Online banking is among the most impressive tech developments of the 2010s for retail users. In this review, we’re going to cover the basics of modern payment systems like N26, Tandem, Wise, Revolut, Tinkoff, Monobank and Tonio, the sphere of problems it addresses, and the most promising directions of their progress.

What are payment systems and how does it work: Highlights

While the definition of payment systems hasn’t been ossified yet, we already can discuss its core aspects, benefits, advantages, and disadvantages.

- Simply put, an online payment system is a ‘digital-first bank’ that typically has no ‘offline’ offices: all its operations are executed in mobile or desktop applications as well as in web interfaces;

- The concept of ‘challenger payment systems’ garnered public attention after the financial collapse of 2008-2009 and became mainstream in the 2010s;

- Online payment systems are characterized by very low operational costs, high-speed operations, and a trustless approach to data processing;

- Meanwhile, the interfaces of those programs can be too sophisticated for elderly people, its regulation is still in its very infancy while their toolkits still lack major functionality;

- Cryptocurrency-centric instruments (stablecoins, decentralized lending protocols, blockchain-based cross-border remittances systems) can also be treated as a type of online payment system, but with its own specifics.

As such, online payment systems have become an integral part of the global financial system. Highly likely, in coming years, modern payment systems might evolve into a dominant concept in B2C banking. For the clients of the B2B segment, applications can also advance the interaction with customers, counterparties, supervisors and tax bodies.

Mobile-first fintech apps: Streamlining bank operations in retail

To start deobfuscating the concept of ‘online payment systems’, we need to understand the effects of the 2008 Global Crisis for ‘old-fashioned’ banking. Online payment systems gained traction as the global recession amplified the various groups of drawbacks demonstrated by classic banking giants.

Some of the first-gen payment systems – online banks underpinned by fintech applications in smartphones – exploded onto the areas underserved by the heavyweight banks (Barclays, HSBC, Lloyds Banking Group, and NatWest Group). Others raised investments from the banks affected by global recession or emerged to replace the collapsed banking institutions.

While the sphere of online payment systems remains fragmented and diverse, all of them have one distinctive feature: they strive to work in a digital-only manner without building the ecosystems of offices and branches.

According to BBVA Research, the term itself was coined not later than 2016. The popularity of powerful and feature-rich smartphones was the technical basis of online payment systems popularity upsurge. Since the outbreak of COVID-19 pandemic, the ‘remote-only’ nature became another catalyst of its massive adoption.

Basically, payment systems offer their customers the full range of services associated with ‘traditional banks’ including credits, payments, money transfers and so on. Also, digital payment systems associated with payment systems can be either used as alternatives to bank cards or together with these cards.

The interface of Wise app // Image by Wise

Online payment systems champion business models different to those of traditional banks: instead of relying on high mortgage and interest rates, they made up the lion’s share of their income from transactional fees. N26, Tandem, Wise, Revolut, Tinkoff, Monobank and Tonio are among the textbook examples of modern payment systems.

Challenges and promises of online payment systems in 2023

The concept has its own obvious strong points. First of all, online payment systems are resource-efficient: their operational costs are significantly lower than that of classic banks. It needs to build or rent offices, to hire staff, and so on. Their front-end teams are just call-centers with customer support operators.

Also, payment systems are way more accessible: they work 24/7 while basic operations can be performed even without stable Internet connection. Thus, users can pay with a card or send money transfers whenever they want.

Last but not the least, these systems are more flexible in terms of tech development and marketing compared to their predecessors. New functions can be implemented easily while the toolkit of functions supported can be customized for this particular group of users.

Meanwhile, this overhyped concept comes with its own roadblocks. First, the toolkits of some payment systems are limited: for instance, the operations with large sums of money can be authorized only in-person. Then, online payment systems lack trust for some categories of customers. Impersonal assistance can also be highly confusing for seniors and people with low levels of tech experience. Finally, as the operations in payment systems don’t require ‘personal’ authorization, it unlocks notable opportunities for fraudsters of various types.

Online payment systems and regulators: Various approaches, various frameworks

While payment systems are delivering the same range of services as traditional banks, their operational routine is too different to work without specifical regulations. The analysts outline that, in the majority of jurisdictions, banks can either obtain a ‘full’ banking license or some sort of ‘limited’ license for fintech, money services businesses, and so on.

- Full banking license is the most difficult to obtain, but it allows payment systems to offer the same services with its ‘classic’ competitors: accept deposits, issue loans, handle money transfers, support integrations with public services, providing receipt and documents, interacting with tax authorities, and so on.

