Russia’s invasion of Ukraine has sent oil prices soaring. International oil prices, measured by Brent Crude, and domestic prices, measured by U.S. West Texas Intermediate futures are both at their highest levels since 2008. Stock markets, meanwhile, have slumped, with tech stocks especially hit hard this year. Oil price inflation predates Russia’s invasion, with prices rising sharply since the end of the first lockdown. Investors have to adapt their portfolios for this new era.

Has This Happened Before?

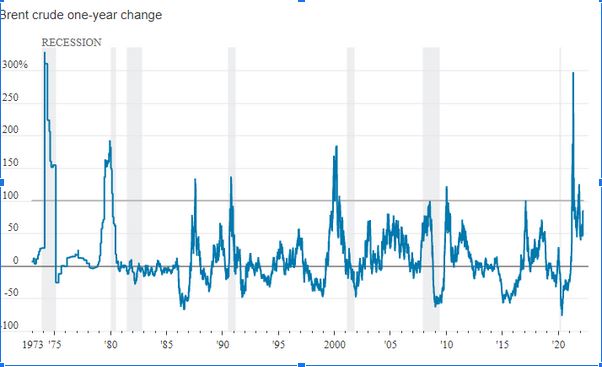

Yes, oil prices have doubled or more within a year. In 1974, 1980 and 2001, this was due to a recession. In1990 and 2008, a recession had just started. Today, prices are rising due to an embargo on Russian exports.

Source: Wall Street Journal

Indeed, there have been recessions after all three of the last commodity booms, in 1973, 1979 and 2007.

How Has the Market Reacted?

The market has been trending downward since the start of the year.

Source: Wall Street Journal

Investors are worried that the oil embargo will affect the global supply of oil, and that this will affect global growth and accelerate inflation.

We have had a year of financial market volatility, oil supply shocks, rising inflation, and declining earnings for businesses such as Facebook.

What Do Economists Think?

Economists such as Nouriel Roubini have long argued that the risks of stagflation are high and that the supply-side shocks and geopolitical risks in the environment are greater than many people think. Added to that, German economist Hans Gersbach believes that bank regulation has created inflationary pressures that are widely not recognised.

Those voices that have warned about geopolitical risks and long-standing supply-side shocks have been most correct about the direction of the world economy.

What Does This Mean for the Stock Market?

We have already seen market declines since the beginning of the year. That downturn sharpened when Russia invaded Ukraine. Rising inflation tends to lead to a rotation away from stocks and into commodities. Investors in commodities futures and in some -not all- commodities businesses, will outperform the stock market as a whole.

The market could not keep going up, as much as people kept saying that “this time is different”. Even with these shocks, the S&P 500 had risen to historic highs. The higher it rose, the lower were future returns. At some point, investors would have to rotate away from stocks because there were no gains left.

The present crisis has simply brought us to the point where stock markets were heading anyway. Given the recessionary outlook of the market, it is doubtful that there is much upside in the market at the moment.

Ultimately, owning stocks makes you a fractional owner of a business. Many businesses are under pressure. Businesses with exposure to Russia have suffered due to sanctions. Businesses that consume a lot of oil now face rising oil prices. Consumers have to spend more just to get the same amount of heating, oil and gas as they have enjoyed before Bradington Young.

How the market looks in the next few months depends a lot on how the Federal Reserve reacts to this crisis.

What Will the Fed Do?

If commodities continue to appreciate in price, the Fed is expected to raise interest rates. However, it’s not as simple as that: prices may rise so high that the Fed decides that it’s not such a great idea to raise borrowing costs as well, or at least as aggressively as they at first telegraphed.

The way that things are unfolding in Ukraine, and the challenges that Europe will have in finding alternatives to Russian oil, it’s a good chance that the Fed will decide not to raise interest rates by as much as many analysts predicted. Analysts had believed that rates would go up by 175 basis points.

The reason the Fed might decide not to raise interest rates aggressively is that raising interest rates would make it more expensive to borrow funds to invest in the stock market. That could lead to demand for stocks declining, pushing the market down.

To make things more difficult: demand destruction could occur, in which demand falls as a result of rising prices, which in turn would force prices down. However, oil is still the basis of so much of our lives that it is difficult to imagine much demand destruction happening.

On the plus side, Americans have more money saved than during past crises and the employment rate remains good. That could reduce the odds of a recession.

So What’s the Bottom Line?

Investors with a well-diversified portfolio don;t need to do anything. There’s a lot of change happening and uncertainty is high, so investors would probably make a mistake trying to adjust for conditions.

Investors who want to buy energy stocks, for instance, should be aware that many energy stocks have already started to have rather frothy valuations. Firms such as Texas Pacific Land Corporation remain cheaply valued with lots of great qualities and limited risk.

Timing the market is impossible. If you are well-diversified, sit tight. If your comfort level has been breached, then sell to a level that’s comfortable for you, without affecting the composition of your portfolio.