Umbrella insurance is another personal liability insurance that can pay claims over your regular insurance policy limits.

If you ever find yourself in a lawsuit that costs more than your insurance can spend, you can lose all the savings.

How can you avoid it with umbrella insurance? Below, we’ll describe the step-by-step action plan for umbrella insurance.

You’ll find how different it is from excess liability insurance, plus many limits on the liability coverage that umbrella insurance has.

How Does It Work?

Umbrella insurance can also cover you for incidents homeowners insurance cannot, such as a defamation or slander lawsuit.

Members of your household — such as your spouse and children — are also generally covered by your umbrella insurance policy.

Here’s the list of situations when umbrella insurance may come in handy:

- Your son punches his classmate at school, and his parents want to sue you

- You’re the reason for the 10-car accident, and your automobile insurance will not cover all the costs for the victims

- Your teenage kid throws a party at home, and some guests bring alcohol and get arrested for driving under the influence

And many more cases where umbrella insurance is your lucky chance to avoid the negative consequences. It is a life vest to keep you on track in topics that homeowners or auto insurance cannot cover.

Of course, one of the most accessible financial solutions is finding some cash advance apps for android or iOS: but admit it, when the stakes are high, you won’t solve everything with a loan.

The Price

If you are wondering how much the umbrella insurance costs, the price will strictly depend on the coverage you purchase, the state of your residency, and the risks the insurer takes when signing your application.

You may lose your assets in case somebody files a lawsuit for you. Let’s say the accident happened on your property or anyone else has operated your vehicle.

Personal umbrella and excess insurance policies demand that you maintain “underlying insurance” for your car, house, boat, or off-road recreational vehicle, all specified on the umbrella policy’s declarations page.

The other fact is that the personal umbrella and excess liability plans sometimes offer coverage beyond that of “underlying insurance.

There may be no minimum underlying coverage needed for coverage above that provided by “underlying insurance”; however, there may be a deductible.

How much coverage you decide to purchase will influence the price of umbrella insurance.

Other elements, including your location, the number of cars you own, and other things, may affect the cost of your umbrella insurance.

What Can You Cover?

Umbrella insurance pays for the damages caused by your property up to the liability limit and the associated legal costs.

For example, if your umbrella policy covers up to $1 million of damage, the insurer will pay this amount on top of the fees for legal defense.

The examples of costs an umbrella insurance covers:

- The price of others’ medical care and burial expenses

- Harm to others’ property

- Slander, libel, defamation of character, and other types of personal assault lawsuits

- Your expense for defense counsel

- If you’re a landlord, your tenant’s injuries or property damage

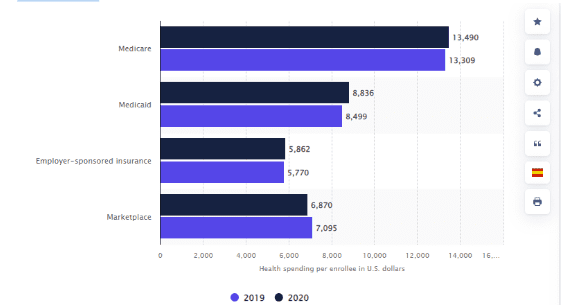

Statistics say Americans’ health spending had increased since 2019 when it was 13,309 U.S. dollars. The following year, the average amount spent per Medicare enrollee counted to 13,490 U.S. dollars.

Health spending per enrollee in the United States in 2019 and 2020 by insurance

Link: https://www.statista.com/statistics/246913/health-spending-per-enrollee-in-the-united-states/

What Can You Not Cover?

First and foremost, umbrella insurance won’t cover your injuries or property damage.

Unless you filed for commercial umbrella coverage instead of taking a personal offer: in this case, the liabilities associated with your business will be covered.

Here are what else you cannot pay for using the umbrella insurance:

- Your injuries

- Your property damage

- Accidents or damage to property for your company is liable for Intentional or criminal activities.

- Intentional or criminal acts

- Contract-related liability that you are responsible for

Most umbrella insurance plans don’t cover responsibility resulting from you intentionally violating the contract agreement.

Your umbrella insurance coverage is unlikely to be of assistance in case a roofing business sues you for failing to pay for the work performed by the contract you signed. Plus, you won’t get coverage if you hurt someone on purpose.

The Insurance Size You Need

You should have at least enough liability insurance to protect your assets. To come up with the “enough” amount, add up the value of your property, savings, and investment accounts.

There are factors to consider while choosing the appropriate level of coverage.

- Asset value: umbrella insurance should at least cover your net worth because that is often how much you stand to lose in a lawsuit.

- Potential loss of future revenue: a significant lawsuit may jeopardize your future income. Consider your prospective future income even if your current income is restricted.

Remember that the federal Employee Retirement Income Security Act of 1974 shields employer-sponsored retirement funds, such as 401(k)s, from most lawsuits. Except for money transferred from an employer-sponsored account, IRAs are not.

However, state legislation may partially protect your IRA funds and the equity you hold in your house. Before determining how much umbrella insurance you require, check your local legislation.

Insurers often sell umbrella insurance in million-dollar blocks. This implies that the cheapest insurance on the market offers $1 million in coverage, the next-cheapest policy provides $2 million in scope, and so on. As a result, regardless of the policy you buy, you get a respectable level of coverage.

Summing Up

A personal responsibility case can leave even the most diligent party, with the greatest of intentions, on the line for a sizable settlement.

Even if it’s improbable that you’ll ever find yourself in this circumstance, it’s wise to try to prevent a severe financial loss. That’s where you may use umbrella insurance.