Finnovista Fintech Radar Latin America, Opportunity for International Fintech.

- Over +85 foreign Fintech companies active in the region

- Mexico, Brazil and Colombia position themselves as the main Latin American destinations for foreign Fintech startups mainly from Europe and the United States.

- The segments of Payments and Remittances, Lending, Scoring, Identity and Fraud and Enterprise Technologies for Financial Institutions lead the offer of foreign Fintech in the region.

February 27, 2018. Finnovista, the impact organization that empowers Fintech ecosystems in Latin America and Spain, launched the first edition of the Finnovista Fintech Radar Foreign Startups in Latin América. On this occasion, Finnovista has conducted a study that, for the first time, aims to identify foreign Fintech startups that are currently offering their services in Latin America, in order to examine the most appealing regional markets for foreign companies and the reasons behind these trends, assess the evolution of new foreign companies entering the market in the following years and try to identify possible opportunities and obstacles in the region.

“In recent years Latin American Fintech entrepreneurship has grown at a rate of 50% and 60% and has drawn the attention of international investors and corporates through investment rounds in startups or strategic partnerships. But at Finnovista we ask ourselves, how appealing does the Latin American Fintech ecosystem result for foreign Fintech startups?” said Fermin Bueno, Managing Partner de Finnovista.

Since 2016 Finnovista has conducted different Fintech Radars about the most representative Fintech ecosystems in the Latin American region in order to create a comprehensive data source of the Fintech enterprises, evaluate the sector’s progress in the region, and give visibility and recognition to a movement that will lead the region towards an ubiquitous and inclusive digital finance landscape. So far, Finnovista has published over 15 studies about Argentina, Brazil, Chile, Colombia, Ecuador, México, Perú and Spain, as well as a regional study with the IDB.

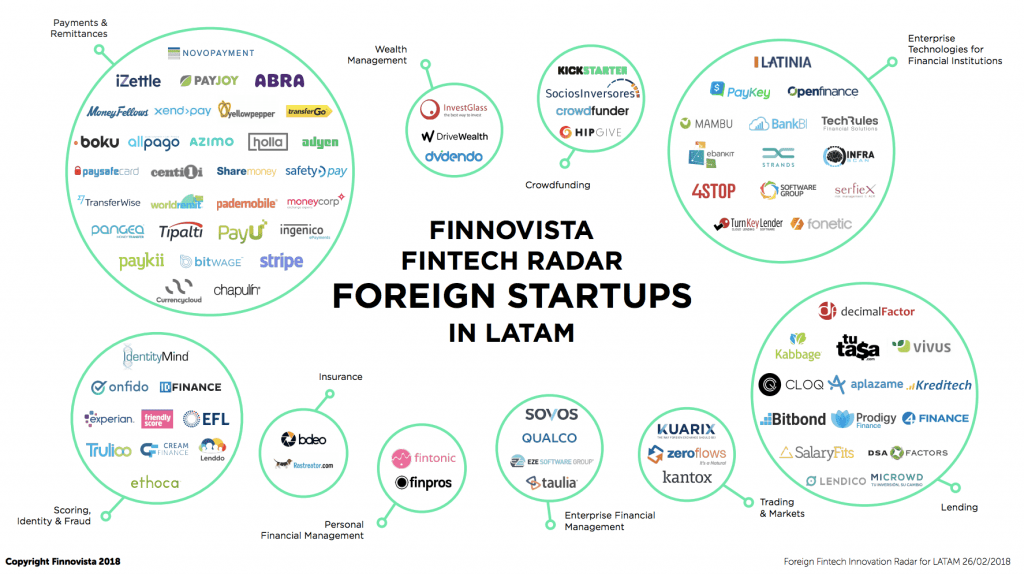

In this first version of the Fintech Radar Foreign Startups in Latam Finnovista identified 86 foreign Fintech startups active in Latin America. 65% of them come from Europe, mainly from the United Kingdom (38%), Spain (31%) and Germany (9%); while 31% of them come from the United States and Canada, mainly from California (30%) and Florida (19%); and only 4% of the 86 startups come from Asia, mainly from Singapore and Philippines.

