We may only be half way through 2021, but it’s already been a landmark year for special purpose acquisition companies (SPACs), which have already surpassed their record-breaking 2020 levels of performance. However, with many financial phenomena, the SPAC boom has led to calls that we may be in the middle of a bubble that’s set to eventually burst. With this in mind, are SPACs just a passing fad? Or are they here to stay?

Firstly, let’s address what SPACs actually are. Special purpose acquisition companies are shell businesses that have been solely set up to generate funds through initial public offerings, with the eventual goal of financing a merger or acquisition of a separate business – typically within a two year timeframe. The acquired business then goes public.

SPACs are unique entities because they have no commercial operations – they only take the money raised through IPOs and various other processes in bringing other companies to market. SPACs are often known as ‘blank check’ companies, because the people investing in the SPAC will have no idea about the company being targeted for acquisition prior.

(Image: Amundi)

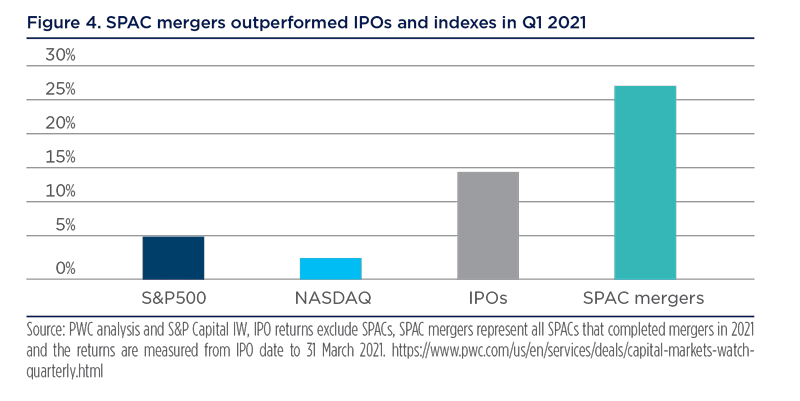

Interest in SPACs has already reached fever pitch in 2021, with Q1 data showing that special purpose acquisition mergers have already outpaced other IPOs and various indexes over the course of the year.

(Image: Bloomberg)

