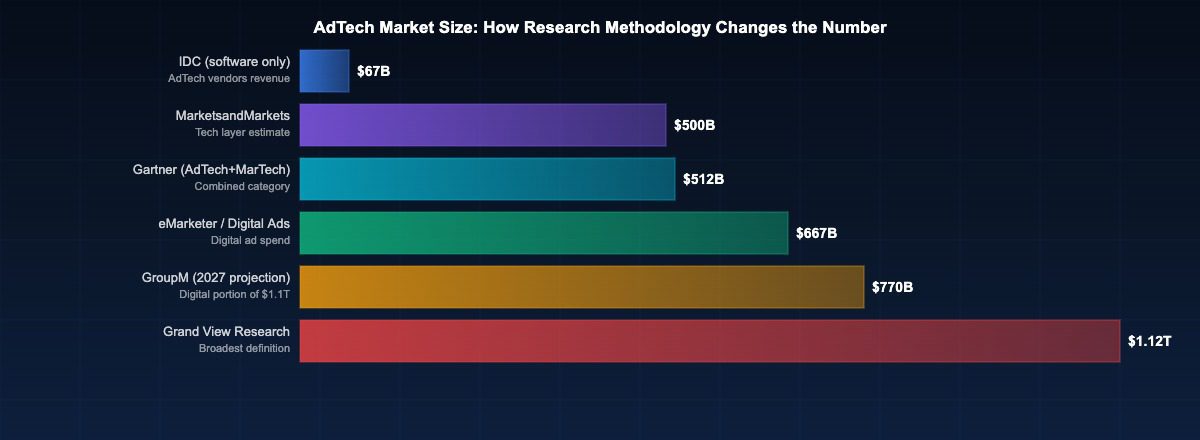

Ask five research firms to size the global AdTech market and you will receive five different answers. Not estimates that are roughly comparable, but figures that diverge by a factor of fifteen, ranging from approximately $67 billion to $1.12 trillion, depending on which firm you ask and what they chose to count. This is not a failure of research methodology so much as evidence that “AdTech market” describes different things to different analysts, and that understanding which definition underpins any given number is the prerequisite for using it intelligently.

The combined scale of the two technology categories makes the distinction consequential. Global MarTech spending is projected to exceed $700 billion by 2026, according to Statista, while AdTech estimates range from below $100 billion at the narrowest to over $1 trillion at the broadest. For investors, practitioners, and journalists attempting to communicate market scale with accuracy, navigating these competing forecasts is an exercise in research methodology as much as market analysis.

Why Estimates Vary So Dramatically

The single most important driver of variation in AdTech market size estimates is the question of what is included within the definition. Different research methodologies draw the boundary of “AdTech” in fundamentally different places, and those boundary decisions produce dramatically different totals.

The narrowest definitions focus exclusively on AdTech software and infrastructure revenue: the fees earned by demand-side platforms, supply-side platforms, ad servers, data management platforms, and associated technology vendors. Under this definition, market size is measured by the aggregate revenue of AdTech companies themselves, not by the total advertising spend that flows through their systems. Research from Gartner and Forrester applying this framing typically produces estimates in the $50 billion to $80 billion range for the global AdTech software market, reflecting the actual revenues of companies such as The Trade Desk, Magnite, PubMatic, DoubleVerify, and Integral Ad Science.

Broader definitions include total digital advertising spend that transacts through AdTech infrastructure, even though most of that spend flows to publishers and media owners rather than to the AdTech companies themselves. Under this framing, the AdTech market is roughly equivalent to the global digital advertising market, which GroupM estimated at $660 billion in 2024. This is the definition implicitly or explicitly used by most headline market size figures that appear in industry press releases, vendor websites, and general business coverage.

The widest definitions, which produce figures in the $1 trillion to $1.5 trillion range, extend the boundary further still to capture the full economic value enabled by AdTech infrastructure, including the advertising revenue of the large platform companies (Alphabet, Meta, Amazon) whose own technology stacks are categorised as AdTech even though their revenue model is that of a media company rather than a technology vendor.

The $1.12 Trillion Figure: Source and Methodology

The specific estimate of $1.12 trillion for the global AdTech market has been cited in reports from multiple market research publishers including Grand View Research, MarketsandMarkets, and Mordor Intelligence. These firms typically apply the broadest definitional frame, encompassing total advertising spending mediated by digital technology infrastructure across search, social, display, video, connected television, audio, and mobile advertising.

Grand View Research, in its 2024 Global Advertising Technology Market Report, projected the market at approximately $1.12 trillion by 2028 using a compound annual growth rate of approximately 14 per cent applied to a 2023 base figure. The methodology includes programmatic advertising spend, direct digital advertising transactions on platform environments, and the full revenue of platform-native advertising systems operated by Alphabet, Meta, and Amazon. Excluding those three platform companies would reduce the estimate substantially.

