Dealing with unexpected medical bills can be quite stressful. Healthcare costs keep rising. Many Americans struggle to pay for procedures, treatments, and prescriptions. When savings and insurance fall short, medical loans may provide necessary financial help.

Understanding Medical Loans

Medical loans help cover healthcare expenses that insurance does not pay for. These loans enable you to finance essential medical procedures and gradually repay the debt. You can also pre-qualify for a personal loan to help cover any medical costs.

Medical loans must be used exclusively for healthcare expenses, unlike traditional personal loans, which can be used for various purposes. Since the healthcare provider secures them, they also tend to have lower interest rates.

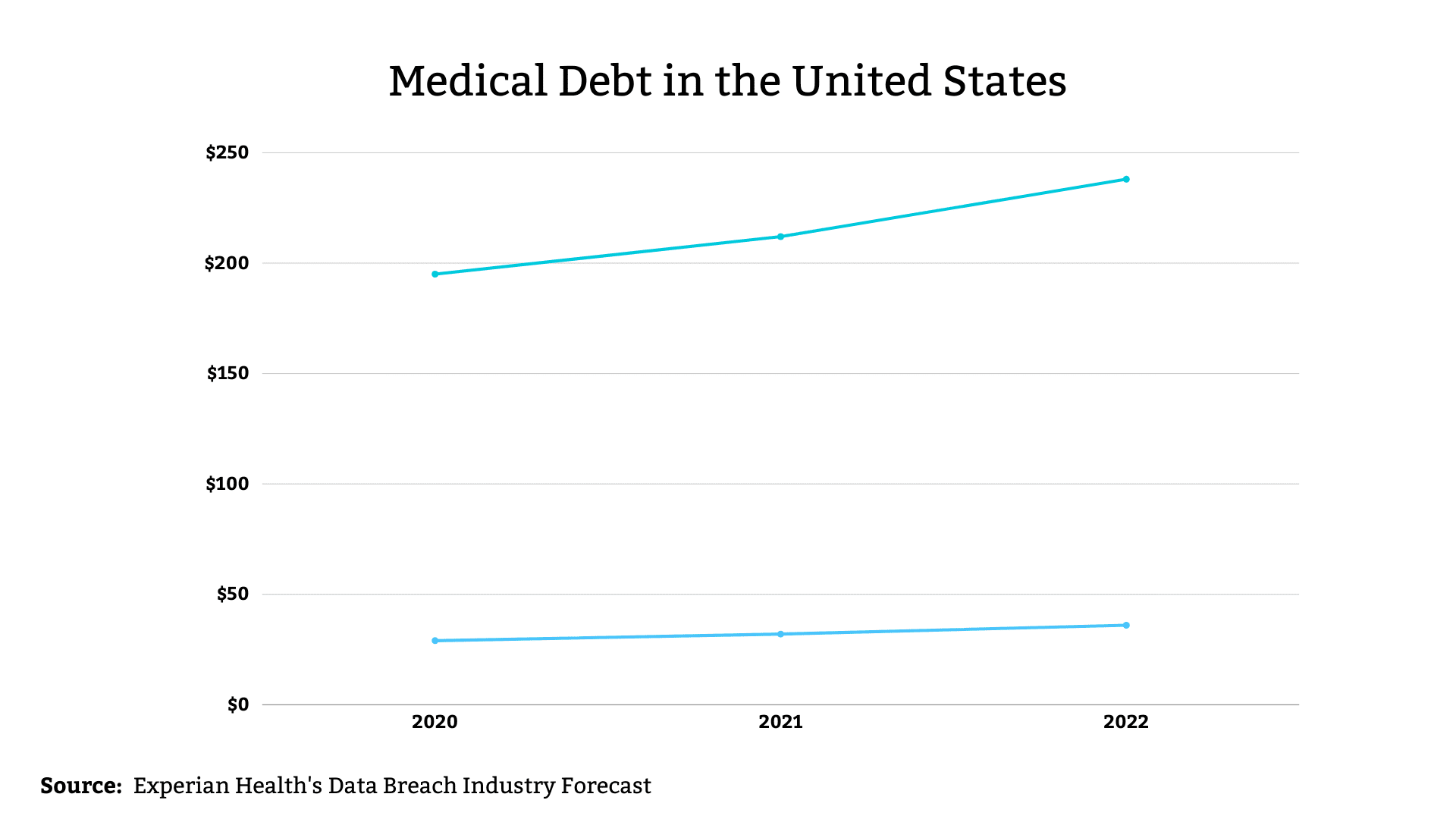

To qualify for most medical loans, good to excellent credit is often required. But, some providers offer medical loans for those who may not meet all credit requirements as well. Currently, there is a staggering $88 billion in medical debt impacting consumer credit reports, highlighting the widespread demand for medical financing assistance.