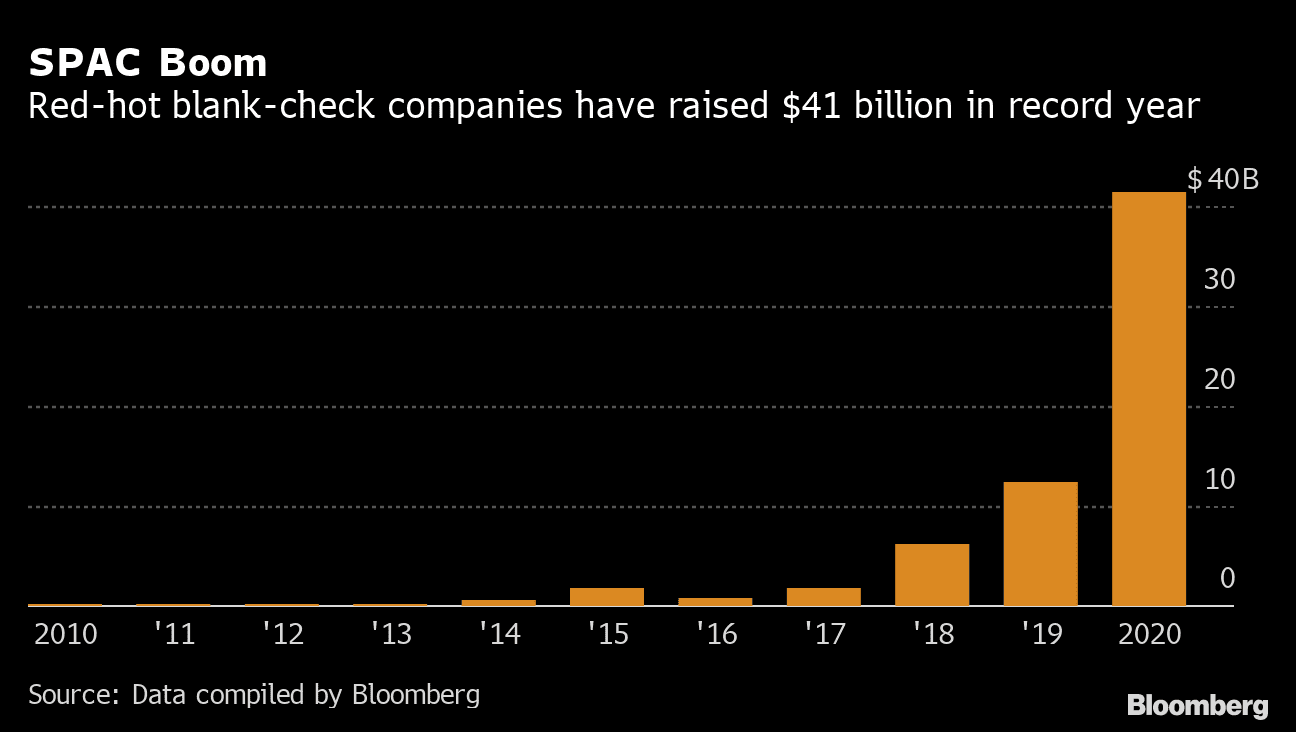

As Bloomberg data shows, 2020 was a record breaking year for SPACs, with special purpose acquisition companies raising some $41 billion over the course of the year.

With such a significant level of momentum already gathered by SPACs, it’s worth asking just how long the boom can last, and whether it’s here to stay or more of a bubble.

Do SPACs Exist Inside a Bubble?

It’s reasonable to expect that such a meteoric rise in the prevalence of SPACs will lead to calls of a bubble existing. Some analysts are speculating that the trend has been overblown by companies listing at increasingly early times, leading to some companies gaining access to capital before they’re ready.

However, there are many cases of companies that have been significant successes based on entering the market with the help of special purpose acquisition companies. For instance, DraftKings went on to be one of the most successful SPACs of 2020, having gone public around eight years on from its formation. This timeframe is similar to that of Facebook and twice as long as the four years Apple spent before opting to enter the public market.

There have also been arguments that SPACs allow some companies to hit the market before they’ve matured enough to turn a profit, but this also needs to be considered with some more perspective. Companies like Amazon, Tesla and Uber all launched flotations before they had begun reporting profits.

Among the examples of companies listed, evidence of a clear and actionable vision, effective leadership and patience from investors were the driving factors behind their market success – as opposed to the way in which they entered the market. This indicates that SPACs can be capable of speeding up the flotations of companies that may go on to become great successes when arriving on their respective stock markets.

Investor Sentiment Could be a Deciding Factor

The success of SPACs are down in no small part to the COVID-19 pandemic, which has enabled a significant number of retail investors to enter the market with a level of liquidity that may not have been possible without social distancing and lockdown measures.

Speaking on this new wave of sentiment, Maxim Manturov, head of investment research at Freedom Finance Europe, said: “The pandemic supplied additional reasons for the retail investment market to grow. To support the economy, most countries adopted stimulating policies, which brought both the loan and deposit interest rates to historic lows.”

“A great number of retail investors buy shares of the companies, which are well known and highly volatile, and post hundreds of percent market cap gains, yearly. Such investors are often referred to as Robin Hoods, they like investing into technology, biopharma, and SPAC companies. Most of such companies have much higher ratios compared to the industry average.”

As a result of this new trend of retail investment, tech, biopharma and SPAC interest has reached new highs, but there are warning signs that market sentiment towards SPACs is beginning to cool as we begin to move away from the COVID-19 pandemic and towards the age of the ‘new normal.’

According to David Trainer, CEO of New Constructs, an investment research company, investors are becoming more wary of the fragility of SPAC flotations, which has seen SPAC valuations “deservedly cut” as a result. Meanwhile, Charlie Munger, vice chairman of Berkshire Hathaway, said that the SPAC boom “must end badly,” although he hasn’t been able to offer insight into when such a negative outcome will take place.

One of the most notable criticisms of SPACs comes from the lack of regulatory scrutiny that they’re placed under when sending companies public in comparison to more traditional IPOs. In fact, UBS is barring financial advisors from pitching some SPAC stocks to clients because of the sheer lack of data available for investments to take place in an informed manner.

These criticisms of the SPAC framework will likely be the biggest test for the movement’s sustainability. Whether we’re in a bubble or special acquisition companies are here to stay will likely be determined by how much investor sentiment the boom can retain in the face of its more established critics. With this in mind, we may realise sooner rather than later whether the SPAC rally of 2020 and 2021 was just a passing fad.