Over the past decade, Germany, long hailed as Europe’s industrial stalwart, has experienced a striking rise in the number of companies registered under foreign ownership. According to data published by CompanyData.com, the number of foreign-owned companies in Germany soared from approximately 20,612 in 2015 to 145,411 in 2025, representing an increase of 605.5 %.

This dramatic uptick signals more than simply statistical growth. It points to a structural reorientation of Germany’s economy: from purely domestic industrial strength to a more globally integrated, cross-border ownership model that blends manufacturing, services and digital infrastructure. The story has multiple dimensions: where the capital is coming from, which sectors are being targeted, and what the implications are for Germany’s famed “Mittelstand” and for foreign investors alike.

The Numbers Behind the Surge

In 2015, foreign-owned firms in Germany numbered roughly 20,612. By 2025, that figure had ballooned to 145,411. That translates to a six-fold increase, underscoring the shift in investor perceptions of Germany, not simply as a safe haven, but as a dynamic gateway into Europe’s single market.

Some specific country-of-origin data stand out:

- Luxembourg remains the largest single source: foreign-owned companies rising from 2,534 in 2015 to 18,990 in 2025.

- England (i.e., UK-based investors) saw their number of German-based companies grow from 1,646 in 2015 to 15,568 in 2025, a growth of 846 %.

- China (Chinese-owned firms in Germany) increased from 399 to 3,253 in the same period, a rise of 715 %.

These numbers show both the steady dominance of traditional European cross-border flows (Luxembourg) and the marked acceleration of newer sources (UK, China).

Sources of Investment: Who’s Driving It?

Luxembourg: The Established Leader

Luxembourg’s position is noteworthy not simply for the volume but for the continuity. Its proximity, both geographic and institutional, to Germany helps explain why it remains the largest single source of foreign-owned companies in Germany. Long-standing business links, favourable tax/regulatory arrangements and the ease of cross-border structures all play a role.

England (UK): Post-Brexit Momentum

The UK’s leap, from 1,646 in 2015 to 15,568 in 2025, represents almost a ten‐fold increase. Post-Brexit strategic repositioning appears to be a significant driver: UK firms seeking a foothold within the EU have looked to Germany as the “entry hub” into Europe’s single market. The rise of UK-based registrations in Germany supports this interpretation.

China: Industrial & Strategic Presence

Although China ranks just outside the top-10 in count (11th place), its 715 % growth is telling. Chinese investment in Germany is increasingly focused on manufacturing, logistics and infrastructure, an example being the European battery plant of Contemporary Amperex Technology Co. Limited (CATL) in Arnstadt, Thuringia, and the minority stake of COSCO Group in Hamburg’s Container Terminal Tollerort. These are concrete manifestations of China’s deeper industrial link-up with Germany.

United States: Digital & Cloud Infrastructure

US companies are less prominent in the numbers above (count of companies) but deeply influential in strategic sectors (tech, cloud, AI). For example:

- Microsoft Corporation’s announced €3.2 billion programme to expand AI and cloud infrastructure in Germany.

- Amazon Web Services (AWS) plans a €7.8 billion investment in the European sovereign cloud, with Germany’s Brandenburg region as a key site.

These strategic bets highlight that foreign-ownership in Germany is not merely about quantity of companies, but about strategic depth in sectors that are shaping the future.

