The terms AdTech and MarTech are used interchangeably in boardrooms, vendor pitches, and industry conferences with a frequency that suggests they mean the same thing. They do not. AdTech and MarTech represent distinct technology categories serving different commercial functions, operating on different economic models, and drawing on different data architectures. Understanding the boundary between them, and the increasingly contested territory where they overlap, is foundational to anyone making technology investment decisions in modern marketing organisations.

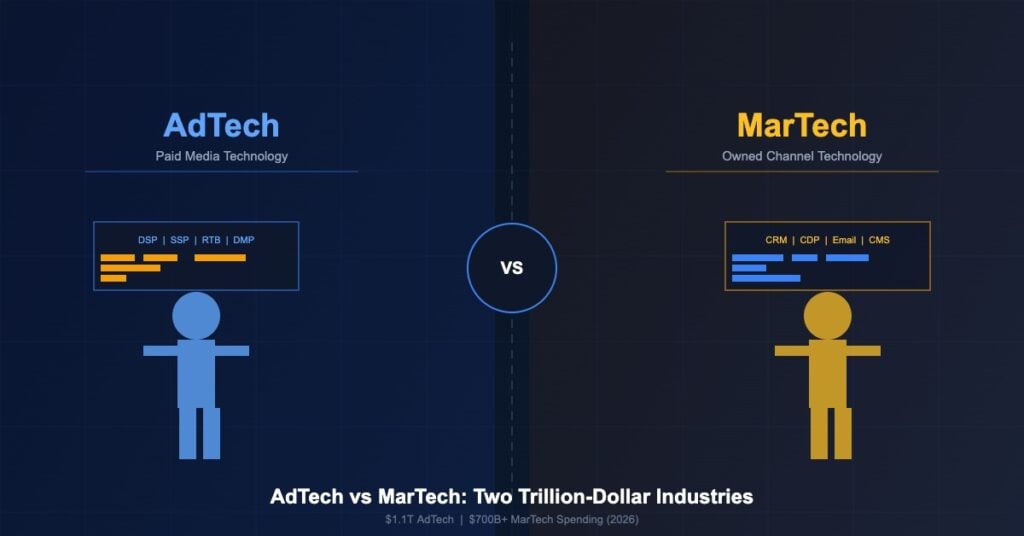

The combined scale of the two categories makes the distinction consequential. Global MarTech spending is projected to exceed $700 billion by 2026, according to Statista, while the global AdTech market is estimated at approximately $1.1 trillion when measured across the full value chain of programmatic infrastructure, platform revenue, and associated services. These are not niche software categories but the central technological infrastructure of the modern commercial economy.

Defining the Categories

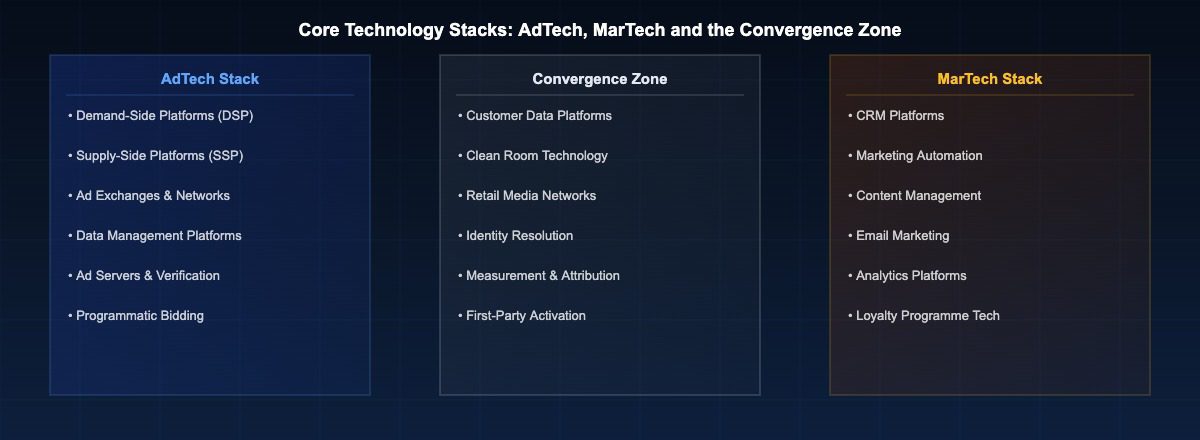

AdTech, or advertising technology, refers to the systems, platforms, and infrastructure used to plan, buy, deliver, target, and measure paid advertising across digital media. The core AdTech stack includes demand-side platforms (DSPs) through which advertisers purchase media inventory programmatically, supply-side platforms (SSPs) through which publishers sell inventory, ad exchanges where buyers and sellers transact, data management platforms (DMPs) that aggregate audience data for targeting, and ad servers that manage creative delivery and frequency capping. Companies including The Trade Desk, Google Ad Manager, Xandr (Microsoft), Magnite, and Index Exchange are central players in the independent AdTech ecosystem, alongside the walled garden platforms operated by Alphabet, Meta, and Amazon.