If we take a look at the countries in which foreign Fintech startups are operating, we observe that the main destinations of these companies mostly coincide with the main Fintech markets in the region in terms of volume of Latin American startups. Precisely, the five markets with a greater presence of foreign Fintech startups are the following:

- Mexico: 74% of the identified startups offer their services in the largest Fintech market of the region

- Brazil, where 46% of the identified foreign startups are active

- Colombia, destination for 33% of the identified startups

- Peru, with 35% of the foreign startups offering their services in the Andean country

- Argentina, where 27% of the foreign Fintech companies are offering their services.

Furthermore, there are seven countries with an average presence of foreign Fintech startups:

- Chile, where 22% of the identified startups are offering their services

- Ecuador, with 15% of the startups operating in the country

- Guatemala, destination of 14% of the startups

- Uruguay, Costa Rica and Dominican Republic, each of them destination of 12% of the startups

- Panamá, with 11% of the startups offering their services in the country.

According to the Fintech Radars conducted by Finnovista in 2017, the main markets in terms of Latin Fintech startups are Mexico (238 startups), Brazil (219), Colombia (124), Chile (75), Argentina (60), Perú (47) and Ecuador (31). As we can see, these countries are also the markets with the highest offer of foreign Fintech services; however, it is important to highlight that Chile, the fourth largest market in terms of Latin American Fintech startups, is not among the five most appealing markets for foreign companies, while Peru, the sixth largest Fintech Latin American market, positions itself as the fourth most appealing market for foreign Fintech startups.

Finally, there are some countries with a minor presence of foreign Fintech startups (below 10%): Venezuela, Bolivia, Guyana, Surinam, Haití, El Salvador, Honduras, Nicaragua, Paraguay, Belice, Barbados and Jamaica.

It is important to point out the similarities and minor differences between Fintech startups from Europe, United States and Canada and Asia regarding the main markets in which they operate in Latin America. Fintech startups from Europe and the United States and Canada share Mexico and Brazil as their main destinations, as 70% of European Fintech startups offer their services in Mexico and 50% in Brazil, while 82% of Fintech startups from the United States and Canada operate in Mexico and 37% in Brazil. However, while the third most important market for European Fintech startups is Peru, for Fintech startups from the United States and Canada the third most important market is Colombia, with 33% of them offering their services in the country. Meanwhile, the most important markets for Asian Fintech startups are Mexico and Colombia, each of them with 100% of the identified startups offering their services, and Brazil and Peru, each of them with 67% of the Asian startups operating in each country.

In order to gain a more comprehensive view about the type of Fintech companies that are entering the Latin American markets, Finnovista has identified the Fintech segments in which these companies are operating. The four principle segments among the identified foreign Fintech startups operating in Latin America are the following:

- Payments and Remittances, accounting for 35% of the identified startups

- Enterprise Technologies for Financial Institutions (ETFI), with 16% of the startups

- Lending, as well accounting for 16% of Fintech startups

- Scoring, Identity and Fraud, with 12% of foreign startups.

The remaining six Fintech segments are all under 10% of the identified startups in the analysis.

If we compare the most representative segments among foreign Fintech startups with those among Latin American startups, we observe there is a coincidence in the relevance of the Payments and Remittances segment. In Mexico, Colombia and Brazil it is the largest segment in terms of Latin American Fintech startups, occasionally sharing this first position with the Lending segment, which this time is the third most important segment. However, it is important to stress the importance gained by the segment Enterprise Technologies for Financial Inclusion among foreign Fintech startups, as it is the second largest segment in number of Fintech startups (16%) alongside the Lending segment, while for Latin American Fintech startups it is still an emerging segment, as seen in Mexico and Colombia, where it represents 5% and 6% of the startups respectively. These results highlight the importance gained by B2B services with a diversified supply of technological services beyond a unique product among foreign companies in comparison with Latin American startups.

On the other side, Finnovista also identified an important amount of Fintech startups within the segment of Scoring, Identity and Fraud. In Mexico this segment only represents 2.5% of the total amount of Latin American Fintech startups in the country and 5% in Brazil, and this increases up to 12% of the total amount of foreign Fintech startups identified in the region. This large amount of foreign companies that enter Latin America offering risk management or digital identity solutions could be a sign of the need to start endowing the market with a technological framework capable of preventing risks associated with mature markets.