Full banking license can be obtained in 10-15 months. Typically, banking licenses for online payment systems are issued by central banks (CBs) or other regulatory authorities. These regulatory bodies can be regional or global such as the European Central Bank (ECB) in Europe or the Federal Reserve in the United States of America, as well as local national bank regulators such as the Saudi Arabian Monetary Authority (SAMA) or Hong Kong Monetary Authority (HKMA). The procedure of obtaining a license can be rather costly for early-stage payment systems , but it comes with great competitive benefits.

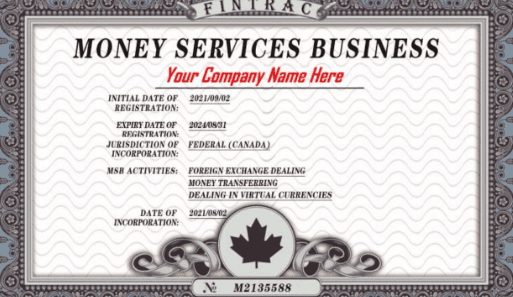

- Fintech license is a special ‘light-weight’ type of license available only for modern fintechs and payment systems with limited functionalities. It can be issued by some regulatory or supervising unit and only allows to devliever a limited range of services: for instance, to issue small-sized loans or to process payments of up to $5,000 in equivalent. The most popular license of this type is a European e-money license (also called an EMI which stands for ‘electronic money institution’). EMI is an option suitable for the majority of fintechs while it has some major limitations. For instance, an EMI-licensed payment system is not allowed for credit issuance. It also can’t custody the clients’ money on its own: it can cooperate with the partner that holds an ‘ordinary’ license. Finally, thanks to KYC/AML regulations, the amount of funds clients can store in the accounts of banks with ‘lightweight license’ is limited. In other regions of the world, such licenses are issued by the Monetary Authority of Singapore (MAS), Bank Negara Malaysia (BNM) while the MSB license in the U.S. can also be an example.

The sample of MSB license in Canada // Image by FINTRAC

Payment systems and cryptocurrencies: What’s the difference?

Cryptocurrencies or digital money protocols built on the top of decentralized databases (blockchains and permissioned distributed ledgers) can also deliver basic financial functionalities available for payment system’s ’ clients. In this case, business operations can be executed through centralized services (they are called ‘centralized crypto exchanges’ or CEXes) or completely in-blockchain (for decentralized finance protocols or DeFis). Here’s how crypto-centric systems address major needs in sphere of fintech:

- Loans and deposits. Both DeFi protocols and centralized exchanges can issue loans and accept deposits in 2023. For instance, decentralized protocols Aave Finance, Curve, Kyber Network can issue loans against collateralized cryptocurrencies. The same operations are available on centralized services like Binance, Huobi, and KuCoin. Binance also accepts deposits in stablecoins (cryptocurrencies pegged to fiat currencies or real-world assets) with 5-7% interest.

- Money transfers. Cryptocurrencies have been used in cross-border money transfers since the inception of Bitcoin. Since 2011-2012, the U.S.-headquartered fintech heavyweight Ripple organized ‘money corridors’ in Asia and LatAm. Also, via non-custodial wallets, the users of cryptocurrency can send them to each other without interacting with any money service.

- Retail payments. In recent years, many merchants and e-commerce platforms have integrated cryptocurrency gateways to their interfaces. For instance, Binance Pay ecosystem streamlines payments in online stores in Asia and Europe.

Cryptocurrencies have a number of advantages over payment systems: they are anonymous, work with negligible fees and can’t be censored. However, the level of trust in cryptocurrencies remains low: for instance, the receipt from crypto applications can’t be accepted by tax authorities as proof of income. Also, some crypto applications have too sophisticated interfaces.

Wrapping up: Pros and Cons of payment systems

To sum up, the online payment system’s segment is still in its infancy in terms of regulations, infrastructure, interfaces, and, therefore, massive adoption in various regions across the globe. Online payment system’s’ teams have a lot of challenges to go through. Accessibility, operability, reliability of many payment systems leaves a lot to be desired.

At the same time, the future looks bright for this young segment. Thanks to its resource-efficiency, cost-effectiveness, flexibility, and ‘online-first’ ethos, the payment systems concept like N26, Tandem, Wise, Revolut, Tinkoff, Monobank and Tonio can evolve into a dominating way of banking for generations to come. The ‘rise and rise’ of the online payment system will be the most impressive paradigm shift in global finances since the inception of the modern economical system.