This article is prepared by HES Fintech, a financial technology company that provides banks and fintech with comprehensive lending software.

People share the same social milestones over the course of their lives: they graduate from school, get a job, start a family, etc. Although these steps are somewhat similar for the majority of the population, the lifetime journey differs with each new generation. The 21st century is all about technology. It’s in the core of formative ideas of our times, and we get used to it since kindergarten.

Despite technology’s abundance, there’s a huge difference in the way Gen Z’s, Millennials, and Baby Boomers adopt it. When it comes to finance, this very difference influences the banking activities of younger generations in a lot of ways. In the modern era, when the CEO of a multi-billion company can smoke pot while discussing the colonization of Mars, Millennials are leaving traditional brick-and-mortar banks for new banking options. What Millenials want is less bureaucracy and more convenience. In a nutshell, they look for businesses that speak to their image and values.

Besides, there’s a lot of skepticism towards traditional banking. In light of the 2008 crisis, banks have severe issues with trustability. According to a WEF’s Global Shapers survey, only 45% of respondents said that they trust banks. The number is even lower for the younger generation: only 28% out of the more than 30,000 Millennials believe in banks’ “fairness”. Mike Mayo, Wells Fargo’s head of U.S. large-cap bank research, sums it up in an honest one-liner: “The financial crisis was terrible for the industry’s reputation of trust.”

The industry had to drastically enhance customer experience, and this atmosphere of change created space for players willing to reshape consumer finance. This means that traditional institutions are facing fintech competitors who are on the same page as the younger generations.

New Kids on the Block

The domain of lending services is no stranger to changes, and the emergence of alternative lenders is a direct result of the global financial crisis’ aftermath. After the collapse, the majority of banks became very prudent in providing loans and their requirements became too stringent. Increased regulations and capital requirements made small consumer lending less profitable for banks. Even clients with a good credit history are denied loans without explanation. But who’s going to take care of the 1.7 billion underbanked adults around the world?

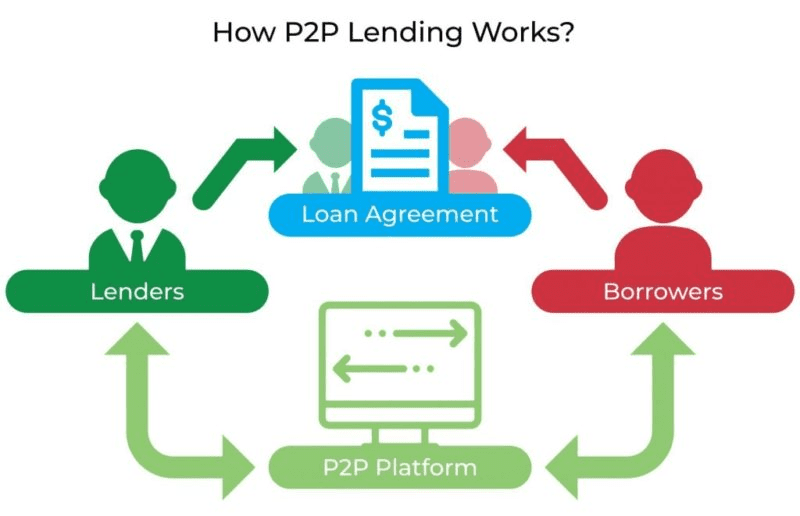

Holes in the market are not necessarily empty. Enter peer-to-peer lending, also known as social lending or crowdlending. The backbone of the business is a peer-to-peer platform that provides direct interaction between borrowers and investors without going through multiple accounts. In comparison with traditional banking, new players offer quicker loan approval times and faster funding.

(Source)

P2P lending solutions show great potential for growth. A good example: back in 2007, Lending Club, a well-known American platform, hardly attracted $10 million of investment. Following their IPO in 2014, the company’s capitalization increased to $10 billion. As for now, the P2P sector offers attractive business opportunities. Aspiring lenders don’t need substantial capital to get into the sector, not to mention that the regulations are softer in comparison with high street banking.

It is estimated that in the US alone 38% of consumer loans are issued by fintech startups. P2P lending is growing globally at the speed of light. According to Mintos, the global P2P lending market is projected to reach $897.85 billion by 2024. Something that started as an underground (and sometimes marginal) alternative to high street banks has become an established option for the masses.

Sometimes It Hurts

However, in spite of optimistic stats, alternative lenders make mistakes too. For instance, 2019 witnessed at least two major failures in the peer-to-peer market, notably the collapse of UK-based Lendy and FundingSecure. It’s worth noting that as for early 2020 the UK P2P market itself has kept a low profile in the wake of Brexit.

In Vietnam, the state bank wrote a notice to domestic credit institutions that advises them “to be cautious in partnering with P2P lenders”, as some of them have misled investors and consumers.

