Starting a business is an exciting endeavor, but it’s important to understand the different business structures available before diving in. Choosing the right structure can significantly affect your business’s operations, taxes, and liability. Christopher Linton, Alabama industry expert, breaks down the various business structures to help entrepreneurs make informed decisions.

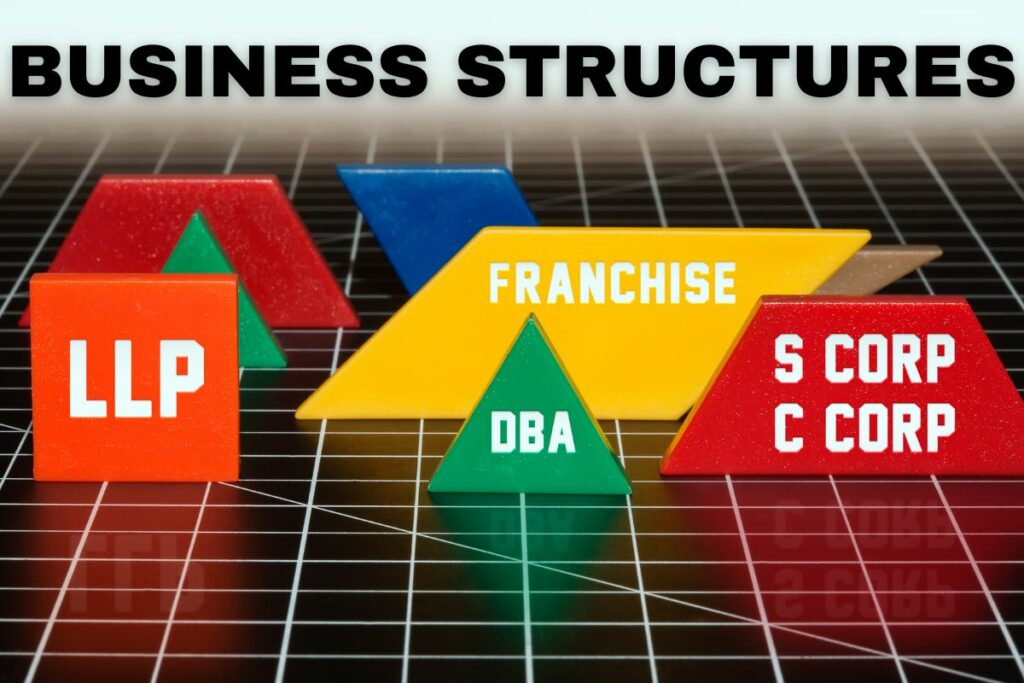

Sole Proprietorship

A sole proprietorship is the simplest and most common type of business structure. If you’re a one-person show, this might be the route for you. As a sole proprietor, you and your business are one entity. You have complete control over decision-making but are also personally responsible for any debts or liabilities the business incurs.

One of the key advantages of a sole proprietorship is its simplicity. You don’t need to file any special paperwork to get started. However, remember that your business income is considered personal income, which means you’ll report it on your personal tax return.

Partnership

Partnerships are like sole proprietorships but for multiple people. There are two main types of partnerships: general partnerships and limited partnerships.

In a general partnership, all partners share equal responsibility for the business’s operations and liabilities. This means that each partner is personally liable for the partnership’s debts. Communication and trust are crucial in a general partnership to ensure everyone is on the same page.

Limited partnerships (LPs) have both general partners and limited partners. General partners operate the business and are personally liable, while limited partners are investors with limited liability; they aren’t involved in day-to-day operations. This can be a good option if you have investors who want to support your business without taking an active role.

Limited Liability Company (LLC)

A limited liability company, or LLC, blends the liability protection of a corporation with the simplicity of a sole proprietorship or partnership. Your personal assets are generally protected from the company’s debts and liabilities. In an LLC, you’re referred to as a “member.”

One significant benefit of an LLC is its flexibility in terms of taxation. You can choose to be taxed as a sole proprietorship, partnership, S corporation, or even a C corporation. This flexibility allows you to select the best option for your financial goals.

Corporation

A corporation is a separate legal entity from its owners, known as shareholders. This separation means that shareholders’ personal assets are protected from the corporation’s liabilities. There are two main types of corporations: S corporations and C corporations.

An S corporation is a unique tax status that allows the company’s income to “pass through” to shareholders. This means the company itself isn’t taxed; instead, shareholders report the company’s income on their individual tax returns. However, not all businesses are eligible for S corporation status, and specific requirements exist.

C corporations, on the other hand, are subject to double taxation. This means that the corporation’s income is taxed at the corporate level, and then any dividends distributed to shareholders are taxed again on their individual tax returns. Despite this potential drawback, C corporations offer more flexibility in ownership and structure, making them a common choice for larger businesses.

Cooperative

A cooperative, or co-op, is a unique business structure owned and operated by its members. These members could be customers, employees, or even producers. A cooperative’s primary goal is to serve its members’ needs rather than generating profits for external shareholders.

Cooperatives can take various forms, including consumer cooperatives (owned by customers), worker cooperatives (owned by employees), and producer cooperatives (owned by producers of goods or services). In a cooperative, decision-making is often democratic, with each member having a say in the business’s operations.

Choosing The Right Structure For Your Business

Selecting the right business structure is crucial. It influences your legal responsibilities, taxation, and how you operate. Here are steps to help you make the right choice:

First, assess your business. Size, ownership, and growth plans guide your choice. Local ventures might opt for sole proprietorships, while tech startups lean toward LLCs or corporations.

Next, consider liability protection and tax implications. Protect personal assets with structures like corporations and LLCs, offering limited liability—account for varying tax implications at federal and state levels, seeking guidance from accountants.

Lastly, decide on your involvement in operations and choices. Are you inclined to take a hands-on approach, or are you comfortable sharing the responsibilities of key choices with partners or shareholders? This contemplation holds significance as your level of participation can significantly influence the most suitable business structure for your venture. Moreover, considering your long-term aspirations is crucial. Corporations are for investor funding, while LLCs are for flexible management.

Final Thoughts

Christopher Linton, Alabama, says understanding business structures is crucial in building a successful enterprise. Each structure has benefits and drawbacks, impacting your liability, taxation, and overall operations. By assessing your business needs and seeking expert advice, you can make an informed decision that sets the stage for your business’s growth and prosperity. Remember, choosing the right structure now can save you headaches.