World’s First Risk Management Blockchain Protocol for the Masses.

By Finamatrix (FIX) A.I. – Empowering You with AI.

Best A.I. Technology Firm 2018 Award.

This technical paper supports the white paper available at Finamatrix.com.

A decentralized and indestructible risk-reduction protocol integrated on the plethora of qualified Blockchains, implementing Genetic-Algorithm Neural-Network (GANN) Risk-Cybernetics powered by Atomic Portfolio Selection (APS) and MVSK Utility Optimization, for autonomous and instantaneous liquidity provision in assets including FX, cryptocurrencies, etc. on an open-source API high-frequency options trading exchange for volatility-arbitrage, delta-neutral and delta-hedged portfolios operated by institutions or individuals.

Dr. Lanz Chan, Ph.D.

Founder & CEO, Finamatrix AI (Singapore)

Chair Professor Dr. Alan WK Wong, Ph.D.

FinTech & Big Data Research Center, Asia University, Taiwan.

Abstract

For the past 11+ years, Finamatrix has received requests to offer our close-sourced AI technology to the masses. For the first time, we develop a volatility arbitrage (vol-arb) trading system on an open-source API digital mutli-Blockchain exchange with our risk-cybernetics protocol.

By providing multiple linkages with global assets including FX, crypto-currencies, etc to our FIX digital exchange, we offer a new and reliable set of implied volatility statistics to the public for the pricing of both call and put options on multiple assets. The FIX cryptocurrency shall power the FIX digital exchange.

To perform vol-arb, a trader must first forecast the underlying asset’s future realized volatility by computing historical daily returns for the past x days. The implied volatility provided by FIX digital exchange shall offer anyone up to 75% probability of obtaining a profit, providing an edge to the public.

Introduction

At the heart of FinTech is risk management, which has been a strong driver for institutional decision-making since time immemorial. With the advent of Blockchain technologies, the development of automation in transactions for the transfer of assets, and in risk management protocols, etc are made possible.

2017 was marked by a turning point in the growth of the crypto markets as more institutional investors looked to gain exposure in digital cryptographic assets. Blockchain offers a system for the seamless transfer of wealth. FIX is positioned to be the leading risk management protocol for Blockchains.

By developing the FIX digital exchange, we access liquidity pools all over the world, and offer immediate pricing, settlements, with multiple-option terms.

FIX Digital Exchange offers the following features:

-

Decentralized risk management infrastructure.

-

Volatility-arbitrage portfolio construction with 1000+ assets.

-

Digital asset options-pricing big datasets and databases.

-

Fair access to risk-reduction protocol.

-

Atomic (small, indestructible) portfolio selection solving the problem of selection bias.

-

Instantaneous liquidity and immediate transactions.

-

Complete trustless automated liquid exchange.

-

Available universally and highly transparent.

-

Total privacy, decentralized ledger.

-

Incentive layer with FIX crypto. Fund deposit provides both fiat plus FIX crypto.

-

Zero risk of asset theft, DDoS attacks, Sybil attacks, confiscation or possibility of interference.

-

Responsible KYC/AML procedures to fund account with fiat or crypto.

-

Up to 75% of traders will reap profits from liquidity pool.

-

Lowest transaction fees for risk-hedging option-trading platform.

Roadmap

-

1st Quarter 2018: Testing of FIX Digital Exchange

-

2nd Quarter 2018: Roll out of FIX Digital Exchange

-

3rd Quarter 2018: Open-source API connectivity with any digital asset.

-

4th Quarter 2018: Further enhancements.

FIX Risk-Cybernetics Protocol

The Portfolio of Digital Assets including FX, Cryptos, etc on the FIX digital exchange is powered by:

Atomic Portfolio Selection (APS) under MVSK (Mean-Variance-Skewnes-Kurtosis) Utility Optimization.

The quadratic utility algorithms are as follows:

