Without a doubt, one of the most stressful aspects of managing our finances is filing our taxes.

One of the biggest challenges with tax filing is calculating your finances. Part of this includes rounding the numbers up or down.

The big question for many Americans is whether you can round these numbers.

This detailed guide will show you the IRS rounding rules and a few best practices for succeeding with tax filing.

Here’s what you need to know.

The Basics of IRS Rounding Rules

You can still be susceptible to tax filing errors even after learning the IRS rounding rules. Use these rules as a basic guideline, but always consult an accountant to verify.

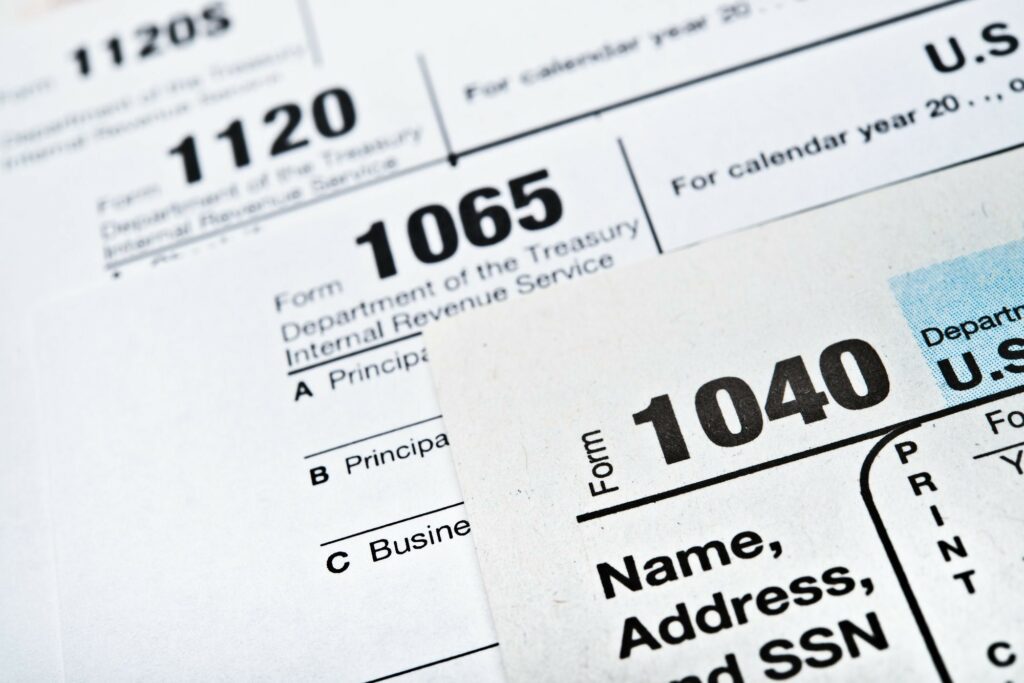

The IRS rounding rules apply to the following tax forms:

- 1120

- 1120-S

- 1065

- 1040

- 1041

You can round your numbers to whole dollars if you wish. This isn’t mandatory for any tax filing procedures. Your accountants and lawyers can suggest if this is the best decision for your financial situation.

The rules are as follows:

- If the cent amount is below 50 cents, you can round down

- If the cent amount is above 49 cents, you can round up

This means that if you have $5.49, you can round them down to $5. If it’s $5.50, you can round this up to $6.

When adding multiple amounts, keep the amount as is. Once you’ve received the total, you can round it up or down as needed. However, you can’t round each value in the sum.

Please note that your numbers will be rounded automatically when you file electronically with the IRS.

Now let’s look at some other best practices to prevent errors when filing your tax returns.

Keeping Records

Make sure you are stringent about keeping records before finalizing your taxes. In case of an audit, you’ll need to show receipts of your income and expenses.

Always take a picture of each invoice and receipt. Keep copies stored on your hard drive and a cloud drive.

As you collect these documents, you’ll want to create a spreadsheet to track your finances. You’ll give this to your accountants/lawyers when filing your taxes.

Collecting Tax Documents

The next step is to ensure that you’ve got all your tax documents at hand. Ensure you contact your employer and clients if you have not received your tax documents before the filing date.

Likewise, if you need to send tax documents, send them to your employees or contractors as soon as possible.

You’ll need W2s and 1099 forms to track your income. These official documents state how much you earned with a particular employer or client respectively.

If you notice any discrepancies, speak to your tax lawyer immediately. You may have to discuss this with your employer or client and request a new tax document.

If what you report and what the tax document states are different, there might be issues with the IRS. You may also receive forms such as 1099-INT for interest earnings and 1099-DIV for dividend earnings.

Creating Your Financial Spreadsheet

One of the easiest ways to track your finances is to use Microsoft Excel or an equivalent application.

Create two sheets, one for your income and another for expenses. In each spreadsheet, your first column should be the date. Specifically, this is when you’ve received or spent the money.

In the next column, put the total amount of the money. For this column, put the actual dollar amount rather than the IRS rounded number.

Write a short explanation of the income or expense in the third column. This can be simple as “salary” or “office equipment,” respectively.

You can also create additional columns for additional information. You can make a “Notes” column to provide details regarding each income/expense.

You can also create a category column to specify the type of income/expense. For instance, you can use categories such as “W2 salary” or “consulting fees.” Likewise, for expenses, you can use categories such as “transportation” or “software.”

If you earn and/or spend in multiple currencies, you may create an additional column specifying the amount in the original currency. However, you must always give the USD conversion to your accountant.

Make sure you have several copies of your spreadsheet at all times. Keep one on your computer and have other copies backed up on external hard drives and cloud drives.

Best Practices

Let’s end with a few best practices for filing tax returns. The first is always to be aware of deadlines. Most of us must file our tax returns on or before April 15. If April 15 falls on a weekend or legal holiday, the due date will be the next business day.

However, for some tax forms, you’ll have a different deadline. Sometimes, this falls after the standard deadline, while others are before. Failure to file on time will result in fines.

While you might not stress over the occasional small fine, it can flag you as a delinquent taxpayer if this is frequent. It’s always best to stick to the deadline.

If you realize there’s an issue after you file your taxes, you must request an amendment. Your tax lawyer or accountant can help you prepare this and make the request.

You might be required to pay estimated quarterly taxes if you’re a freelancer. Speak to your accountant in advance if this is required. They’ll also advise you on how much to save to pay in estimated taxes.

Ensure you always keep a receipt of every tax payment you make on the IRS website.

As mentioned throughout this guide, you always want an expert to help you prepare your taxes. Find the best tax attorneys to help you with the process.

File Your Taxes Properly

Now you know what the IRS rounding rules are and how to use them to calculate your taxes.

Make sure you also follow our other tips on how to file your taxes without issue. Always keep track of your finances in a spreadsheet.

You must also always keep copies of your receipts and tax documents. Follow our best practices to avoid issues with filing taxes.

A great tax attorney will help you during the tax filing process.

Ready to tackle those taxes? Be sure to check out our other financial tips as well!