data without needing formal GIS training.

Advanced surveillance technologies integrated with spatial analytics can cut implementation costs while improving financial resilience. Investigators can visually spot clustering anomalies to flag organized strikes right away, making it much easier to intercept wire transfers coming from unexpected overseas servers.

On the performance side, the software handles enterprise-grade datasets of up to 100,000 markers per map without slowing down, thanks to WebGL-based rendering. Drive-time and radius analysis tools are particularly useful for neutralizing “impossible travel” scenarios, in which the system checks whether a cardholder could physically move between two transaction points within a given timeframe.

Endpoint intelligence platforms that offer continuous monitoring can pipe data directly into tools like this via real-time CRM integrations for faster threat response.

| Feature | Details |

|---|---|

| Primary use case | Spatial anomaly detection, geographic clustering, impossible travel verification |

| Key technologies | Google Maps enterprise framework, WebGL rendering, iQ automated analysis |

| Deployment and integration | Cloud-based SaaS, API connectivity, real-time CRM syncing (e.g., Salesforce) |

| Target audience | Fraud analysts, risk operations teams, compliance investigators |

| Pricing model | Tiered subscriptions (Individual, Team, Enterprise); free 10-day trial |

Feedzai

Feedzai runs a full-spectrum RiskOps Platform built for banks, fintechs, and payment processors. It unifies AI-driven anomaly detection, machine learning, and case management into a single ecosystem, replacing the patchwork of disconnected point solutions many institutions still rely on.

With median losses exceeding $2,300 per consumer incident, continuous risk assessment across the entire customer lifecycle is no longer optional. The platform intercepts unauthorized push payments, account takeovers, and money laundering attempts through real-time decisioning engines.

Transactions get evaluated against vast historical datasets, and anomalies are flagged milliseconds before funds move. Banks can stop criminals without piling friction onto the user experience. One of Feedzai’s standout capabilities is its explainable AI, which breaks down the math behind every flagged transaction, enabling compliance teams to demonstrate fairness and auditability.

About 83% of consumers want alerts to prevent suspicious transfers, so transparent and rapid AI interventions directly affect customer trust. The models learn continuously from new data to identify shifting criminal tactics; no manual rule changes needed. That automated adaptability lowers false positives while keeping legitimate transactions frictionless.

| Feature | Details |

|---|---|

| Primary use case | End-to-end RiskOps, payment protection, AML compliance |

| Key technologies | Adaptive machine learning, explainable AI, 360-degree customer profiling |

| Deployment and integration | Enterprise-scale cloud or hybrid; deep integration with core banking systems |

| Target audience | Retail/commercial banks, neobanks, payment processors, acquiring merchants |

| Pricing model | Custom enterprise quote-based pricing |

ThreatMetrix

ThreatMetrix, owned by LexisNexis Risk Solutions, is a digital identity and risk decisioning engine that draws on a massive global network. It analyzes billions of transactions across industries to build persistent, reliable digital identities. Unauthorized-party attacks now account for 71% of incidents and losses, underscoring the need for deep intelligence on devices, IP addresses, and user behavior to stop account takeovers.

Because bad actors constantly rotate their tactics, ThreatMetrix acts as an early warning system for large banking enterprises. The system classifies transactions using Open Smart Learning models, catching compromised credentials before they breach the banking perimeter. Security teams use these instant risk assessments to separate legitimate customers from scam activity.

The interpretable ML layer uses SHAP-based model explainability, so analysts can see exactly why a transaction got a specific risk score. Trusted users sail through with seamless approval; suspicious ones get a step-up authentication challenge. Identity-centric security strategies using layered, adaptive defenses are now a must to counter deepfakes and automated phishing targeting high-value payments. By verifying the genuine identity behind the screen in milliseconds, ThreatMetrix makes stolen credentials and mule networks far less viable.

| Feature | Details |

|---|---|

| Primary use case | Account takeover prevention, scam detection, new account origination risk |

| Key technologies | Global Digital Identity Network, Open Smart Learning, SHAP-based explainability |

| Deployment and integration | Cloud-based decisioning with client-side web and mobile SDKs/APIs |

| Target audience | Global banks, Fortune 500 enterprises, digital-native financial platforms |

| Pricing model | Quote-based, tailored to transaction volume and geographic scope |

Quantexa

Quantexa’s Contextual Decision Intelligence platform is purpose-built for the enormous data environments inside top-tier banks and global insurers. It ingests massive volumes of fragmented internal and external data to perform enterprise-scale entity resolution (essentially connecting records that belong to the same person or organization, even when the data doesn’t match perfectly). Digital attacks surged 86% in some regions recently, exposing just how limited legacy rule-based systems really are.

Quantexa connects the dots between seemingly unrelated accounts, shell companies, and devices to generate contextual network graphs. Investigators use these visual relationship maps to unmask complex money laundering rings designed to slip under standard monitoring thresholds. It’s the kind of big-picture view that siloed point solutions consistently miss.

Traditional rules-based setups also generate mountains of false positives, which drain analyst time and delay legitimate transactions. Quantexa tackles this with highly contextualized risk scoring that surfaces real threats instead of noise. Privacy-preserving AI systems combining federated learning and ensemble ML are becoming necessary as banks navigate strict global data regulations.