Sectoral Profile: Where the Investment Lands

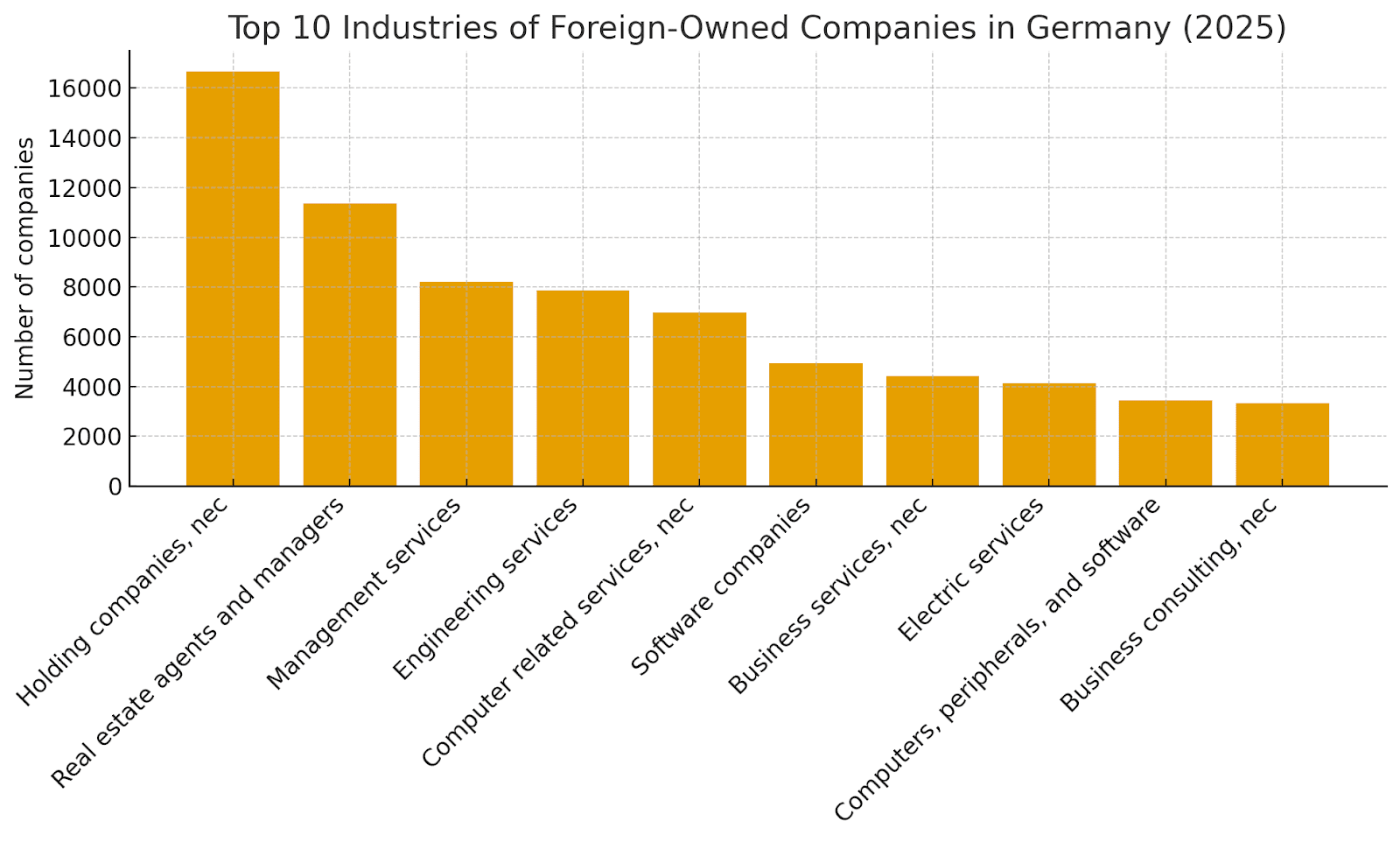

The surge is not evenly spread across sectors. According to CompanyData.com’s 2025 snapshot, the leading industries among foreign-owned companies in Germany are:

- Holding companies: 16,681

- Real-estate activities: 11,359

- Management services: 8,193

- Engineering services: 7,853

- IT / Computer services: 6,983

- Software companies: 4,944

What’s striking here is the combination of traditional “shell” structures (holding companies), real-estate and management services, with highly growth-oriented segments: engineering, IT, software. This points toward a dual trend: foreign capital exploiting Germany’s stability via holding/real estate vehicles, and concurrently targeting its industrial-digital core for growth.

Why Germany? The Pull Factors

Several forces help explain the attractiveness of Germany to foreign investors:

- Economic anchor and market access

Germany is often viewed as Europe’s industrial and economic anchor: a stable platform with deep-skilled workforce, strong infrastructure and access to the EU internal market. This makes it attractive for firms wanting a strategic hub within Europe.