Advantages of Opting for Medical Loans

Instant access to funds: A primary advantage of medical loans is their immediate access to funds, allowing you to receive prompt treatment. This is especially helpful for pressing procedures like surgery when timing is critical.

Funding electives: Medical loans finance elective treatments. These include LASIK eye surgery, dental work, fertility treatments, and cosmetic procedures. They aim to improve the quality of life. Without financing help, these procedures could be unattainable for some patients.

Dealing with unpaid medical bills: At present, 30% of millennials are grappling with outstanding medical debt. This data underscores the growing requirement for responsible financial solutions when it comes to covering essential healthcare expenses.

Prevent the progression of the condition: Healthcare issues sometimes worsen without timely diagnosis and treatment. The ability to finance expenses aims to prevent conditions from progressing. This can reduce suffering and long-term effects when care is not delayed.

Responsible Cost Sharing: For treatment options that are not covered by insurance, service centers often have co-lenders that specialize in affordable financing. These partnerships aim to make treatments more accessible through responsible lending practices.

Finding the Right Medical Loan

Research Multiple Sources: Banks, credit unions, and online lenders offer various medical lending options to patients. Healthcare systems and providers themselves also offer these options. With many potential sources available, research helps find the best rates and terms for each patient’s unique situation.

Hospital Lending Programs: Half of U.S. hospitals offer lending programs, loans, or payment plans to help patients manage expenses. This provides a helpful internal financing option for care. Some facilities even offer no-interest loans based on financial need to increase access.

Affiliated Lenders: For elective treatments not covered by insurance, such as plastic surgery or extensive dental work, many provider offices have affiliated lenders that may help finance expensive procedures. These partnerships aim to make treatments attainable through responsible lending.

45% of Americans currently have or have had outstanding medical debt. This widespread percentage shows why medical lending options could benefit many patients and providers.

Understanding Medical Loans with Less-Than-Perfect Credit

Individuals with credit scores below 600 may still be approved for medical loans. But, in these situations, interest rates could be much higher. This can make paying off debt more challenging.

Before applying, medical loan candidates should check all three credit reports and scores. This will help them understand their current standing. Comparing options helps find the best rates possible. This is for those who may still need to meet all credit requirements but still need necessary healthcare.

You can get approved for a medical loan with poor credit. But, this often requires persistence to secure better rates. Meeting with financial advisors also helps borrowers consider all alternatives.

Key Factors to Consider Before Choosing a Medical Loan

Interest Rates and Loan Costs: Higher interest rates can make medical loans expensive for a long time. So, candidates should optimize for the lowest rate available. This may need a longer repayment term. Considering potential impacts over the full lifetime of the loan helps make informed borrowing decisions.

Negotiating Extended Payment Plans: Patients should also consider negotiating extended payment plans with healthcare providers as their first option before exploring other alternatives. You can also apply for Medicaid or financial assistance programs that fit your eligibility criteria. This can help reduce your reliance on loans.

Evaluating the Optimal Loan Amount: 6% of U.S. adults currently owe over $1,000 in medical debt. Evaluating the optimal loan amount needed, all fees involved, the monthly payment schedule, early payoff options, and total interest costs helps patients make responsible borrowing choices.

Accelerated repayment option: Some medical loans may offer an accelerated repayment option, allowing borrowers to repay the loan before the end of the specified term. It is important to ask about and consider such options when negotiating loan terms. Faster payments can save interest and resolve the debt faster.

Total interest charges: Patients should get a clear idea of the total interest charges associated with medical expenses. This includes the interest rate over the life of the loan. Knowing all interest rates allows borrowers to make informed decisions about whether a loan is the right financial option for their particular situation

Pros of Medical Loans

Access funds without requiring collateral: Medical loans allow access to finance without collateral. Borrowers do not have to put up valuable assets to secure the loan, making it a convenient, risk-free financing option.

Available even with average credit scores: Medical loans for individuals with average credit. This inclusion ensures that people with different credit histories can qualify for funding and provide the financial support they need for their medical needs

Lower rates than other financing options: Compared to some other financing options like credit cards or personal loans with higher interest rates, medical loans tend to offer lower interest rates This lowers the overall cost of borrowing and provides a cost-effective way to manage healthcare costs.

Conclusion

Many Americans associate medical expenses with financial stress. While medical loans provide important support, potential borrowers need to consider costs and explore options before committing to a loan. Responsible financial management includes considering 0% interest rate plans, financial assistance programs, Medicaid, and medical credit cards as viable options for managing health care costs These options can remove the financial burden and avoid excessive debt. Medical loans should be a last resort, ensuring timely treatment without compromising financial stability. Making the right choices when it comes to healthcare finances is important for financial well-being and access to necessary medical care.