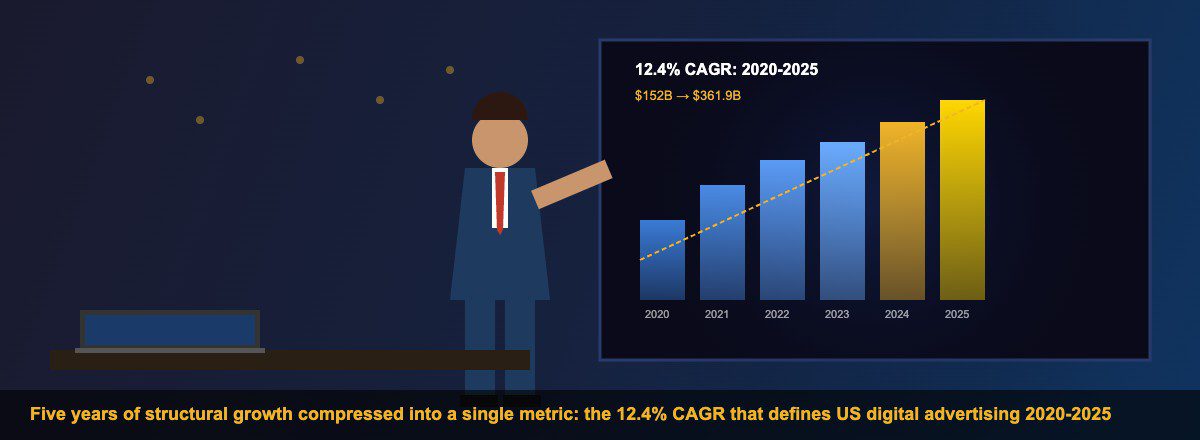

There is a number that quietly tells the whole story of how American digital advertising transformed between the pandemic year and the middle of the decade: 12.4. That is the compound annual growth rate at which US digital advertising spend expanded from 2020 to 2025, compressing what might otherwise have been a decade’s worth of structural change into five years of relentless expansion.

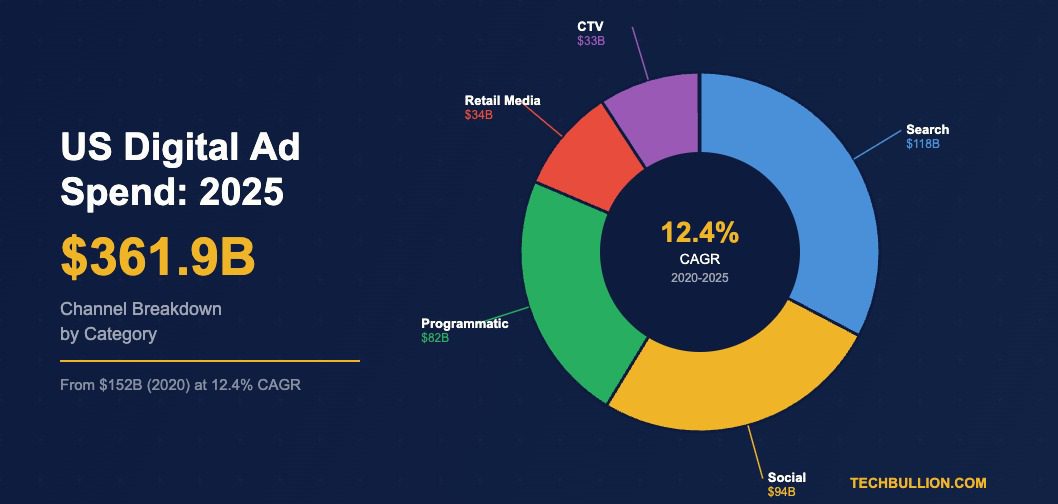

In 2020, total US digital advertising spend stood at approximately $152 billion, already the largest digital advertising market in the world by a wide margin. By 2025, that figure had reached $361.9 billion, more than doubling in absolute terms over a period that included a global pandemic, two years of macroeconomic turbulence, the most significant regulatory challenge to big tech since the Microsoft antitrust proceedings of the 1990s, and the disruption of the third-party cookie infrastructure that the entire programmatic ecosystem had been built upon. The 12.4 per cent CAGR was not achieved despite these headwinds. In several meaningful ways, it was accelerated by them.

Understanding the mechanics of that growth rate, and the forces that sustained it through conditions that would have stalled a less structurally resilient market, is essential context for anyone seeking to understand where US digital advertising is heading next.

The Pandemic Inflection Created a Base That Made Every Subsequent Year Look Slower

The 2020 to 2021 transition deserves particular attention because it shaped the statistical framing for the entire five-year period. US digital advertising grew by approximately 38 per cent in 2021, recovering from a modest contraction in 2020 caused by pandemic-driven advertiser caution and then surging as e-commerce adoption, streaming consumption, and digital media engagement all hit record levels simultaneously. That single year of 38 per cent growth contributed disproportionately to the five-year CAGR, making the subsequent years of 12 to 15 per cent growth appear comparatively moderate even as they added tens of billions of dollars of absolute revenue.

