Do you like to do a lot of your financial planning and investing yourself? Or maybe you are fed up with high financial advisor fees and only need a little bit of help with financial planning and investing. Like millions of others, if you fit this category you are looking online for retirement planning software.

So many people are starting to take their financial futures into their own hands especially when it comes to retirement planning. Others know a bit about investing but still want a professional’s help to determine what their asset allocation should be, what their risk level should be, what types of funds they should be looking at, and how they can minimize taxes in retirement.

Web-Based Retirement Planning On Your Own

Although robo-advisors get most of the press these days when it comes to big changes in financial technology for consumers, there is also a revolution in retirement planning for those who want to be empowered to run their own retirement projections and scenarios. Two of the more modern software applications for financial and retirement planning come from WealthTrace and Personal Capital. Let’s compare and contrast these two financial applications.

Accurate Retirement Projections

A big problem with free web-based retirement calculators over the years has been their lack of accuracy. The adage “you get what you pay for” is almost always true and there is no exception here. Free retirement calculators lack the ability to vary tax rates over time, calculate taxes correctly each year, project Required Minimum Distributions (RMDs), or allow for users to change important assumptions such as investment rates of return and inflation. Also, many of the assumptions are hidden and the users have no idea what assumptions and settings are being used.

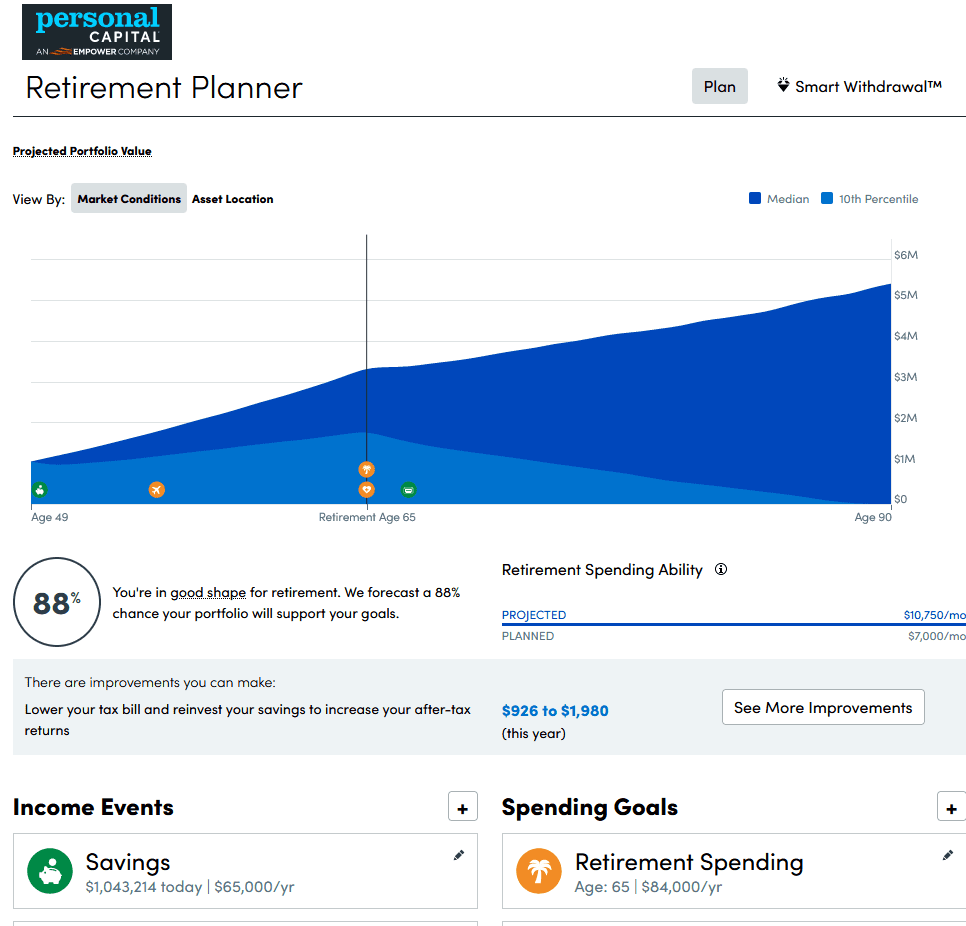

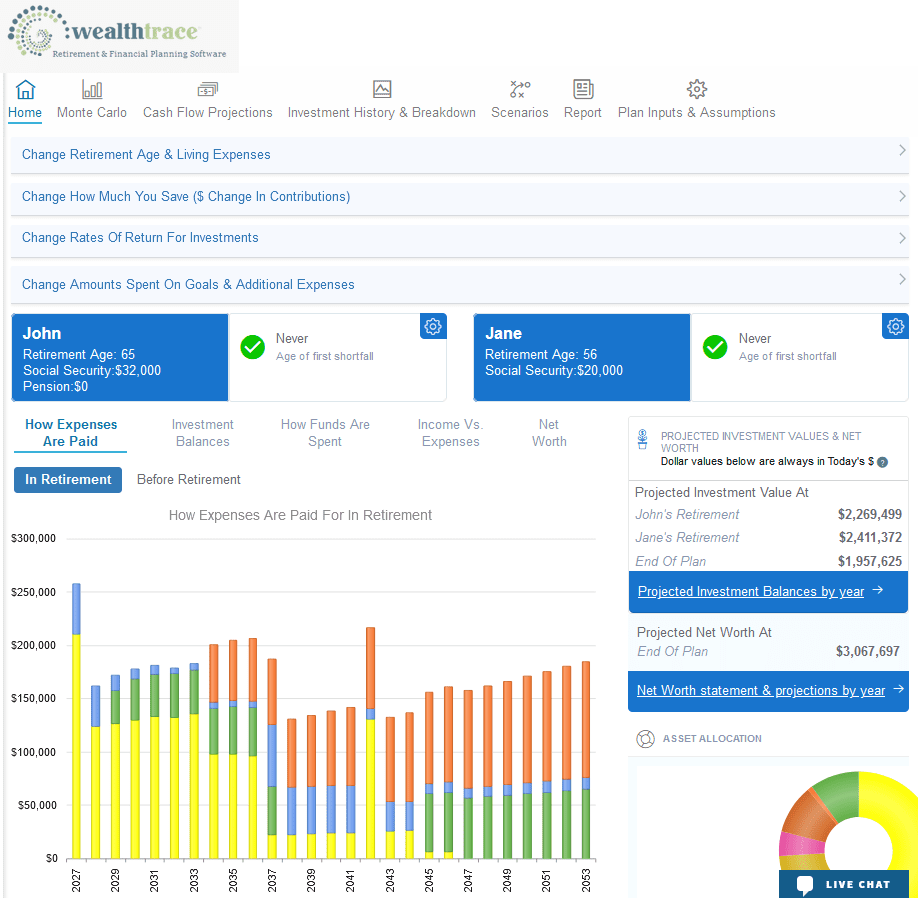

Around the same time about ten years ago, WealthTrace and Personal Capital saw a need and they filled it. They both presented easy to use retirement planning to consumers with easy to understand interfaces and the ability to change many assumptions. They both have complex Monte Carlo simulations which tells the user the probability of never running out of money.

But Personal Capital was built mainly to track investments with retirement planning as a secondary offering. Because of this, they left out many of the detailed settings and assumptions that WealthTrace offers. For example, in Personal Capital you cannot change your life expectancy or investment return assumptions. You cannot specify how much you save to each investment account and they do not recalculate federal tax rates each year in their projections. You also cannot tell the software that you plan on reallocating to a more conservative investment mix when you retire. WealthTrace allows for all of this.

Linking Accounts

