Car prices have never been higher in the United Kingdom. Many people yearn for new cars with the latest gadgets and features. Unfortunately, the cost of new cars is astronomical and out of the reach of millions of consumers. It also does not help that new cars usually depreciate by up to 40% within the first year of ownership.

That is why an increasing number of consumers are choosing to buy used cars to save money. After all, used cars have already depreciated enough to cost far less than new cars without sacrificing their functionality and longevity. In fact, a well-maintained used car can last you many years.

Why Used Cars Can Save You Money

Used cars are more affordable than new cars because they have a depreciated value from their original value. The age and amount of depreciation are the factors that influence the price of a used car. If you buy a vehicle that is only 1 to 3 years old, it will still have lost a significant portion of its original value, which means you can find a good price for it.

Now you may think that buying a much older car will result in even greater depreciation and a much lower price tag. While that may be technically true, you must consider the potentially expensive repair costs associated with older cars. A car over 5 years old is likely to be severely degraded, depreciated, and neglected.

On the other hand, a used car that is no more than 1 to 3 years old will likely require fewer repairs, especially if the mileage is under 50,000. The result is fewer repair costs and a lower tag price.

How to Save Money on a Used Car with PCP Financing

Most consumers look for used cars with the lowest price tags to save money. However, there are many more effective strategies for saving money on used vehicles besides comparing price tags. The most effective strategy pertains to car finance.

The way you finance your car purchase has a significant impact on the total cost. You may believe a hire purchase (HP) agreement is the best way to buy a car because the monthly payments cover the full cost of the vehicle over time. The only problem is that HP agreements have high monthly payments.

A personal contract purchase (PCP) is a more cost-effective option if you want to save money on your monthly payments. You make the initial deposit and then make low monthly payments that cover the depreciated value of the vehicle rather than the total cost. When you come to the end of your PCP contract term, you can either pay a balloon payment to own the vehicle, trade in the car for another one, or return the car altogether.

The balloon payment option to keep the car is the most expensive choice due to the interest accumulated over the contract term. You are much better off trading it in for another vehicle to maintain lower monthly payments without any big payment obligations. It can provide a low-cost opportunity to try out some newer used cars, no more than one or two years old.

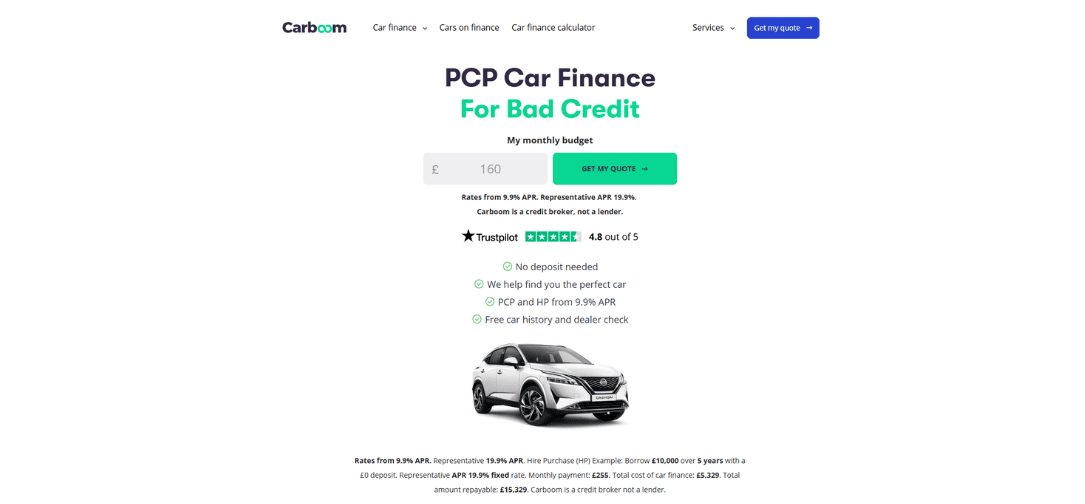

Visit Carboom.co.uk to learn more about how to obtain PCP car financing, even when you have bad credit.

How to Maximise Savings on a Used Car

Would you like to learn some of the other effective strategies for maximising your savings on a used car purchase? Here are the top five tips below:

1) Compare Finance Rates

Every car finance service will offer slightly different interest rates and monthly payment terms. Requesting price quotes and comparing the various rates can help you find the one that best fits your budget. Even a slight 1% APR difference could go a long way in saving you hundreds of pounds or more over the term of the agreement.

2) Buy an Almost New Used Car

Used cars that are less than three years old typically have reduced prices, modern features, and fewer repair costs. Some may even come with manufacturer warranties to cover the cost of any potential repairs within a specific period. It is the best option if you’re seeking long-term financial security, although it comes with a slightly higher monthly payment.

3) Negotiate with the Dealer

Car dealers are usually quite eager to sell their cars, so they are more than willing to negotiate a fair price that matches your budget. If you can manage to negotiate a lower purchase price, it means you will also borrow less money to finance it. Borrowing less money means lower interest payments and more cost savings.

4) Higher Valued Used Cars

Search for higher-valued used cars with less depreciated value. They can often result in PCP finance terms with lower monthly payments because there is a smaller difference between the car’s purchase price and its guaranteed future value (GFV). You may even be able to negotiate a lower balloon payment at the end if you work something out with the dealer.

5) Buy on a Holiday or Special Occasion

Many car dealers have discount sale promotions running on holidays and other special occasions in the UK. That makes it the perfect time to consider purchasing a used car, as you can take advantage of these rare deals before they expire. Check out local internet ads or dealership websites to find these deals in your area.

Conclusion

Financing a used car is one of the smartest decisions you will ever make if you are looking to save money. Then, you can implement other effective strategies to maximise your cost savings, such as budgeting for added expenses and reviewing the vehicle’s history. All these strategies play a role in how much money you will save in the short-term and long-term.

Get a Quote for PCP Car Finance with Bad Credit

Don’t forget to check out Carboom.co.uk for affordable monthly premium rates on PCP car finance. They will even accept a client with bad credit and help them find a perfect car on a PCP agreement with an APR of at least 9.9% or higher.