You’ve been trying for a while now to handle your credit card debt on your own. You’ve meant well, but now you’re only remitting minimum monthly payments or less, if you’re making payments at all.

You are overwhelmed, and you know you can’t move forward in life — you can’t truly progress — until you deal with your debt.

The good news is that there are solutions available to you. One is debt relief, also known as debt settlement. But is the strategy right for you? Let’s explore that and others.

Here are the options and consequences of debt relief.

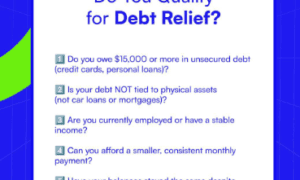

Who is a Debt Relief Candidate?

You many want to consider debt settlement, debt management or bankruptcy if you can’t see yourself paying off your credit card or other unsecured debt within five years, even if you slash spending drastically.

You may also need one of those solutions if your debt comes to at least half of your gross income.

What is Debt Settlement?

Debt settlement is a financial strategy wherein you hire a firm to negotiate with each of your creditors to see if they would accept less than what you owe to “settle” your obligation. Creditors usually go along because, well, something is better than nothing, which is what they may get if you pursue bankruptcy, which is your other likely option.

How it works is, rather than pay creditors directly, you deposit cash monthly into an escrow-like account that you control. Once you’ve saved enough, your negotiators will begin negotiations with your credit card issuers. You pay the agency – Freedom Debt Relief has a great credit card debt relief program — nothing until settlements are reached.

A short-term consequence is damage to your credit, which the process of debt settlement causes. However, once your debts are cleared and you begin rebuilding your credit, your credit scores will rebound. Also, your credit report is likely not great these days anyway.

What is a Debt Management Plan?

This solution is a repayment plan in which a credit counselor assists you with determining the amount you can reasonably pay toward your debt, in accordance with your financial goals.

For a nominal fee, the counselor negotiates with your creditors and, with the funds you provide monthly, makes payments to your creditors until the bills are fully paid. This typically takes between three to five years.

Note that while participating in a debt management plan, you cannot obtain new credit. You must also close your existing credit cards and allow the credit counseling agency to manage those accounts. Also, enrollment in such a plan will be noted on your credit report.

What is Bankruptcy?

Widely considered the remedy of last resort, bankruptcy is a legal process that is overseen by federal bankruptcy courts that was created to help people get rid of all or most of their debt or to help them repay part of what they owe.

The consequences of bankruptcy are serious and long-term. Depending on the kind of bankruptcy you file – Chapter 7 or 13 — the filing can remain on your credit report for seven to 10 years. During this time, it will be difficult for you to open lines of credit or be approved for loans with reasonable rates.

You also may have to relinquish some of your possessions including real estate, vehicles, and jewelry.

In summary, when mulling the options and consequences of debt relief, carefully consider your short- and long-term goals when deciding on the strategy for you. Once you’re back on the right track, be mindful that you must get control of your spending to avoid falling into the same financial situation.