- By Charu Chanana, Market Strategist at Saxo Capital Markets

Summary: The US dollar strength seems stretched, but stagflation risks in Europe and UK as well as sustained weakness in the Chinese economy continue to suggest that there may be further runway. While a strong dollar helps to rein in inflation for the US, it may not bode well for the domestic economy or investors with a large international exposure. However, this may also be the time when international exposure looks more affordable and attractive.

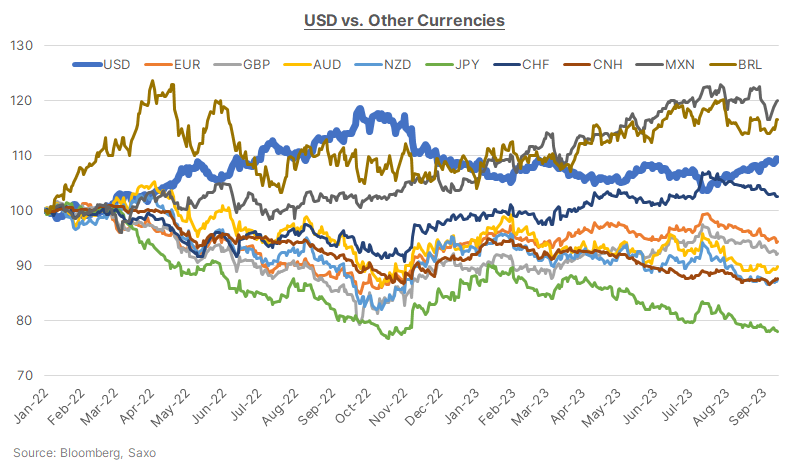

US dollar is proving hard to turn around

Most central banks appear to be at the end of the tightening cycles, but this fast-paced rate hike cycle has brought a splurge of gains in the US dollar. Higher yields and sustained strength in the US economy have underpinned the King Dollar and talks of rate cuts so far have proved to be premature. Fed funds futures are pricing in 2024 terminal rate of 4.5% at the time of writing in mid-September, with the first full rate cut priced in for June. Compare this to pricing at the start of the third quarter, when end-2024 rate was seen to be 4.1% and the first full rate cut was priced in for May 2024.

Note: Indexed to 100 as on 3 January 2022

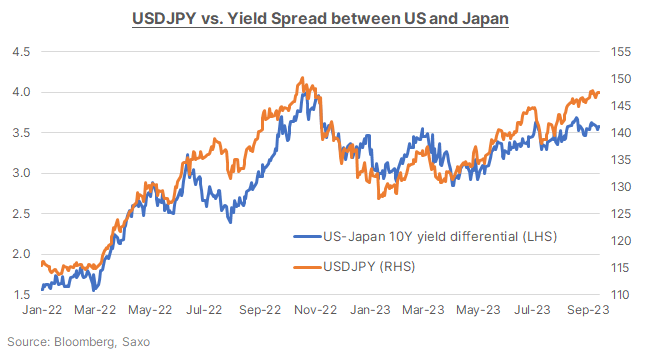

FX markets from here will start to focus more on which central banks would switch over to an easing cycle first, and how relative rate cut aggressiveness will play out. Yield differentials could start to be a secondary factor for currencies as we head into the fourth quarter and into 2024. The still-firm US August core CPI continues to put the focus on the Fed’s higher-for-longer message for now, but a weakening of economic momentum in the US in Q4 could shift that rhetoric. Higher interest rates and tighter financial conditions could further filter through the economy, weighing on businesses. We also see risks to the consumer in the fourth quarter, with the erosion of pandemic savings and the start of student loan repayments weighing on household budgets. This weakening of the US economy could bring rate cut expectations forward from mid-2024 for now, weighing on the USD.

However, the relative strength of the US economy compared to Europe or China could continue to provide a supporting bid for the dollar. Stagflation risks are running the highest in the Eurozone and the UK, suggesting dollar losses against the EUR and GBP may remain hard to come by. With EUR’s high weighting in the Bloomberg Dollar Spot Index, that means an overall downward trend in the dollar could be evaded until stagflation concerns become more prominent in the US.

Meanwhile, China’s economic recovery remains uninspiring and easy monetary policy continues to present a yield disadvantage to yuan vs. USD. While there are some early indications of economic data out of China starting to improve with August credit data on an uptick and August CPI suggesting an exit from deflation, there could be seasonal factors at play here. A firmer recovery in the economy will be needed to make the gains in yuan sustainable. Until then, weaker yuan is also helping China maintain its export competitiveness in competition to the weakness in Japanese yen as well.

The Bank of Japan has been somewhat active in the third quarter to defend the yen and also hinted at bringing forward the timeline of exiting the negative interest rate environment. However, unless we see clearer signs of a policy tweak, fundamentals remain misaligned to the rhetoric. This means any appreciation bias in the Japanese yen would remain short-lived.

