The venture capital partners who gathered at a closed-door session in San Francisco in early 2024 were not debating whether advertising technology would continue to grow. They were debating which parts of it would grow fastest, and which incumbent players would find themselves displaced before the decade was out. The distinction matters. After a bruising 2022 and a cautious 2023, AdTech investment has returned with purpose, backed by a market forecast that points to continued structural expansion driven by forces that no macroeconomic cycle can easily reverse.

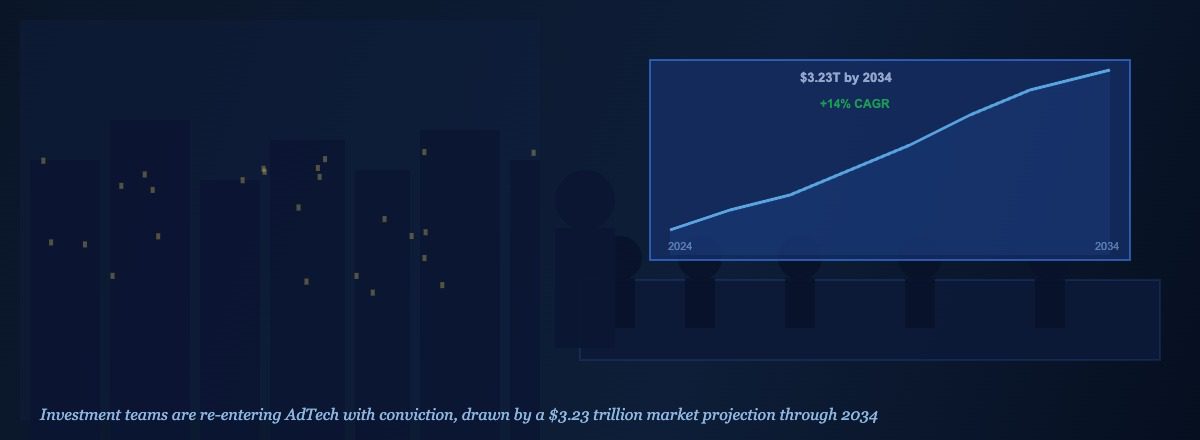

The numbers that underpin this confidence are substantial. The global AdTech market, valued at approximately $869 billion in 2024 according to Grand View Research, is projected to reach $3.23 trillion by 2034, a compound annual growth rate of approximately 14 per cent. That trajectory reflects not a single driving force but a convergence of several durable structural tailwinds: the migration of advertising budgets from traditional to digital media, the growth of connected television as a premium programmatic channel, the rise of retail media networks as a high-margin inventory category, and the continued expansion of digital advertising into emerging markets across Asia-Pacific, Latin America, and Africa.

Understanding why investment in advertising technology continues to flow, and where it is being directed, is essential context for anyone navigating the AdTech ecosystem.

The Migration of Television Budgets Is Still Only Partially Complete

The single largest reservoir of advertising spend that has not yet fully transitioned to programmatic digital channels is linear television. In the United States alone, television advertising commanded approximately $60 billion in annual spend as recently as 2022, according to Magna Global’s advertising forecast. The shift of viewers from linear broadcast and cable to streaming services has been well-documented, but the migration of advertising budgets has lagged behind audience migration by several years due to the structural differences between upfront television buying and programmatic digital purchasing.

Connected television is the primary channel absorbing these shifting budgets. CTV advertising revenue in the United States reached approximately $25 billion in 2024, according to eMarketer’s projections, and is forecast to exceed $40 billion by 2027. The gap between audience reach on streaming platforms and the advertising revenue those platforms command relative to linear television represents one of the largest near-term growth opportunities in the entire AdTech ecosystem. Every percentage point of linear television budget that migrates to programmatic CTV represents billions of dollars of incremental demand flowing through the technology stack.

| AdTech Segment | 2024 Market Size (est.) | 2027 Projection | Key Investment Driver |

|---|---|---|---|

| Connected Television (CTV) | $25 billion (US) | $40+ billion (US) | Linear TV budget migration |

| Retail Media Networks | $54 billion (global) | $100+ billion (global) | Commerce data + closed-loop attribution |

| Programmatic Display | $200+ billion (global) | $280 billion (global) | Open web + DOOH expansion |

| Audio Advertising | ~$13 billion (global) | ~$20 billion (global) | Podcast growth + programmatic DAI |

| Digital Out-of-Home | ~$22 billion (global) | ~$33 billion (global) | Screen digitalisation + programmatic |

Investment in CTV infrastructure has consequently been one of the dominant themes in AdTech funding since 2022. The Trade Desk, which built significant CTV buying capabilities into its platform, grew its annual revenue to approximately $2.4 billion in 2024. Magnite, FreeWheel, and Publica have attracted sustained investment as the sell-side technology layer enabling programmatic access to streaming inventory.

Retail Media Has Become the Category That Every Major Investor Is Watching

If CTV represents the largest near-term budget migration opportunity, retail media represents the most structurally novel growth category. As detailed in TechBullion’s analysis of retail media technology, the emergence of retailer-owned advertising networks has created a new tier of inventory that commands premium CPMs precisely because it sits closest to the moment of purchase decision.