- Post-Brexit repositioning

For UK companies, Germany offers a means to retain EU market access while leveraging a robust German environment.

- Industrial transformation and digitalisation

Germany’s Mittelstand (small and medium enterprises) is undergoing transformation, digitisation, automation, shift toward software and engineering services. Foreign investors see an opportunity to participate in this evolution. - Data & transparency

In cross-border M&A and investments, the complexity of German ownership structures (especially among privately held Mittelstand firms) means that platforms like CompanyData.com offer crucial visibility, helping investors navigate ownership chains, beneficial owners and structure of subsidiaries.

Challenges & Risks

However, the growth in foreign-owned companies in Germany also comes with a set of risks and obstacles.

- Ownership complexity: Many German Mittelstand firms have intricate ownership and corporate-group structures that are opaque to external investors. This complicates due diligence and valuation. As Daan Wolff (CEO of CompanyData.com) notes: “The challenge is … identifying the right acquisition targets and understanding their ownership structures.”

- Regulatory and screening regime: Foreign investments, especially in strategic industries (digital infrastructure, energy, logistics), may come under increased scrutiny (e.g., EU FDI screening rules).

- Cultural/integration issues: Investments into Mittelstand firms, often family‐run, with long traditions, require cultural sensitivity and commitment. The target companies may not always align easily with foreign ownership models.

- Macroeconomic headwinds: While company-count data show growth, other metrics signal caution. For example, a recent report noted that foreign investment in Germany fell for the third year in a row in 2024. (Reuters) This suggests that while company registrations are up, actual investment flows may face headwinds.

Implications for Investors and the Mittelstand

For foreign investors: The German market no longer simply offers “safe but slow” growth; instead, it offers dynamic access to Europe, digital/industrial transformation, and (in some cases) undervalued firms with global potential. But success depends on rigorous data, ownership clarity and strategic alignment.

For Germany’s Mittelstand: The influx of foreign capital brings opportunity, access to global networks, digital capabilities, fresh capital. But also pressure: to evolve, to integrate, perhaps to lose family control, and to adapt to changing ownership paradigms.

Outlook: What Comes Next?

Looking ahead, the conversation with Daan Wolff suggests a few themes:

- Continued growth in technology, renewables and digital infrastructure: Germany’s Mittelstand remains attractive because it combines niche expertise with global access, and sectors such as AI, software, renewables will be focal points.

- Data analytics will become even more central: Investors will increasingly rely on AI/ML to identify which companies are ripe for investment. Platforms like CompanyData.com that provide structured, verifiable data (ownership hierarchies, beneficial owners, cross-border links) will be indispensable.

- Shift from quantity to strategic depth: Rather than simply tracking number of foreign-owned firms, the emphasis will be on quality of investment: strategic stake, growth potential, integration into global value chains.

- Potential headwinds: Germany faces macroeconomic challenges (energy costs, labour costs, global competition). Also, regulatory screening and national-security concerns may impose limits on certain types of foreign investment.

Conclusion

The increase from ~20,600 foreign-owned companies in 2015 to ~145,400 in 2025 in Germany marks not just growth but transformation. Germany is now not only Europe’s industrial anchor but a global investment platform bridging manufacturing strength, services dexterity and digital capability. The fact that Luxembourg, the UK and China have all dramatically increased their footprint underscores the global competition and opportunity at play.

Yet, numbers alone do not tell the full story. What distinguishes successful outcomes will be the ability to navigate ownership structures, align with strategic change (digitisation, renewables, services), and recognise that Germany’s Mittelstand is changing. For investors and target firms alike, data will not just support decisions; it will drive them.

To learn more about the underlying dataset and services, visit www.companydata.com.

About CompanyData

CompanyData.com is a global company data provider founded in 2013. The company has supported over 5,000 clients in 81 countries with verified, structured company data, and has been recognized as the best B2B Data Provider for its quality and reliability.