Quantexa supports these environments with strong data governance, controlled access, and audit capabilities tailored to each deployment setup. Banking clients regularly report major reductions in false positives and a noticeable increase in operational efficiency across their compliance teams.

| Feature | Details |

|---|---|

| Primary use case | Complex AML investigations, KYC/CDD compliance, organized threat ring detection |

| Key technologies | Advanced entity resolution, contextual network graphing, scalable data ingestion |

| Deployment and integration | Flexible (on-premise, private/public cloud, hybrid); robust API connectors |

| Target audience | Tier-1 and Tier-2 banks, government agencies, major insurance providers |

Trustmi

Trustmi zeroes in on a specific pain point: the vulnerabilities lurking in the procure-to-pay lifecycle. Its behavioral AI model correlates signals across ERP platforms, email servers, vendor databases, and banking networks. Business email compromise and credit-push schemes led to an estimated $8.5 billion in losses between 2022 and 2024. That’s a massive blind spot for most organizations.

Trustmi addresses it by deploying an anonymized database of historic payment patterns to validate routing and account data. If a bad actor intercepts an invoice and alters the banking details, pre-payment checks flag the anomaly before any funds leave the building. Vendor impersonation attempts fail without anyone in accounts payable needing to lift a finger.

Integration into existing AP workflows via the API takes roughly 2 weeks and doesn’t disrupt daily operations. Trustmi has helped secure over $200 billion in payment volume globally with virtually zero false positives.

The rise of real-time payments has made funds recovery almost impossible, so preemptive validation of vendor banking details is no longer a luxury. The platform also analyzes documents for tampering and assigns color-coded risk levels that non-technical finance users can actually understand.

| Feature | Details |

|---|---|

| Primary use case | Business email compromise (BEC), vendor impersonation, AP payment errors |

| Key technologies | Behavioral AI baselining, crowdsourced trust network, document tampering detection |

| Deployment and integration | Fast 2-week SaaS API deployment with existing ERP/finance systems |

| Target audience | Enterprise finance teams, accounts payable, treasury, controllers |

| Pricing model | Custom volume-based pricing tied to total spend processed |

VALID Systems

Check fraud might sound old-school, but it’s still a multi-billion-dollar problem. VALID Systems tackles it head-on with an AI-powered platform for account risk and transaction decisioning. The software delivers sub-second evaluations of check deposits across mobile, ATM, and teller channels. Nearly half of the institutions surveyed saw fraud-related losses climb recently, fueling a rush toward AI that automates first-party threat detection.

VALID analyzes a triad of data points: payer history, depositor behavior, and the established relationship between both parties. That behavioral and transactional approach prevents heavy losses tied to remote deposit capture and fraudulent check rings. Risk teams can confidently block suspicious deposits without slowing down legitimate customers.

The InstantFUNDS module accelerates up to 99 percent of deposit approvals while actively guaranteeing covered losses on approved items. Processing over $4 trillion in check volume annually, VALID has built a massive intelligence network to train its ML models.

Anti-theft systems now use statistical fingerprinting of user behavior, reducing false positives and unnecessary account friction. VALID also offers native deployment inside the Snowflake AI Data Cloud, so banks can run advanced decisioning containers without the headache of traditional data migration.

| Feature | Details |

|---|---|

| Primary use case | Real-time check screening, deposit acceleration, liquidity management |

| Key technologies | Sub-second ML decisioning, CheckDetect, InstantFUNDS charge-off guarantees |

| Deployment and integration | Native Snowflake deployment, direct ATM/teller/mobile API integrations |

| Target audience | Retail banks, credit unions, large financial service providers |

| Pricing model | Quote-based, tailored by transaction volume and scope of risk guarantees |

Eftsure

Eftsure is a continuous controls monitoring SaaS platform built to help eliminate B2B payment threats and corporate financial risk. What sets it apart is its continuous supplier master data screening, which perpetually validates payee details against an independently verified database. In recent years, banking and financial institutions have experienced a significant surge in cyber-driven impersonation schemes targeting business-to-business vendor management systems.

Eftsure acts as a prepayment checkpoint, validating payment files exported from an institution’s ERP system before the final payment run. Visual indicators flag the confidence level of each bank account match right inside the web dashboard. That immediate feedback stops funds from bleeding into unauthorized offshore accounts by prompting manual review of high-risk payees.

On the compliance side, the platform maintains a thorough audit trail of all verification events, permanently replacing the risk associated with static, manual spreadsheet controls. It also monitors supplier master data around the clock, triggering alerts and re-verification workflows whenever account details change.

New industry rules require financial institutions to be far more vigilant about accounts receiving funds, placing a heavy compliance burden on corporate treasury teams. Eftsure provides verifiable evidence of controls over changes to supplier bank details, which goes a long way toward satisfying external audit requirements. It integrates with existing finance systems and serves mid-market to large-enterprise CFOs handling high volumes of complex vendor payments.

| Feature | Details |

|---|---|

| Primary use case | Continuous supplier master data screening, erroneous payment prevention, AP controls |

| Key technologies | Independent networked database matching, real-time file validation, visual confidence indicators |

| Deployment and integration | SaaS with API or file-based interfaces connecting to core ERP/finance systems |

| Target audience | Mid-market to large enterprise CFOs, financial controllers, treasury teams |

| Pricing model | Sales-led custom quote |