Both software packages allow users to link their investment accounts, which is such a wonderful feature because the balances and account holdings update every day from nearly any bank or broker in the world. Both use a third party, Yodlee, to do this. This also allows both platforms to pull in information on the asset classes the user is invested in so they can manage their asset allocation.

Personal Capital allows users to link mortgages and credit cards as well, but WealthTrace does not have this capability.

Tracking Performance

Using historical data from linked investment accounts, both WealthTrace and Personal Capital show account performance over various time frames. But WealthTrace also utilizes the power of Morningstar’s data to show historical performance for mutual funds and ETFs. You can compare the historical performance of any fund or ETF that exists to see how they stack up against each other. This is a great tool for those who are having trouble deciding which fund to select in their 401(k) plan, IRA, or taxable brokerage accounts.

Historical Data

Both platforms allow you to view all historical transactions for your bank and brokerage accounts. This is so useful for those who have multiple accounts across different platforms. Now you can view your transactions for everything in one place. Search for deposits, withdrawals, dividend payments, and trading transactions easily for any account.

Fund Fees

Both Personal Capital and WealthTrace allow users to view the fees they pay on any mutual fund or ETF and sort by the highest fee fund. This allows their users to quickly find out which funds are costing them the most money and most assuredly leads many investors to sell high fee funds and purchase lower-cost funds, thus saving potentially thousands of dollars over time.

What-If Scenarios

The real go-getters when it comes to retirement planning love running what-if scenarios. Unfortunately for Personal Capital users, there aren’t many scenarios beyond very simple changes to spending that can be done. But WealthTrace prides itself on its powerful scenario capabilities.

In WealthTrace you can quickly combine complex scenarios into one, such as inflation increasing while your taxes go up at the same time. Run a scenario where you retire earlier, move to a different state, and spend more on travel. Even more impressive is the ability to run Roth Conversion scenarios. You can home in on the best combination of how much to convert, when to start, and when to end the Roth conversion. WealthTrace shows you how much more or less you will pay in taxes along with which scenario provides the most money at the end of the plan and the best Monte Carlo result.

A New Era

Financial technology has come a long way in the last ten years. There are so many applications now that help people manage their finances, including tracking investments and budgeting. But when it comes to financial and retirement planning, WealthTrace and Personal Capital are two of the better ones you will find.