These heavy-weight underperformers in the currency markets continue to point to more upside for the dollar. But gains from here will be harder to come by. There will be some downward pressure from AUD and NZD if commodity prices and risk sentiment continue to remain supported. High-beta currencies like the Swedish krona could also see some momentum. Chinese authorities are also showing more commitment to yuan stability. Meanwhile, continued tightness in the oil markets could push Brent towards the $100-mark in the short-term, and that could bring the CAD higher.

Meanwhile, the EM rate cut cycle has begun, and aggressively at that. Brazil, Chile and Poland have started to cut rates in the third quarter, and the pace of rate cuts has been an aggressive surprise. While such sharp rate moves could destabilise EM currencies, one would expect the rate cuts from here to remain more modest if the Fed continues to preach higher-for-longer. This could mean EM carry would remain interesting, especially for Latin American currencies, and could bring upside in BRL and MXN. Mexico could also benefit from the US growth, but some near-term pressure on the currency could come from Banxico’s plans to unwind its FX forward book, which would mean dollar buying. Asian currencies could continue to be under pressure until CNY appreciation fades, but strength could return to INR after it has reached a record weak level in September, on strong domestic growth and increasing capital flows, provided inflation spikes remain temporary.

When dollar reigns, all else fails

A strong dollar makes a tough market, tougher. The third quarter brought about some warnings from policymakers where economies and currencies are getting hit the most due to the dollar strength. Both China and Japan appear to be getting concerned about the depreciation in their currencies, as they are not at a point in the economic cycle where their monetary policy and yield directions can follow that of the US. For others like the Eurozone or the UK, the rise of the US dollar is threatening their inflation-fighting capability and forcing them to raise rates further, which is putting their economies on the brink of a recession or stagflation. But is a coordinated central bank intervention like the 1985 Plaza Accord possible? We think not, because at that time the US wanted a weaker dollar and joined in the coordinated response, as a strong US dollar was weakening its export competitiveness. However, the scenario has flipped now with a strong dollar aiding the Fed’s inflation fight, and thus a coordinated effort to weaken the dollar may be unlikely.

De-dollarisation expectations, meanwhile, have also been pushed forward by several years especially with the BRICS expansion from next year, which made us beg the question as to whether it will bring more coordination or chaos. Any alternatives to the US dollar could only remain useful at best for trade within the expanded BRICS, but it remains tough to see any real threats to the USD’s global trade and reserve currency status for the foreseeable future.

As an investor, one needs to remain cautious of the impact of a strong dollar on their portfolios. Here are a few considerations:

- A strong US dollar weighs on the earnings of US companies that have a large presence in international markets. The S&P 500 generates about 30% of revenues outside of the US. This partly explains why the dollar is inversely correlated to US equities or risk assets in general.

- From a macro lens as well, a strong US dollar could mean reduced exports, and hence a slower economic growth in the US.

- Many emerging markets could also be destabilised, as the burden of their USD-denominated debt increases, and this raises the risk of a default for the more vulnerable frontier economies such as Sri Lanka.

- Most commodities, such as crude oil, are denominated in the USD. So, a strong dollar can cause a decline in commodity prices.

To hedge or not to hedge

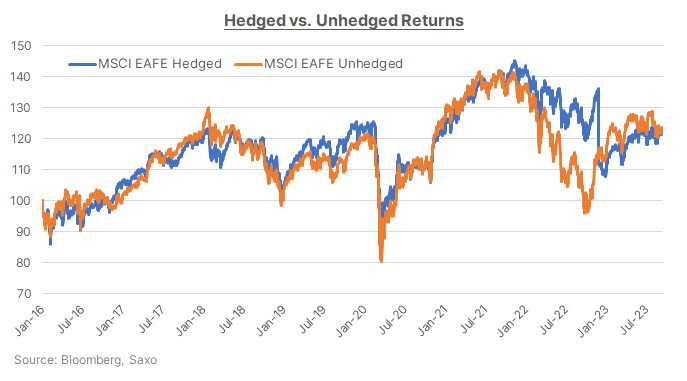

Market participants with a high exposure to USD assets, but with a bearish view on equities and looking to hedge their portfolios could consider being long US dollar as a safe-haven. However, it is worth noting that this may be more suited for traders with a short-term view, as returns from hedged and unhedged products tend to be the same over a longer horizon. Also, it is worth noting that the wide interest-rate differentials between the dollar and other currencies make hedging costly for Asian and European investors today. The decision to invest internationally in a well-diversified portfolio could be more relevant for portfolios than the decision to hedge.

US-based investors may be facing a weak performance of their non-US investments. This could mean they shift their focus to domestically-exposed US companies, primarily the small and medium-size corporations or in sectors like real estate or utilities compared to large caps and tech or consumer names that have more international exposure.

For non-US based investors, adding to US exposure is getting expensive and local opportunities may be more attractive and affordable, which could weaken fresh flows into US assets.