In the Chinese market things got way out of hand as the whole P2P industry was compromised by hundreds of pyramid-scheme scandals. What’s more, there were numerous reports of debt collectors using intimidation and harassment techniques — something that’s common for the South-East region. Think about the scale: more than 4,000 people have lost as much as $117 million following the crash of just one(!) P2P lender PPMiao. As a result, in November 2019, the Chinese government gave P2P lenders two years to reinvent their model and become small loan providers — strict as that. The China Banking and Insurance Regulatory Commission (CBIRC) reported that by the end of the year, just 427 existing P2P companies were still active, down from 6.000 in 2015.

R is for Regulations

The industry is relatively young, and those stories reflect mistakes associated with growth and a lack of experience. For instance, not every P2P provider carries out proper identification of a loan agreement parties. Some lenders accept a simple electronic signature that allows the use of another person’s data. What’s more, sometimes a mobile phone number or account in social media is enough for registration.

The solution lies in developing a regulatory sandbox to bring the best out of technological and business innovations. To protect both borrowers and investors, regulations must provide a wide framework for lenders to adhere to. Among others, this includes the requirement to hold certain capital on account books in case platforms experience financial difficulties.

The use of big data is also a vital question. In the European market, both GDPR and PSD2 were introduced to increase the transparency of payments. These standards influence P2P lending directly: now lenders have to follow remote identification procedures for storing and handling user data.

All in all, with regulations in hand, alternative lenders will build a healthier culture internally and bring fair value to customers. Surely, this will require a change of mindset, but P2P providers must embrace a customer-centric approach and stick to transparency. From their part, clients must fully understand the principles of alternative lending and bear responsibility for their choices.

The Future of Partnerships

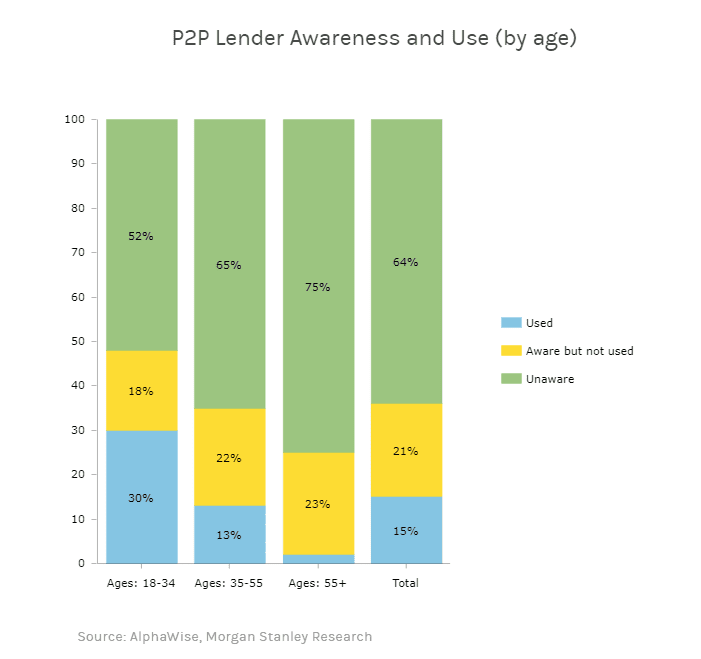

According to statistics, the Millennial and Gen Z generations account for 38% of the global workforce. In the next ten years, that figure is projected to reach 58%, strengthening the positions of youthful generations in the workplace. This basically means that this group will become the main target for lenders. For instance, in the European market, more than 50% of the P2P market consists of people aged 22-37, both borrowers and investors. By matching this demographic group with the right solutions, banking institutions won’t miss lucrative market opportunities.

With this goal in mind, the banking sphere is actively turning to strategic partnerships with P2P services and digital money transfer platforms. Those partnerships seem like a perfect match: banks know regulations from A to Z, have the market reach and structured data for underwriting, and fintechs come up with technology and customer experience.

P2P lending is one of the most disruptive innovations in the domain of finance. The recent innovations such as the blockchain, smart contracts, and the development of more advanced scoring models may also add to transparency in the P2P domain and drive market growth. The bottom line is when choosing a loan, Millennials resort to up-to-date options to avoid the fuss and red tape.

Traditional players want to learn how alternative lenders are using big data in their solutions. Huw van Steenis, the head of Morgan Stanley European financial services, puts it this way: “Banks will be forced to provide a similar level of service and pricing if they hope to compete and stay relevant to their customers.” Given all this, partnerships will likely be the dominant trend in the lending domain in 2020.

The further development of AI and machine learning could accelerate the industry, making it more efficient for all parties. However, P2P lending comes with much more than pure convenience. It’s a chance for financial inclusion of the global underbanked, a shot at making a social difference for the world.

Author Bio

Dmitri Koteshov is the digital content marketer at HES FinTech, a fintech company behind comprehensive lending and credit scoring solutions. As a seasoned professional, Dmitri maintains a longstanding interest in providing insights on fintech software development and analyzing current technology trends.