The financial sector is undergoing a profound transformation driven by rapid data growth, evolving regulatory frameworks, and the adoption of artificial intelligence in risk management. Financial institutions are rethinking how they collect, store, and analyze massive, heterogeneous datasets to enable real-time, compliant, and explainable credit-risk decisions.

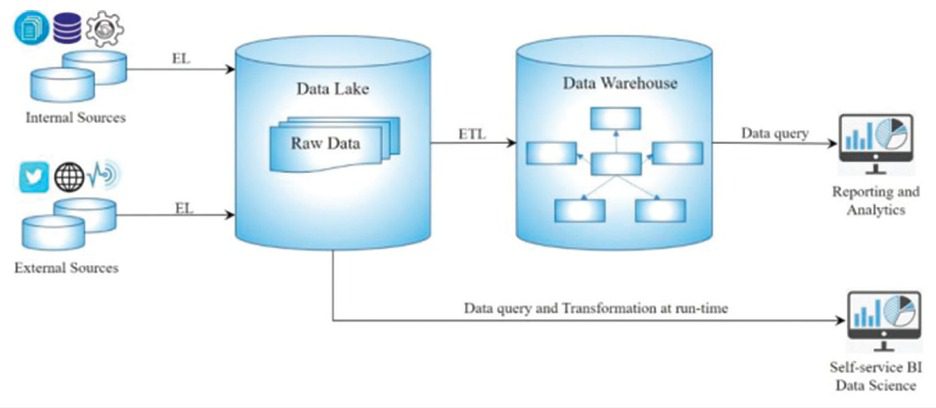

Traditional data warehouses, once the backbone of analytics, now struggle with the scale and velocity of modern data. In this context, Pushpalika Chatterjee’s 2019 research on the Intelligent Enterprise Data Lake Framework (IEDLF) presented a timely architectural vision that redefined how financial data could be unified, governed, and analyzed for risk prediction and compliance reporting.

The IEDLF introduced a flexible, cloud-native, and metadata-governed architecture capable of integrating data from credit bureaus, core banking APIs, and alternative digital sources, using schema-on-read principles. By 2021, several leading financial institutions and consulting firms had begun applying similar data-lake strategies to enhance transparency, scalability, and regulatory alignment.

The Shift Toward Data-Driven Modernization

Between 2019 and 2021, financial modernization rapidly accelerated. Consulting leaders like Deloitte and Accenture reported significant investments in data-lake modernization programs across the banking sector, combining compliance, customer analytics, and risk modeling into unified ecosystems.

Cloud providers soon followed with frameworks directly reflecting IEDLF concepts. AWS’s Financial Services Data Lake Reference Architecture and Google Cloud’s Risk Analytics Blueprint showcased layered ingestion, governance, and AI-readiness, mirroring the IEDLF’s modular approach.

The industry’s convergence around these principles confirmed that data lakes had matured from research concepts into the operational foundation for financial intelligence—supporting everything from Basel III reporting to real-time fraud detection.

Architectural Innovation and AI Integration

The Intelligent Enterprise Data Lake Framework proposed in Chatterjee’s research emphasized a multi-layered structure integrating ingestion, validation, storage, and consumption layers, orchestrated through Apache Kafka, Spark, and Airflow pipelines.

This design anticipated the rise of AI-powered data fabrics, where streaming and batch pipelines coexist to serve both regulatory reporting and predictive modeling. Institutions soon began adopting this hybrid approach—merging credit-scoring systems with anomaly-detection models, all trained on unified, versioned datasets.

By 2021, this architecture evolved into the Lakehouse paradigm, combining the scalability of data lakes with the governance and transactional capabilities of data warehouses. The transition marked a pivotal step in transforming legacy banking systems into AI-driven, cloud-native ecosystems.

Governance, Transparency, and Regulatory Confidence

A key innovation in the IEDLF was its metadata-driven governance model, designed to meet financial regulations such as Basel III, CECL, and IFRS 9. The framework embedded data lineage, auditability, and validation as integral architectural features rather than afterthoughts.

This approach directly aligned with the growing emphasis on explainable AI (XAI) and model transparency in financial regulation. The same governance philosophy is now visible in enterprise-grade tools like Apache Atlas, AWS Glue Catalog, and Great Expectations, which provide automated lineage tracking and quality scoring—concepts central to Chatterjee’s original framework.

The IEDLF thus anticipated an essential requirement of modern AI governance: ensuring not just performance, but accountability in financial decision-making.

Real-Time Risk Intelligence: From Theory to Implementation

One of the most impactful features of the IEDLF was its focus on real-time intelligence. By integrating event-driven ingestion (Kafka/NiFi) with real-time processing (Spark/Dataproc), the framework enabled continuous monitoring of borrower activity and credit exposure.

Industry adoption soon followed. In 2021, HSBC’s Counterparty Credit Risk (XVA) Platform, built in collaboration with Google Cloud, achieved a tenfold improvement in performance using streaming pipelines—an implementation that mirrored the IEDLF’s emphasis on hybrid ingestion and distributed analytics.

Similarly, Capital One migrated its credit-risk analytics to an AWS-based data-lake architecture, leveraging schema-on-read ingestion and Spark processing. These examples demonstrate how the architectural foundations proposed in the 2019 paper became cornerstones of real-world financial modernization efforts.

Industry Adoption and the Lakehouse Transition

By 2021, the industry consensus was clear: cloud-native, governed data lakes were the future of financial analytics. European banks such as ING and BBVA began adopting Delta Lake and Apache Iceberg to unify compliance-grade governance with scalable data management.

These institutions demonstrated how combining open-source technologies with structured metadata models can achieve both transparency and real-time performance—core goals of the IEDLF. The convergence between academic theory and operational deployment reinforced the framework’s foresight and industry relevance.

Conclusion: The Enduring Foundation for Financial AI

The Intelligent Enterprise Data Lake Framework has matured from a pioneering academic concept into a widely adopted industry practice. Financial institutions across the world have embraced the key principles identified in Chatterjee’s research—real-time ingestion, layered governance, schema-on-read processing, and AI-driven credit analytics.

As technological ecosystems continue to evolve with Lakehouse architectures and federated AI, the foundational blueprint of the IEDLF remains firmly relevant. Intelligent data lakes now function as the operational and analytical core of modern financial systems, enabling secure, transparent, and scalable credit-risk management.

This sustained alignment between academic research and industry execution illustrates how forward-thinking scholarship can anticipate, influence, and guide large-scale digital transformation in the financial sector.