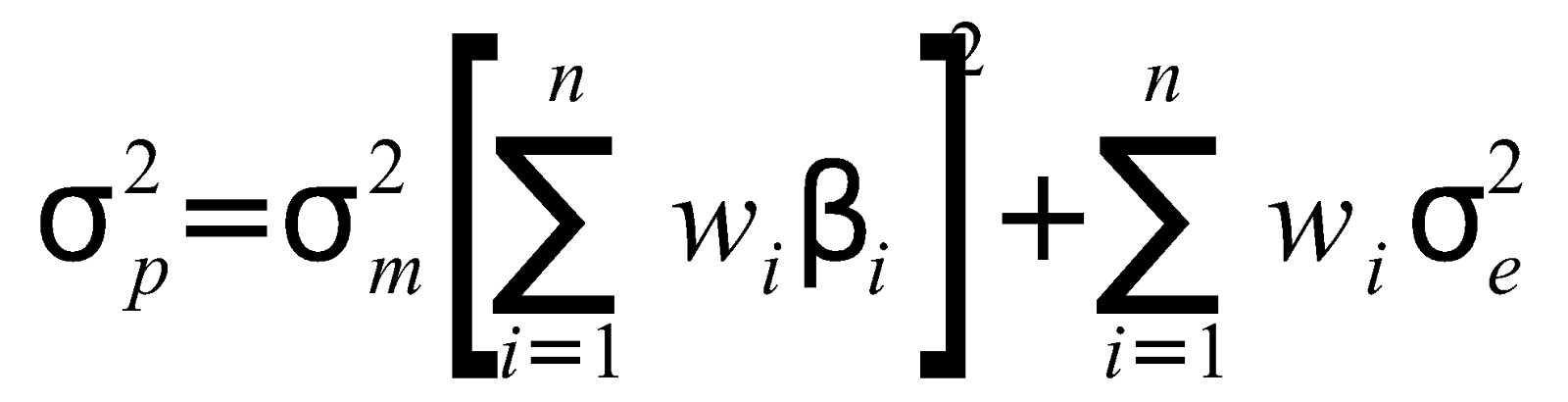

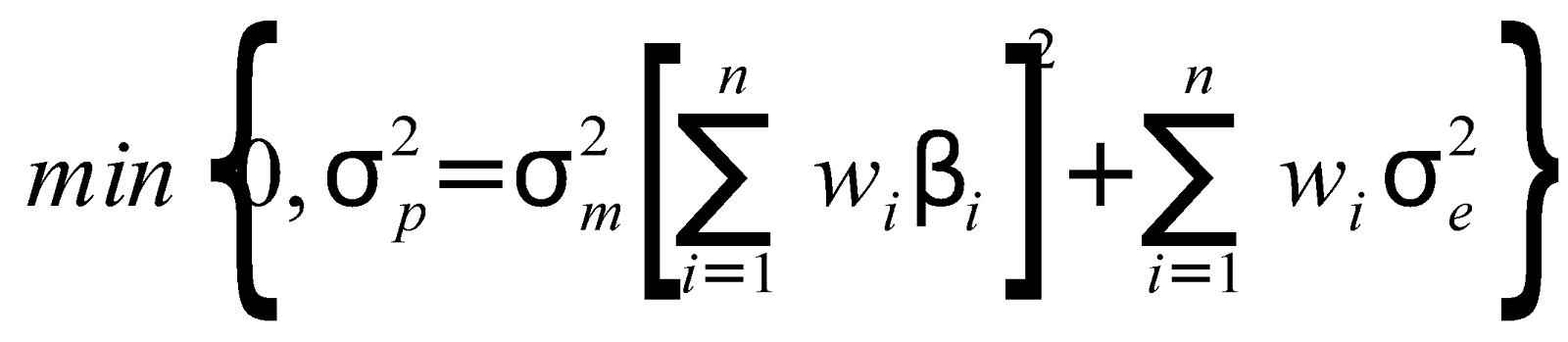

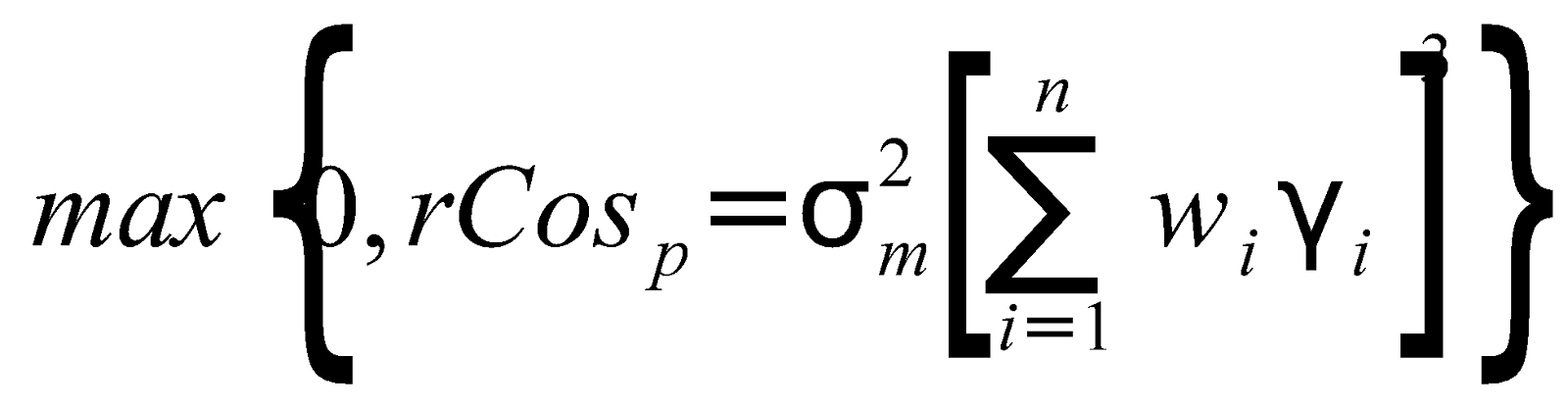

Portfolio-Variance:

whereis market variance,

![]() is the individual asset i weight,

is the individual asset i weight,![]() is beta of asset i and

is beta of asset i and![]() is the residual variance.

is the residual variance.