MarketsandMarkets, using a somewhat narrower frame that focuses on the technology revenue layer rather than total media spend, published estimates for the AdTech market in the $400 billion to $600 billion range for a similar forecast period, illustrating precisely how definitional choices reshape the output.

Mordor Intelligence’s 2024 report on the digital advertising market, which is often cited interchangeably with AdTech market figures, projects total digital advertising spend to reach approximately $1.1 trillion by 2028, again driven primarily by growth in mobile advertising, connected television, and continued expansion of retail media networks.

Competing Frameworks from Major Research Houses

The research firms that large enterprises and investment banks rely upon for market sizing tend to apply more conservative and methodologically transparent definitions than the syndicated market research publishers whose headline figures dominate trade press coverage.

IDC segments the advertising technology market into distinct layers: advertising software platforms, advertising services, and media spend. IDC’s estimates for the AdTech software layer specifically, which represents the actual revenue of AdTech vendors, were approximately $67 billion globally in 2023 according to their Worldwide Advertising Technology Spending Guide.

Gartner’s analysis of the AdTech market focuses on enterprise marketing technology spending, which it estimates at approximately $512 billion globally for 2024 when combining both AdTech and MarTech categories. Gartner’s CMO Spend Survey, published annually, provides insight into how marketing budgets are actually allocated rather than projecting total market size, and consistently finds that paid media (which funds AdTech) represents the largest single category of marketing expenditure at approximately 25 per cent of total marketing budgets.

GroupM, the world’s largest media investment group and a subsidiary of WPP, publishes the most widely cited forecast for total global advertising spend, which it projects at $1.1 trillion by 2027 across all channels including television, print, out-of-home, radio, and digital. Digital advertising, which is the channel category most directly associated with AdTech infrastructure, represents approximately 70 per cent of total global advertising by 2026 under GroupM’s projections, implying a digital advertising market of approximately $770 billion.

Regional Composition and Its Impact on Global Estimates

Market size estimates are also shaped by assumptions about regional composition, currency conversion methodologies, and the treatment of rapidly growing but lower-CPM markets in Asia-Pacific and Latin America.

The United States represents the single largest national AdTech market, with the Interactive Advertising Bureau (IAB) reporting total US digital advertising revenue of $225 billion in 2023. The US market is particularly important to global estimates because it combines high CPMs, high programmatic adoption rates, and a dense ecosystem of independent AdTech vendors, making it the market where the distinction between AdTech software revenue and media spend is most clearly documented.

China’s digital advertising market presents a particular challenge for global estimates. Platforms including Alibaba, Tencent, Baidu, and ByteDance operate at massive scale, but their advertising ecosystems are largely closed to the Western AdTech infrastructure vendors whose revenues are most commonly measured. Chinese digital advertising revenue of approximately $130 billion in 2024, according to eMarketer, may or may not be included in global AdTech estimates depending on whether the analyst is measuring the global market for AdTech tools and platforms or the global market for advertising that transacts through any digital technology infrastructure.

Europe’s AdTech market is estimated at approximately $100 billion in annual digital advertising spend, according to the European Digital Advertising Alliance, with the UK, Germany, and France representing the three largest national markets. The impact of the General Data Protection Regulation and the broader regulatory environment in Europe has materially affected the structure of the AdTech market there, with restrictions on behavioural targeting reducing the premium attached to data-rich programmatic inventory relative to the US market.

Practical Implications for Using Market Size Data

For practitioners, investors, and researchers working with AdTech market estimates, several practical guidelines help navigate the competing figures.

First, always identify the source’s definitional boundary before citing a number. A figure from Grand View Research that includes total digital advertising spend flowing through platform ecosystems is not comparable to a figure from IDC that measures only the revenue of AdTech software vendors. Both may be accurate within their own definitions while being entirely incompatible with each other.

Second, understand the forecast year. A market size figure for 2028 is a projection, not a measurement, and the uncertainty range around projections five years forward in a rapidly changing technology sector is substantial. The Covid-19 pandemic demonstrated that even one-year digital advertising forecasts from the most reputable research houses can miss actual outcomes by 20 per cent or more in either direction.

Third, treat figures from vendors and industry associations with appropriate scepticism. A vendor that sells AdTech infrastructure has a commercial interest in the market being described as large and growing. IAB figures represent the self-reported revenues of IAB member companies and may not capture all market participants equally.

The $1.12 trillion figure is not wrong, but it describes a different thing than most practitioners are seeking to measure when they ask how large the AdTech market is. Understanding precisely what each estimate includes is the prerequisite for using any of them intelligently.

Related reading: AdTech Market Concentration | AdTech vs MarTech | Programmatic Advertising and RTB | Attribution Technology in AdTech

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.