For years, green hydrogen has been described as a future solution for decarbonising industry and heavy energy use. What has been missing is a credible timeline — not based on targets or announcements, but on how investment, technology and real operations are actually unfolding.

That picture is now becoming clearer. Major oil and gas companies, industrial players and utilities are still investing in green hydrogen, but with far more discipline than in earlier years. Fewer projects are moving forward, but those that do are larger, more focused and tied to real customers. This shift makes the transition slower than early forecasts suggested — but also far more predictable.

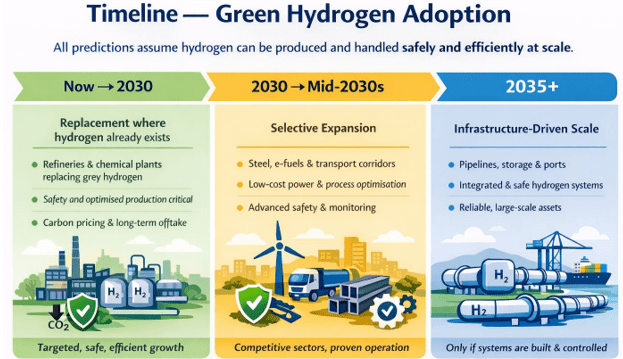

A practical timeline for green hydrogen adoption

Now to 2030: replacing hydrogen where it already exists

In the near term, green hydrogen adoption is concentrated where hydrogen is already used today — mainly in refineries and chemical plants. These sectors already understand hydrogen handling, have safety frameworks in place and can justify higher costs through regulation, carbon pricing or long-term offtake agreements.

This phase is less about rapid growth and more about learning how to operate green hydrogen reliably at scale. Projects that succeed do so by focusing on stable production, tight process control and continuous monitoring. Those that struggle tend to underestimate operational complexity rather than technology readiness.

2030 to the mid-2030s: selective expansion

From around 2030, green hydrogen begins to move beyond its traditional base — but only selectively. Steel production using direct reduced iron (DRI), e-fuels for aviation and shipping, and certain heavy transport corridors become viable in regions with cheap renewable electricity and predictable demand.

Margins in this phase are thin. That means efficiency losses, safety incidents or unstable operation can quickly destroy the business case. As a result, optimisation and real-time control become essential rather than optional.

2035 and beyond: infrastructure determines scale

Beyond the mid-2030s, the role of green hydrogen depends less on electrolysers and more on infrastructure. Pipelines, storage, ports and integrated control systems will decide whether hydrogen remains an industrial fuel or becomes a broader part of the energy system.

At this stage, trust becomes critical — from investors, insurers and regulators. That trust depends on proven safety and long-term operational performance.

Why safety and optimisation are central to the transition

All timelines for green hydrogen assume one critical condition:

hydrogen must be produced and handled safely and efficiently at scale.

Hydrogen is unforgiving. Small amounts of oxygen ingress, leaks or unstable operating conditions can create safety risks, reduce efficiency and increase costs. Without reliable monitoring and control, even well-designed plants struggle to operate consistently.

This is why attention is shifting away from headline capacity numbers and towards how hydrogen plants actually run day to day.

Turning ambition into operation

Hydrogen and oxygen gas analysers play a key role in this transition. Continuous measurement of oxygen, hydrogen and other critical gases allows operators to detect unsafe conditions early, minimise losses and maintain stable production as plants scale up.

Modcon is one of the companies working in this area, supporting hydrogen producers with on-line gas analysers and real-time monitoring systems designed for demanding industrial environments. By focusing on measurement, control and optimisation, this type of technology helps hydrogen projects move from concept to bankable, reliable operation.

The real signal to watch

Green hydrogen is not failing — it is being priced, engineered and tested. The transition will not happen everywhere at once, and it will not be driven by ambition alone. It will be driven by projects that can prove they are safe, efficient and optimised in real operation.

The timeline is no longer theoretical. It is being written now, one operational plant at a time.