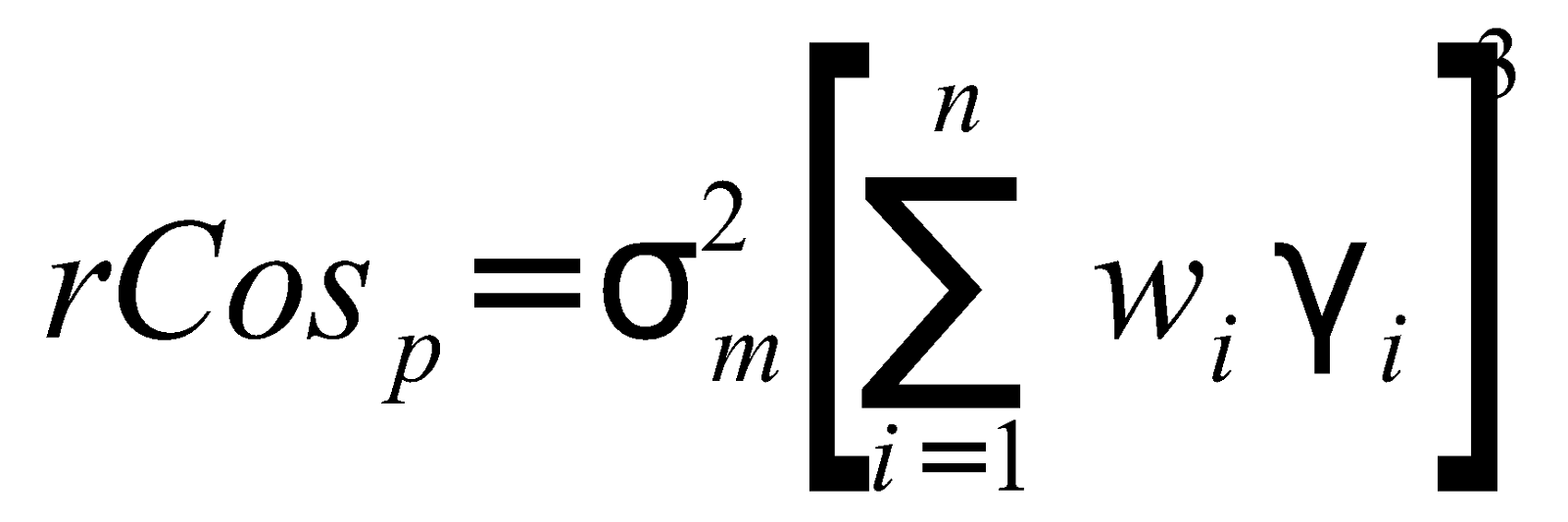

Relative-Portfolio-Coskewness:

where![]() is market variance,

is market variance,![]() is the individual asset i weight,

is the individual asset i weight,![]() is beta of asset i and

is beta of asset i and![]() is the coskewness estimate of asset i. The

is the coskewness estimate of asset i. The![]() is a risk-preference parameter that adds skewness to the market portfolio.

is a risk-preference parameter that adds skewness to the market portfolio.