Amazon’s advertising business, which crossed $50 billion in annual revenue in 2024, demonstrated to the market that retail transaction data is the most valuable targeting and measurement asset in digital advertising. The replication of this model by Walmart Connect, Kroger Precision Marketing, Target’s Roundel, and dozens of regional retailers has created what the industry now calls a retail media network ecosystem, and investment in the technology infrastructure required to build, operate, and connect these networks has followed accordingly.

Criteo, which repositioned itself as a retail media technology platform, and companies including Epsilon, CitrusAd, and Symbiosys have attracted significant capital on the thesis that every retailer with meaningful transaction data will eventually want the infrastructure to monetise it. The scale of this investment reflects a consensus view that retail media is a structural addition to the AdTech landscape rather than a temporary trend, a view supported by GroupM’s projection that retail media will account for approximately 20 per cent of global digital advertising by 2027.

Privacy Technology Investment Is Being Driven by Regulatory Necessity, Not Optional Enhancement

A third major driver of AdTech investment that will not diminish regardless of macroeconomic conditions is privacy infrastructure. The regulatory framework surrounding digital advertising data has expanded substantially since GDPR entered force in 2018, and the trajectory of global privacy regulation points consistently toward stricter data collection rules, enhanced consent requirements, and heightened enforcement. As examined in TechBullion’s coverage of privacy-preserving advertising technology, compliance with this regulatory environment requires investment in technical infrastructure that the industry has historically been reluctant to fund voluntarily.

The deprecation of third-party cookies in Chrome accelerated investment in identity resolution alternatives including first-party data clean rooms, universal ID systems such as LiveRamp’s Authenticated Traffic Solution and The Trade Desk’s Unified ID 2.0, and privacy-preserving measurement methodologies. Each of these technology categories has attracted venture capital and strategic investment, creating a new tier of AdTech infrastructure that did not exist five years ago.

| Investment Category | Investment Driver | Key Players Attracting Capital | Investment Horizon |

|---|---|---|---|

| Privacy-safe identity | Cookie deprecation | LiveRamp, ID5, Unified ID 2.0 | 2024-2027 |

| Data clean rooms | GDPR + walled garden data access | Habu, InfoSum, Snowflake | 2024-2028 |

| AI-powered optimisation | Efficiency + targeting accuracy | Multiple DSPs, creative AI vendors | 2024-2030 |

| Measurement infrastructure | Attribution accuracy post-cookie | Nielsen, iSpot, Innovid, VideoAmp | 2024-2028 |

| Retail media enablement | Commerce data monetisation | Criteo, CitrusAd, Epsilon | 2024-2029 |

Artificial Intelligence Is Compressing Technology Cycles and Attracting Generalist Capital

The integration of artificial intelligence into advertising technology has become one of the defining investment themes of the mid-2020s. Where AI in AdTech was historically associated with incremental improvements to bidding algorithms and audience prediction models, the generative AI capabilities that emerged from 2023 onwards have created new categories of tooling: automated creative generation, real-time copy personalisation, AI-driven media planning, and conversational campaign management interfaces.

These capabilities have attracted a category of investor that has not traditionally been active in AdTech: generalist technology venture funds drawn by the AI narrative rather than deep domain knowledge of programmatic buying. The result has been a significant increase in total investment flowing into the AdTech category, though with a concentration in AI-adjacent tooling rather than core programmatic infrastructure. The broader market structure within which these investments are being made is analysed in TechBullion’s overview of AdTech market concentration.

The risk embedded in this investment wave is the degree to which AI capabilities will be commoditised within the major platform ecosystems. Google, Meta, and Amazon have each embedded AI-powered campaign optimisation tools directly into their self-serve advertising interfaces. Independent AdTech vendors that are building AI tools that replicate capabilities already available for free within platform walled gardens face a structural challenge that even sophisticated venture capital cannot easily underwrite away.

Emerging Markets Represent the Next Phase of Structural Growth

The final investment thesis that points to sustained AdTech spending growth is geographic. The digital advertising markets that have driven growth in the United States and Western Europe over the past two decades are maturing, with penetration rates for digital advertising reaching 75 to 80 per cent of total advertising spend in the most advanced markets. The next phase of growth will be driven by markets where digital advertising penetration remains well below 50 per cent: India, Southeast Asia, Latin America, and Sub-Saharan Africa.

India’s digital advertising market crossed $10 billion in 2024, according to the Dentsu Digital Advertising Report, and is growing at over 20 per cent annually driven by smartphone adoption, affordable mobile data, and the growth of e-commerce. Indonesia, Brazil, and Nigeria are each on trajectories that mirror the early growth phases of the US and UK digital advertising markets a decade earlier. Investment in localised AdTech infrastructure is following the audience growth, creating opportunities for regional technology vendors and for global players seeking to establish early positions in high-growth geographies.

The investment case for AdTech is not a uniform one. Within a market projected to reach $3.23 trillion by 2034, there are categories with exceptional growth momentum and categories facing structural disruption from platform consolidation and regulatory pressure. As explored across TechBullion’s ongoing coverage of the AdTech market, the sophistication required to navigate these distinctions is precisely why investment in AdTech knowledge and capability continues to grow alongside investment in AdTech technology itself.

Related reading: Retail Media Technology | AdTech Market Concentration | Privacy-Preserving Advertising | DOOH Advertising Technology

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.