The channel-level story of those five years reflects the structural shifts that drove aggregate growth. Search advertising, the dominant category throughout, grew at approximately 9 per cent CAGR over the period as Google’s core search business expanded through mobile and AI-enhanced results, while Amazon’s emergence as the second major search advertising platform added incremental growth that was absent from 2020 baselines. Social media advertising grew faster at approximately 14 per cent CAGR, powered by Instagram’s commerce integration, the emergence of TikTok as a major advertising platform, and Meta’s recovery from its 2022 difficulties. Connected television, growing from a small base, delivered the highest CAGR of any major category at approximately 40 per cent as streaming audiences migrated away from linear television.

| Year | US Digital Ad Spend | YoY Growth | Key Channel Driver |

|---|---|---|---|

| 2020 | ~$152 billion | +5% (pandemic year) | Search resilience; social recovery |

| 2021 | ~$210 billion | +38% (rebound surge) | E-commerce boom; social + search |

| 2022 | ~$245 billion | +17% (normalisation) | Search + retail media growth |

| 2023 | ~$280 billion | +14% | Programmatic + retail media |

| 2024 | ~$320 billion | +14% | CTV acceleration; political spend |

| 2025 | $361.9 billion | +13% | CTV breakout; Amazon $50B+ |

Retail Media’s Emergence Explains Why Growth Stayed High at Scale

One of the most common questions about the US digital advertising CAGR is how a market at $152 billion can sustain double-digit percentage growth to reach $361 billion without running into the diminishing returns that typically afflict large markets. The answer lies substantially in the emergence of retail media as an entirely new advertising category that added incremental budget pools rather than competing for existing digital spend.

In 2020, retail media as a distinct advertising category barely existed in its modern form. Amazon’s advertising business was present but nascent, and the concept of retailers operating programmatic advertising networks using first-party transaction data was largely theoretical. By 2025, as detailed in TechBullion’s analysis of retail media technology, US retail media advertising across all networks had crossed $60 billion annually. This category created entirely new advertiser demand, drawing from trade marketing budgets that had never previously been categorised as digital advertising spend.

The practical effect was to extend the addressable market for digital advertising well beyond its 2020 boundaries. Brands that had historically separated their trade spending from their digital media budgets found that retail media networks collapsed that distinction, making previously non-digital expenditure flow through programmatic platforms and count toward digital advertising totals.

AdTech Infrastructure Investment Compounded the Growth

The CAGR story is inseparable from the sustained investment in AdTech infrastructure that made the growth technically possible. At $152 billion in 2020, the US digital advertising market was already the most sophisticated in the world, yet the programmatic infrastructure serving it was in many respects immature: cookie-based audience targeting was still dominant, measurement was fragmented across incompatible attribution models, connected television had no established programmatic buying pathway, and retail media inventory was not yet systematically accessible through demand-side platforms.

The five years from 2020 to 2025 saw billions invested in solving each of these limitations. Identity resolution platforms built alternatives to third-party cookie targeting. Measurement companies developed cross-channel attribution methodologies capable of spanning display, social, CTV, and retail media. The Trade Desk, Magnite, and their peers built programmatic infrastructure for streaming television. Retail SSPs created pathways for programmatic buyers to access retailer inventory. As explored in TechBullion’s overview of the AdTech investment outlook, each of these infrastructure investments increased the efficiency and reach of the advertising dollar, making it rational for advertisers to allocate incrementally larger budgets to digital channels.

| Infrastructure Built (2020-2025) | Problem Solved | Revenue Unlocked |

|---|---|---|

| Privacy-safe identity resolution | Cookie deprecation adaptation | Sustained open web CPMs |

| CTV programmatic buying | Streaming inventory access | $33B CTV market by 2025 |

| Retail media SSPs | Retailer inventory programmatic access | $60B+ retail media category |

| Cross-channel attribution | Multi-platform measurement | Justified larger budgets |

| AI campaign automation | SMB advertiser accessibility | Expanded advertiser base |

What the 12.4% CAGR Implies for the Next Five Years

If the period from 2020 to 2025 was defined by the maturation of existing digital channels and the emergence of retail media and CTV as new categories, the period from 2025 to 2030 will be shaped by the next layer of structural change. The forecast trajectory points to US digital advertising reaching approximately $645 billion by 2029, implying a forward CAGR of approximately 12 to 13 per cent, remarkably close to the rate achieved over the prior five years.

The sustainability of that rate at a larger absolute base depends on the emergence of new advertising surfaces and budget pools that can continue to expand the addressable market. The most likely candidates are artificial intelligence-native advertising formats, spatial computing and augmented reality environments, and the continued global expansion of US platform revenue from international markets not yet captured in US-only totals.

For AdTech investors and practitioners, the 12.4 per cent CAGR from 2020 to 2025 is not merely historical data. It is evidence that digital advertising can sustain extraordinary growth rates through structural change, regulatory pressure, and macroeconomic cycles, provided the underlying technology infrastructure continues to evolve. The full trajectory of the US market, including the $413 billion 2026 forecast analysed in TechBullion’s US digital advertising forecast, suggests that the next chapter is likely to look more similar to the last five years than most observers currently expect.

Related reading: US Digital Ad Market 2025 | US Digital Ad Forecast 2026 | AdTech Investment Outlook | Retail Media Technology

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.