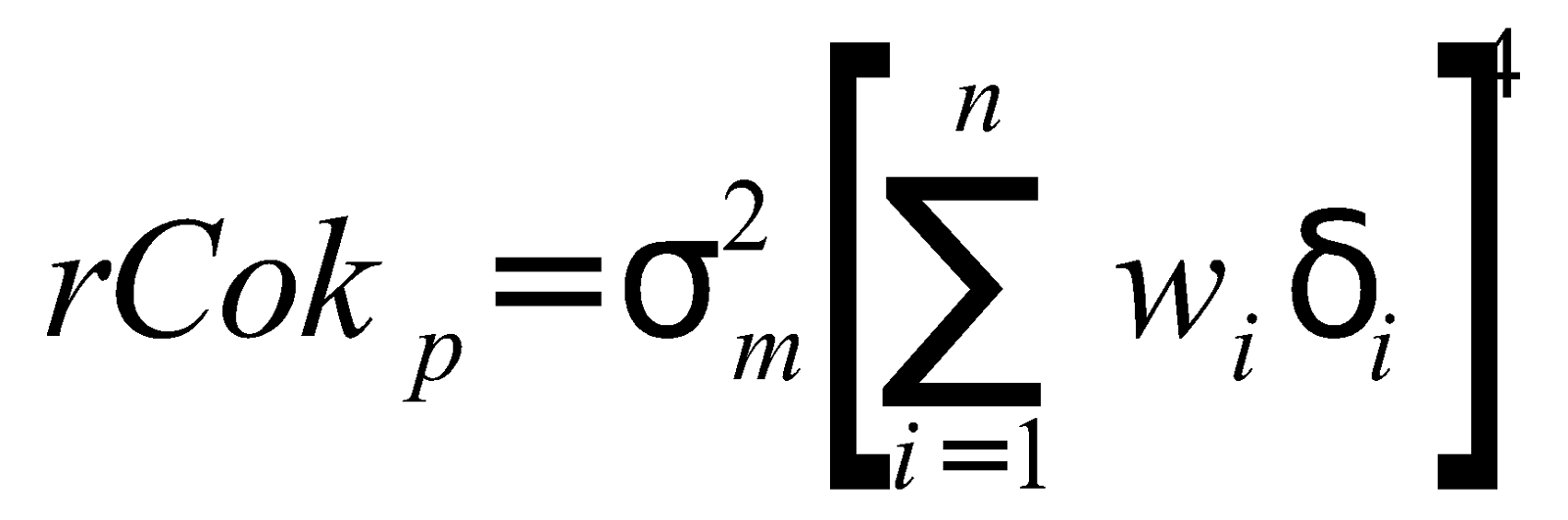

Relative-Portfolio-Cokurtosis:

where![]() is market variance,

is market variance,![]() is the individual asset i weight,

is the individual asset i weight,![]() is beta of asset i and delta,

is beta of asset i and delta,![]() is the cokurtosis estimate of asset i. The

is the cokurtosis estimate of asset i. The![]() is a risk-preference parameter that adds kurtosis to the market portfolio.

is a risk-preference parameter that adds kurtosis to the market portfolio.

Maximized returns:

or

Minimized variance:

Subject to the simultaneous constraints of:

The risk-preference parameter, given by

and the risk-aversion parameter, given by

The Random Parameter Optimization Engine for the FIX digital exchange is:

Optimization function operationalized on the Golden Ratio (GR),

where,![]() and segments a and b are:

and segments a and b are:

a = | minimum price – mean price |

b = | mean price – maximum price |

where a>b : hypothesized ratio=1.618

where b>a : hypothesized ratio=0.618

We calculate the Gold Ratio Estimator (GRE) where GRE = GF/GR

and GF is the Genetic-optimization Factor (GF) result between 0 to 1.618 under x constraints, where x are a set of parameters obtained from liquidity pools statistics.

Conclusion

It is envisaged for the FIX digital exchange to satisfy the growing requirements of volatility-arbitrage and delta-hedged option portfolios in the total portfolio of both institutions and individual traders.

References:

Chan, Lanz, Atomic Portfolio Selection: MVSK Utility Optimization of Global Real Estate Securities (June 16, 2004). Finamatrix, July 2011. Available at SSRN: https://ssrn.com/abstract=1744802

Chan, Lanz, Machine-Learning Fully Automated FX Trading System for Superior Returns with Risk Cybernetics Artificial Intelligence Framework (May 22, 2015). Available at SSRN: https://ssrn.com/abstract=2609630

Chan, Lanz and Wong, Wing-Keung, Automated Trading with Genetic-Algorithm Neural-Network Risk Cybernetics: An Application on FX Markets (February 20, 2012). Finamatrix Journal, February 2012 . Available at SSRN: https://ssrn.com/abstract=1687763

Gikhman, Ilya I., Stock, Implied, Local Volatilities and Black Scholes Pricing (July 31, 2017). Available at SSRN: https://ssrn.com/abstract=3011435 or http://dx.doi.org/10.2139/ssrn.3011435

Jablecki, Juliusz and Kokoszczynski, Ryszard and Sakowski, Pawel and Slepaczuk, Robert and Wojcik, Piotr, Options Delta Hedging with No Options at All (October 11, 2014). University of Warsaw Faculty of Economic Sciences Working Paper No. 27/2014. Available at SSRN: https://ssrn.com/abstract=2508639 or http://dx.doi.org/10.2139/ssrn.2508639

Joenväärä, Juha and Nguyen, Lien, Exploiting ‘Risk’ in Risk Arbitrage: Evidence from Option Holdings of Risk Arbitrageurs (January 23, 2018). Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3107499

https://www.research.ibm.com/ai/