Once again, we can observe the huge opportunity that the Latin American market represents for Fintech startups from the region as well as for foreign Fintech startups that are looking to expand operations in foreign countries. Precisely, as we already highlighted in previous studies, in Latin America there are two elements that contribute to the importance of the Fintech sector: a high rate of unbanked people and a high technological penetration.

According to the World Bank, it is estimated that 2 billion adults (42% of the global adult population) are excluded from the formal financial system. In Latin America 49% of the adult population does not have access to a bank account, a figure well above the average of 6% in high income countries of the OECD. Given this situation, Fintech services represent the most important driver to improve financial inclusion due to its capacity to optimize costs and improve the supply of products and services, and a great market opportunity as it has the capacity to reach a segment of the population that was previously unattended by traditional financial services.

In this sense, Latin America represents a great opportunity for Fintech companies from around the world that are looking to address this market through the massive adoption of mobile technology. In 2016 the region had already 450 million smartphones and, according to the Mobile Economy Report 2016 by GSMA, this penetration is expected to increase up to 76% of the population within three years. This technological adoption has driven the adoption of formal financial services in the region to such an extent that in 2016 Latin America became the region with the largest increase in digital banking accounts, reaching the 10 million digital bank accounts at the end of the year in comparison to the one million in December 2011.

In recent years Governments and regulators have understood the power that technology has in creating a more inclusive financial system, fighting against poverty and stimulating economic growth. A number of initiatives have been taken which have promoted the emergence of regional and international Fintech solutions, such as the policy of electronic invoicing in Mexico, Chile, Brazil, Ecuador, Argentina, Guatemala or Peru among others, which requires buyers and sellers to register the invoices of each transaction electronically, accelerating the digitalisation of finance and the creation of Fintech companies offering Enterprise Financial Management services.

However, there are still a lot of challenges that need to be addressed in order to attract more foreign companies. On one side, the political instability in countries like Venezuela or the economic volatility in countries like Mexico due to the uncertainty brought about by the trade policy with the United States could present a barrier for foreign countries when selecting Latin America as the destination for their international expansion. Furthermore, it is necessary to create clear and homogeneous regulatory systems that permit the development of a favourable ecosystem for entrepreneurship and innovation. Finally, because technology on its own is not a guarantee of success, those companies that begin to operate in Latin America must understand the complexity and singularity of the markets in each country in order to adapt their products an services and solve the specific needs of each segment of the population. To this respect,

acceleration and/or scaling programs such as Startbootcamp FinTech Mexico City can be a very interesting options for startups that are looking to enter new markets, as they provide the necessary tools that might help in understanding the market as well as the opportunity to connect with investors and potential clients that, as mentioned by Diana Florescu, can be very useful when beginning an internationalisation process towards an unknown market.

“At Finnovista we are convinced about the potential of the Latin American Fintech ecosystem both for regional and international startups, especially for those sharing cultural aspects that could benefit from an easier entrance and adaptation of their products and services in these new markets, as in the case of Spain”, concluded Fermin Bueno. 2017 was the year in which we saw a massive growth in the number of Latin American Fintech startups, and we are convinced that 2018 will be and exciting year where we observe a positive evolution of the foreign market with the entrance of new competitors that foster and accelerate innovation in order to transform the financial industry and build a more inclusive world.

About Finnovista

Finnovista is an impact organization that empowers Fintech ecosystems in Latin America and Spain through a collaborative Fintech platform that encompasses acceleration and scale programs, conferences, hackathons, research, competitions and a dedicated Fintech co-creation space. At Finnovista we build bridges between financial institutions and Fintech startups with the vision of transforming finance for a better world at the intersection of entrepreneurship, technology and innovation. For more information visit http:www.finnovista.com where you can find additional details.

Press contact

Finnovista Jessica Pleguezuelos jessica@finnovista.com Tlf. +34 629 006 371

You can find all the information about this report at: https://www.finnovista.com/fintechradarforeignstartupslatam2018/?lang=en