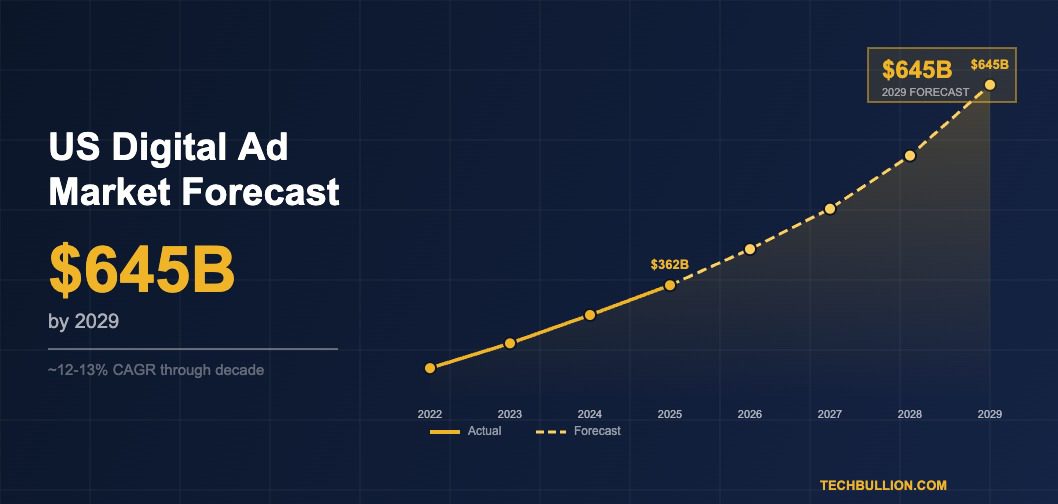

The meeting that signals a structural shift in how large an industry has become is rarely announced as such. For American digital advertising, that meeting happened quietly in media agency planning sessions throughout late 2024, when senior strategists began inputting a number into their long-range financial models that would have seemed implausible five years earlier: $645 billion. That is the scale that the most credible independent forecasting institutions now project for US digital advertising spend by 2029, a figure that sits at the outer edge of what most public commentary about the industry has yet fully absorbed.

The distance from $361.9 billion in 2025 to $645 billion in 2029 represents an additional $283 billion of annual digital advertising expenditure materialising over four years. That increment is larger than the entire US digital advertising market was in 2014. It is being driven not by optimistic extrapolation of past trends but by identifiable structural forces that are already in motion: the continued transfer of television budgets from linear to connected formats, the deepening penetration of retail media into trade marketing budgets, the expansion of AI-driven campaign tools that extend digital advertising accessibility to businesses that previously could not participate efficiently, and the ongoing globalisation of US platform revenue from markets where digital advertising adoption is still at an early stage.

Understanding what drives a market to $645 billion is as important as knowing the number itself.

The Linear Television Transfer Has More Distance to Run

The single largest reservoir of advertising budget that has not yet fully converted to digital formats remains linear television. In the United States, national broadcast and cable television commanded approximately $55 billion in advertising revenue as recently as 2023, according to Magna Global’s advertising forecast. The audience for that inventory has been declining for a decade as viewers migrated to streaming platforms, but advertising budgets follow audience more slowly than audience follows content, due to the structural inertia of upfront buying cycles and the preference of some brand categories for the guaranteed reach metrics that linear television provides.

The gap between where television audiences actually are and where television advertising budgets remain is one of the most reliable sources of incremental digital advertising spend available over the remainder of the decade. Every billion dollars that shifts from national broadcast and cable into connected television programmatic inventory flows through the AdTech stack that serves digital advertising. At current migration rates, US linear television advertising revenue is projected to fall below $40 billion by 2028, with the bulk of that decline redirected toward CTV and streaming platforms. That migration alone represents $15 to $20 billion of additional digital advertising demand that is not dependent on new advertiser entry or increased marketing budgets.

| Year | US Digital Ad Spend | YoY Growth | Primary Growth Driver |

|---|---|---|---|

| 2025 | $361.9 billion | +13% | CTV breakout; Amazon $50B+ |

| 2026 | ~$413 billion | +14% | Linear TV migration; retail media |

| 2027 | ~$470 billion | +14% | AI automation; SMB expansion |

| 2028 | ~$545 billion | +16% | New ad surfaces; spatial computing |

| 2029 | ~$645 billion | +18% | AI-native formats; platform globalisation |

Retail Media Will Keep Expanding Its Share of Digital Budgets

The retail media category that did not meaningfully exist as a distinct digital advertising segment in 2020 had grown to over $60 billion in annual US spend by 2025. Its trajectory toward 2029 is driven by dynamics that are structural rather than cyclical: the more transaction data a retailer accumulates, the more precisely they can demonstrate advertising ROI, and the more brands are willing to allocate budget to their networks. This self-reinforcing dynamic is not approaching saturation in the near term.

