The crypto world has been abuzz recently, not due to market fluctuations or the launch of a new token, but because of a single footnote buried in a 41-page legal document from the U.S. Securities and Exchange Commission (SEC). In its Amended Complaint against Binance, the SEC clarified something that, for years, has been a point of confusion and contention: what exactly constitutes a “crypto asset security.” While it might seem like a niche legal distinction, Footnote 6 could reshape the way we think about regulating crypto assets, and it has far-reaching implications for the industry.

The Shorthand of “Crypto Asset Security”

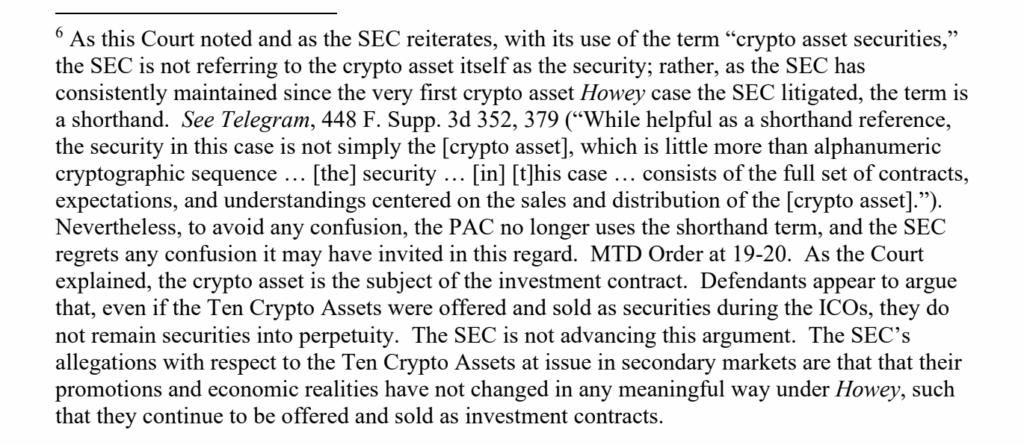

In Footnote 6, the SEC acknowledges that when it uses the term “crypto asset security,” it isn’t referring to the token itself as the security. Instead, it’s referring to the broader “investment contract” that surrounds the sale of that token—the bundle of contracts, expectations, and understandings between the parties involved in the transaction. To put it simply, the security isn’t the digital asset (or token) itself but the circumstances, promises, and expectations tied to how that token is marketed and sold.

This clarification is crucial. For years, many in the crypto space have been frustrated by the SEC’s seeming overreach in declaring that certain tokens themselves are securities. The token, in most cases, is just code. It’s the agreements made around the sale—promises of future profit, the pooling of funds, and the reliance on someone else’s efforts—that create the investment contract.

In doing this, the SEC is essentially saying: we don’t care about the token, we care about the promises made around it.

The SEC’s Evolving Approach

This footnote is not a complete departure from the SEC’s previous positions, but it does represent a refinement of its approach. Historically, the SEC has relied on the Howey test, a legal standard set by a 1946 Supreme Court decision, to determine whether an arrangement constitutes an investment contract. The Howey test looks at whether there is an investment of money in a common enterprise, with the expectation of profits derived from the efforts of others. The token itself, as the SEC now makes clear, is not inherently part of this equation; it’s how the token is sold and the expectations built around it that matter.

What this means is that crypto projects and token issuers will need to be far more cautious about how they promote their assets. It’s no longer sufficient to claim that a token, by itself, isn’t a security. The SEC is paying close attention to the ecosystem surrounding the token—the contracts, marketing materials, and any promises or expectations of profit.

Why This Matters for the Industry

For crypto businesses, this clarification from the SEC is a double-edged sword. On the one hand, it brings much-needed clarity to an area of regulatory uncertainty. It’s not the tokens themselves that attract scrutiny; it’s the context of their sale. This could give crypto projects more freedom to innovate, as long as they’re careful about how they structure and market their offerings.

However, the challenge lies in how the SEC will enforce this distinction. Now that the agency has admitted it has used the term “crypto asset security” as a shorthand, it will need to demonstrate that the marketing and sale of a token—especially in secondary markets—continue to meet the Howey criteria. This won’t be easy. The SEC will need to show that promises of future profits and reliance on third-party efforts persist, even as tokens change hands.

Moreover, the SEC’s statement about avoiding “any confusion it may have invited” speaks volumes. It suggests that the agency is aware that its previous terminology might have been too broad or misleading. This admission could open the door for stronger legal defences from token issuers, particularly in cases where the secondary market trading of tokens doesn’t involve the original issuer at all.

Implications for Secondary Markets

Perhaps the most important takeaway from Footnote 6 is its potential impact on secondary markets. The SEC appears to recognise that while tokens may be sold as securities during an Initial Coin Offering (ICO), they don’t automatically remain securities once they hit the open market. This distinction is key for many crypto businesses and investors, as it provides a clearer path for compliance. Once the initial sale is over, and if the accompanying promises or expectations change, the token may no longer meet the criteria of an investment contract.

That said, the SEC is not letting token issuers off the hook that easily. The agency is likely to continue scrutinising how tokens are marketed and traded on secondary platforms. If a token’s value still hinges on the efforts of its creators or promoters, it could still be considered a security, even after the ICO. In short, the focus shifts from the token itself to the ongoing representations made about it.

A New Era of Crypto Regulation?

Footnote 6 may seem like a small legal footnote, but it has the potential to herald a new era of crypto regulation. It signals that the SEC is refining its approach, moving away from treating all tokens as securities and towards a more nuanced understanding of the digital asset space. For the industry, this brings both opportunities and challenges.

The opportunity lies in greater clarity. The SEC’s focus on the surrounding agreements and expectations means that token issuers can be more precise in how they structure their offerings to avoid triggering securities laws. However, the challenge remains: the SEC is not backing down from its mission to regulate the crypto space, and it’s clear that enforcement actions will continue, albeit with a more targeted approach.

As the crypto industry matures, it will need to engage with regulators like the SEC in more constructive ways. Footnote 6 could serve as the foundation for a new regulatory framework that balances innovation with investor protection. For now, token issuers and investors alike should take note of the SEC’s evolving stance and tread carefully as we navigate this new terrain.