After experiencing a three-month downturn, the cryptocurrency market has finally reached a strong rebound. While the confidence is gradually recovering, investors are becoming more rational, which is reflected in their preference for more practical applications.

We Credit Tag Limited, a tech startup headquartered in Singapore, recently launched Credit Tag Chain (CTC) – a blockchain-based global credit asset value network that is designed to break the development bottleneck of the traditional credit industry. Unlike many other proposed solutions for credit business, CTC seems to be more focused on the application of real business scenarios rather than ICOs.

The global credit industry has flourished in recent years under the growth of mobile internet. Many country’s population have experienced the benefits of the Inclusive Finance. However, as the scale of transactions continues to climb, and due to the limitation of current personal credit systems, more and more maladies start surfacing: increased risks of delinquency of long-term loans, information silos on credit records, etc. As a result, more qualified borrowers are not able to obtain loans and credit industry will face higher liquidity risks.

In a recent sector in-depth report, Moody’s analysis showed that the blockchain technology can reduce the cost of the US mortgage industry by 0.84 to 1.7 billion dollars annually. The researchers wrote that since the financial crisis, many industries have carried out technological innovations, except that the mortgage industry has not yet changed much. Blockchain technology provides the credit industry with a huge opportunity to simplify the mortgage process while addressing the high costs and complex process issues.

The technical white paper of the Credit Tag Chain (CTC) shows that by maximizing the advantages of the smart contract on the blockchain, CTC can autonomously direct the flow of crypto-currency for mortgages, and establish a completely trusted value network between borrowers and credit institutions. At the same time, with its established credit resources in countries such as China, Indonesia and Vietnam, CTC is expected to be the first disruptive innovation on lending in the Asia Pacific region.

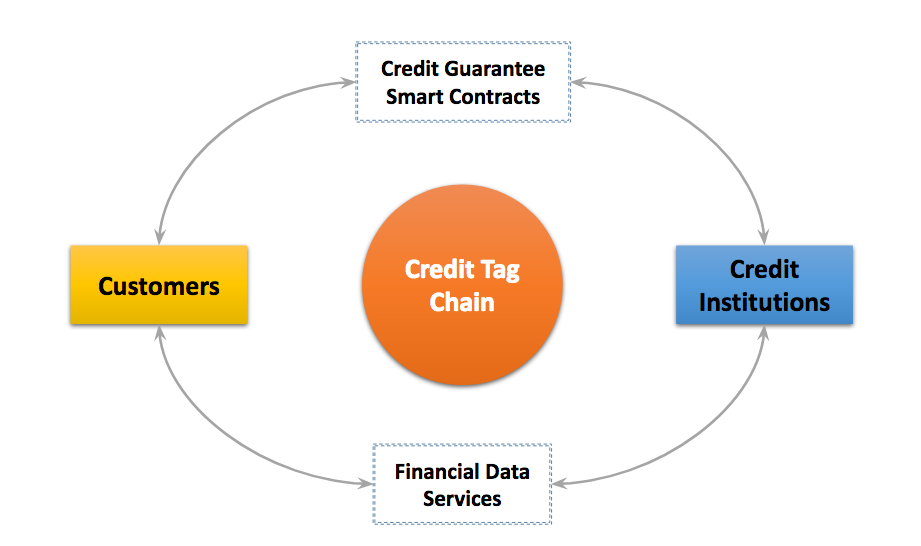

CTC’s Smart Contract for Secured Loans and Lending Information Stored on Blockchain

In simple terms, the business logic of CTC is as follows: borrowers freeze a certain amount of CTCs (TOKENs) through smart contracts to obtain loans from credit institutions. The data on borrowing behaviors generated by users will be registered through smart contracts to help build their own credits. Different credit institutions can query each other’s credit records through blockchains to increase the credibility of users’ data and greatly reduce risks. At the same time, CTC will also make data inquiries more accurate, more convenient, and more secure through privacy protection mechanisms. If the CTC network can be successfully deployed and implemented for both credit guarantee and credit data query, it will bring more stimulus in demands to the entire credit industry.

Nigel, one of the co-founders of the CTC with financial and blockchain technology background, said that the CTC network will bring more far-reaching impact to the global credit industry from the following aspects:

First, the loan service will be more convenient to the borrowers, because CTC is a decentralized service network, smart contracts make the lending relationship between borrowers and credit institutions more intuitive, transparent, and harder to tamper with.

Second, credit institutions can serve a wider range of people. Through the distributed credit network, CTC helps all borrowers build their record scores, resolve information asymmetry between lending institutions, and thus scale credit industry.

Third, more innovative models will emerge. CTC will eventually establish a mutually beneficial ecosystem for borrowers and credit institutions. In the future, both B2C and C2C can operate without any differences on the same network. Cryptocurrency, as an important asset form, will also provide growth drivers for this ecosystem.

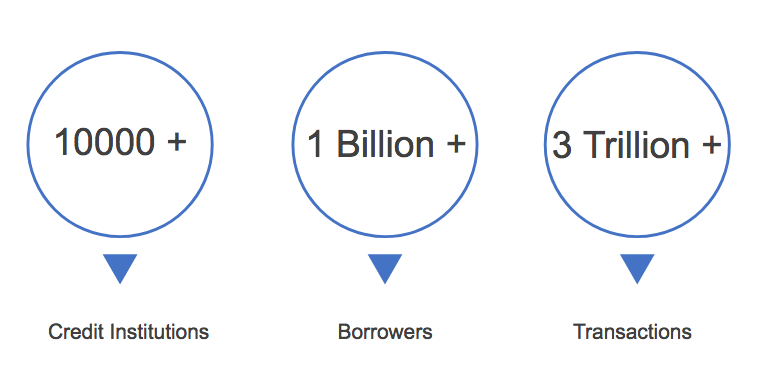

CTC network will face the global credit market of 10,000 credit institutions, 1 billion borrowers and 50 trillions transactions

By the end of 2017, there are more than 10,000 credit institutions globally, the total number of borrowers has exceeded 1 billion, and the market cap of the credit industry is more than $20 trillion. With the expectation of hitting record high in the second half of 2018, the overall credit transaction volume will go beyond 50 trillion.

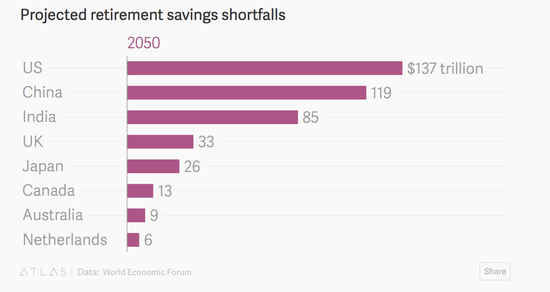

The World Economic Forum (WEF) predicts that by 2050, the world will face a shortfall of $400 trillion in retirement funds, of which the United States will account for $137 trillion US dollars and China will account for $119 trillion.

Thus reliance on credit services has increasingly become a means of cash flow used by ordinary people. Being the world’s 4th most populous country, for example, Indonesia’s 265 million population has attracted many financial companies with its openness to credit services and FinTech-friendly regulations. However, the lack of its personal credit information has made it very difficult to get loans. And this is where CTC’s innovative lending model comes in and make a big impact.

The CTC network has already initialized its operation. In the coming months, they will create an online lending process across several companies in Southeast Asia using its blockchain and smart contracts technology, which will bring significant benefits to the credit industry.