The expansion of retail media beyond Amazon into the Walmart Connect, Kroger Precision Marketing, Target Roundel, and Instacart Ads ecosystems has created a competitive market for retailer inventory that is driving both innovation and budget allocation. Brands that shifted initial retail media budgets toward Amazon experimentation in 2021 and 2022 are now establishing dedicated retail media strategies that span multiple networks, often with dedicated budget lines that did not exist in prior years. As TechBullion’s analysis of the US digital advertising forecast for 2026 establishes, retail media is already a confirmed structural pillar of the US digital advertising market rather than an emerging category requiring proof of concept.

The convergence of retail media with connected television, as retailers make their audience data available for targeting on streaming platforms, creates a further incremental growth vector that extends retail media’s reach well beyond sponsored product placements within e-commerce environments.

AI Automation Is Expanding the Effective Advertiser Base

One of the underappreciated components of the $645 billion forecast is the role of AI-powered campaign automation tools in expanding the total number of businesses that participate meaningfully in digital advertising. Meta’s Advantage+, Google’s Performance Max, and Amazon’s automated campaign management tools have each materially reduced the complexity barrier to entry for digital advertising, bringing smaller businesses into the market at scale that would not have been economically viable under manually managed campaign structures.

The effect on total market size is additive rather than redistributive. When a local business that previously ran minimal or no digital advertising begins spending $2,000 per month through an AI-automated Meta campaign, that budget is incremental to the market rather than shifted from an existing advertiser. Across millions of small and medium-sized businesses, this democratisation of digital advertising access represents a meaningful source of market expansion that does not depend on the behaviour of large advertisers.

As explored in TechBullion’s overview of the AdTech investment outlook, the investment flowing into AI-powered advertising infrastructure reflects a consensus view that these tools have not yet approached the limits of their market-expanding potential. The combination of lower entry costs, better performance attribution, and increasingly sophisticated creative automation will continue to bring new advertiser demand into the digital ecosystem through 2029.

| Growth Driver | Incremental Spend by 2029 | Primary Beneficiary Channels | Confidence Level |

|---|---|---|---|

| Linear TV budget migration | $15-20 billion | CTV, streaming platforms | High |

| Retail media expansion | $40-50 billion | Amazon, non-Amazon RMNs | High |

| AI-enabled SMB access | $25-35 billion | Social, search platforms | Medium-High |

| New ad surfaces (AR, AI) | $20-30 billion | Emerging platform formats | Medium |

| Platform revenue globalisation | $10-15 billion (US platforms) | Google, Meta international | Medium |

The Risks Embedded in the $645 Billion Forecast

No forecast of this magnitude is without risks, and the $645 billion projection carries several that deserve candid acknowledgement. The most significant is regulatory: the Department of Justice antitrust proceedings against Google’s search advertising dominance, if they result in structural remedies requiring Google to divest or operationally separate key advertising technology components, could disrupt the efficiency of the largest digital advertising channel and create transitional friction that slows budget growth. The Federal Trade Commission’s ongoing scrutiny of Meta’s data practices represents a parallel vector of potential market disruption.

Macroeconomic conditions represent a second risk category. Digital advertising has historically proven more resilient during economic downturns than traditional media, due to its measurability and the ability to pause campaigns quickly, but a severe or prolonged recession would inevitably slow the pace of incremental budget growth. The 2022 period, when digital advertising growth decelerated sharply in response to macroeconomic uncertainty, provides a relevant precedent.

The emergence of genuinely disruptive new platforms or technologies that redirect advertiser attention toward inventory surfaces not yet captured in current forecasting models represents a third category of forecast uncertainty, though this is a risk that cuts both ways: unexpected platform emergence could accelerate total market growth as well as redistribute it.

What $645 Billion Means for AdTech Infrastructure

The AdTech ecosystem that serves the US digital advertising market at $645 billion in 2029 will look considerably different from the one serving it at $361 billion in 2025. The additional $283 billion of annual spend will require proportional expansion of programmatic buying infrastructure, measurement systems, identity resolution capabilities, and creative technology. The companies that build and operate this infrastructure stand to benefit from the growth in underlying market volume regardless of which specific channels or platforms capture the largest share of total spend.

As detailed in TechBullion’s analysis of how the US digital ad market reached $361 billion in 2025, the technology stack enabling digital advertising at scale has been under sustained investment for a decade, and the returns from that investment are now compounding into the growth trajectory that the $645 billion forecast reflects. The next four years represent the continuation of that compounding rather than a break from it.

For practitioners, investors, and strategists operating in the US digital advertising market, the $645 billion number is not a distant aspiration. It is the destination that current structural trends are pointing toward, and the companies that understand what is driving it are better positioned to build for it.

Related reading: US Digital Advertising CAGR 2020-2025 | US Digital Ad Forecast 2026 | AdTech Investment Outlook | US Digital Ad Market 2025

According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020.

Market analysis from Grand View Research projects that technology-driven market segments will continue expanding at compound annual growth rates between 15 and 25 percent through the end of the decade.