Heading into 2022, shipments of almost all consumer electronics products such as mobile phones, TVs, and computers are declining.

Due to the Russia-Ukraine conflict, global inflation, supply chain disruptions caused by the pandemic and other factors, consumers have become increasingly pessimistic about the economic trend, and the global demand for consumer electronics has also shrunk sharply.

Against this backdrop, industry cancellations have also increased. On July 10, Taiwan media quoted sources in the island as saying that Samsung will extend the suspension of parts procurement period, due to the high inventory of some products, even the end of the year will not be restocked. Meanwhile, Dell, the US PC giant, is said to be cutting orders for its entire PC line by 50%, regardless of whether it has previously signed a supply and quantity guarantee agreement, in order to avoid falling stock prices.

Worryingly, consumer electronics have shown a long-term trend of continuing to cool. A phenomenon that has to be paid attention to is that the consumer electronics industry is gradually entering the mature stage of this round of product innovation cycle, the growth of the existing market space is slowing down, and the industry chain competition is intensifying. In secondary market investment, the consumer electronics industry is no longer a growth track that can give a high valuation. In the view of some industry insiders, the investment logic has even turned from growth to cycle.

According to a new forecast from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker, global shipments of traditional PCs will fall 8.2% year over year in 2022 to 321.2 million units. Similarly, the forecast for worldwide tablet shipments has been lowered to 158 million units, a 6.2% decline compared to 2021.

IDC expects shipments to return to positive annual growth in 2023 and beyond, although this year’s decline will result in a five-year compound annual growth rate (CAGR) of -0.6%. Meanwhile, tablets face a larger decline over the same period as competition from PCs as well as smartphones will continue to inhibit growth, leading to a -2.0% CAGR.

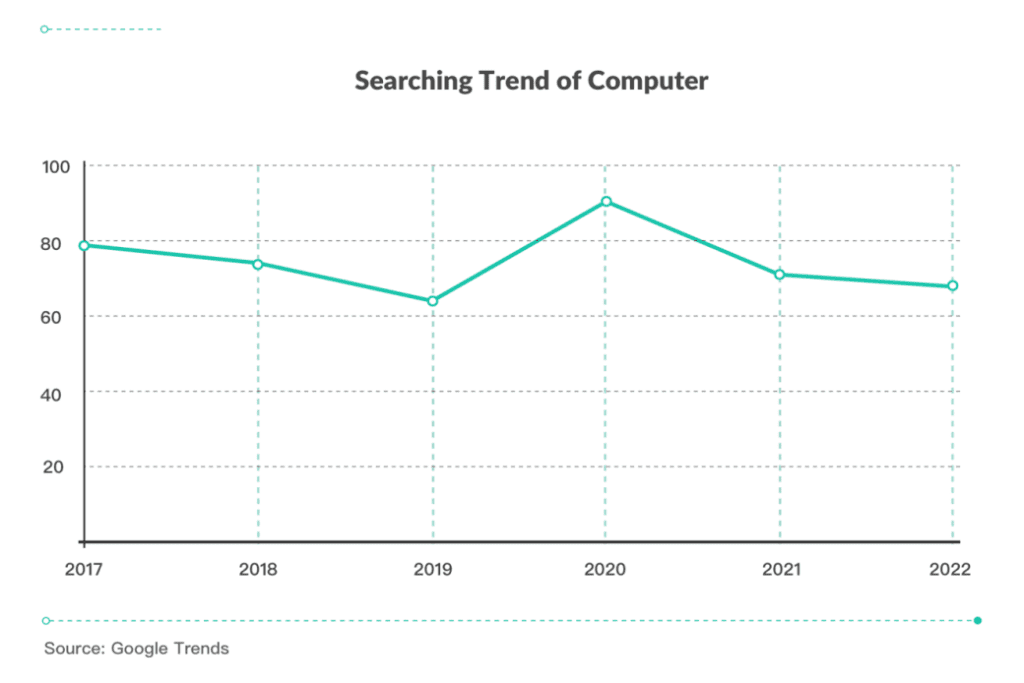

According to data collated by coupon website CouponBirds, search trends of computers are also declining. Before the pandemic, interest in computers declined year by year, from 79% in 2017 to 64% in 2019. In 2020, the outbreak of COVID-19, people being quarantined at home led to a rapid increase in the demand for working from home, making personal computers indispensable. As a result, searches for computers have gone straight to the top. With the current pandemic abating, people can get out and about and back into the office, and interest in computers has plummeted.

“Supply shortages have plagued the industry for a while and the recent lockdowns in parts of China continue to exacerbate the issue as factories struggle to receive new components from upstream suppliers while also facing issues downstream when it comes to shipping finished goods,” said Jitesh Ubrani, research manager for IDC Mobility and Consumer Device Trackers. “While the restrictions are expected to ease soon, worker sentiment within the supply chain remains muted, and backlogs of deliveries will persist for the remainder of the year.”

While supply chain deliveries have eased from the second half of last year, some mobile phone components are still in short supply, mainly for low-end and mid-range smartphones. In particular, the delivery delay of 4G SOC is quite prominent. Delivery time is about 30 to 40 weeks. Due to limited capacity planning, the market demand for low-end and mid-range phones has not been met since last year.

According to Canalys data, in the first quarter of 2022, global smartphone shipments fell by 11% year-on-year. For example, Samsung still ranks first in the market, its shipments fell by 4% year on year. In the dominant European and Indian markets, Samsung’s mobile phone shipments fell by 9% and 2%, respectively.

In late June, Sunny Optical, a supplier of camera modules for mobile phones, said in an institutional survey that it expects global mobile phone sales in 2022 to be 1.22 billion units, a year-on-year decrease of 7.9%. China sold 260 million mobile phones, declining 16.9% year on year. European market sales of 170 million units, down 15% year on year. Other regions sales are 790 million units, down 2.6% year on year.

The TV market is also not optimistic. Omdia forecast in May that global TV shipments in 2022 were estimated at 211.639 million units, the lowest since 2010 and about 1.89 million less than last year. In the first quarter, demand in the North American, European, and Chinese markets fell sharply by around 20% from a year ago.

This year’s consumer electronics industry is in crisis. Although next year it may turn out to be better, but the difficult situation will continue. Because of Russian-Ukrainian conflict, inflation, supply chain tensions and shrinking demand, the current consumer electronics situation is not optimistic. Many investors are also less confident in the sector than they once were.