The defining commercial characteristic of AdTech is that it is built around paid media. Every interaction within the AdTech stack ultimately traces back to a financial transaction in which an advertiser pays to place a message in front of an audience it does not own. The AdTech stack exists to make that transaction more efficient, more targeted, and more measurable.

MarTech, or marketing technology, refers to the software tools used to plan, execute, automate, and measure marketing activities that a company conducts through channels it owns or operates directly. The MarTech stack encompasses customer relationship management (CRM) systems such as Salesforce, marketing automation platforms such as HubSpot and Marketo, content management systems, email marketing tools, social media management platforms, analytics platforms such as Google Analytics and Adobe Analytics, customer data platforms (CDPs), and loyalty programme infrastructure. Scott Brinker, who maintains the widely referenced MarTech Landscape, catalogued over 14,000 distinct MarTech solutions in his 2024 report, a figure that reflects both the category’s breadth and the degree of fragmentation within it.

The defining commercial characteristic of MarTech is that it operates across owned and earned channels. A company’s email list, its website, its customer database, and its social media presence are all owned assets. MarTech tools help organisations activate those assets more effectively without paying media costs for each impression or interaction.

The Economic Model Distinction

The economic boundary between AdTech and MarTech is perhaps the clearest way to understand the two categories. AdTech economics are fundamentally media economics. Every time an advertiser wins a programmatic auction and serves an impression, a portion of the advertiser’s spend flows through the AdTech stack to pay for the inventory, the data used to target it, the DSP fee, the SSP fee, the ad server fee, and the exchange take rate. Industry research from ISBA and PwC found that only 51p of every pound spent on programmatic advertising in the UK reaches the publisher as media cost, with the remainder absorbed by various AdTech intermediaries. The entire AdTech ecosystem is funded by media spend flowing from advertisers to publishers.

MarTech economics are software economics. A company pays a software vendor a subscription fee, a usage-based fee, or an implementation fee to licence the tools that help it manage its customer relationships, automate its marketing workflows, and analyse its owned data. There is no media transaction involved. Salesforce generates revenue by selling licences to its CRM platform, not by taking a cut of any advertising spend. HubSpot earns subscription revenue when marketers use its email automation tools to send messages to their own customer lists.

This distinction has significant implications for procurement, governance, and accountability. AdTech spend is typically managed by media buying teams and flows through agency relationships, with measurement focused on reach, frequency, CPM, and conversion metrics. MarTech spend is typically managed by marketing operations or IT teams and evaluated through software procurement processes, with measurement focused on efficiency gains, automation rates, and customer lifecycle metrics.

Where the Lines Blur

The clean conceptual boundary between AdTech and MarTech has been progressively eroded by several structural trends that are reshaping both categories.

Customer data platforms represent perhaps the clearest example of a technology that straddles the boundary. A CDP ingests first-party customer data from across an organisation’s owned touchpoints, resolves it into unified customer profiles, and then activates those profiles for targeting across both owned channels (email, push notifications, website personalisation) and paid channels (programmatic advertising, social retargeting). When a CDP feeds audiences into a demand-side platform for paid media activation, it is functioning as AdTech infrastructure built on MarTech data foundations. Vendors including Segment, Tealium, mParticle, and Adobe Real-Time CDP occupy this intersection explicitly.

The deprecation of third-party cookies, which Google has repeatedly delayed but which remains a structural direction of travel for the open web, is accelerating the convergence. As third-party audience targeting loses fidelity, advertisers are increasingly reliant on first-party data that lives within the MarTech stack. Publishers and brands are building direct data relationships through their owned channels, then activating those relationships in paid media through clean room technologies such as LiveRamp, Habu, and Google Ads Data Hub. This clean room model requires integration between the MarTech systems that hold first-party data and the AdTech systems through which paid media is purchased.

Retail media is another convergence zone. When a retailer such as Tesco, Walmart, or Boots allows consumer goods brands to advertise within its digital properties using its loyalty data, it is operating technology infrastructure that combines MarTech data assets (loyalty programme data, purchase history, customer profiles) with AdTech delivery mechanisms (on-site sponsored listings, programmatic off-site targeting). Tesco’s dunnhumby data science subsidiary, for example, has built an entire commercial operation on exactly this combination.

Organisational Consequences

The AdTech/MarTech distinction is not merely academic. It has concrete organisational consequences for how marketing functions are structured, how budgets are allocated, and how technology governance operates within companies.

In organisations where AdTech and MarTech are managed as separate domains, the risk of data silos is significant. Paid media teams may be purchasing audiences for acquisition campaigns without access to the first-party customer data held within the CRM or CDP, leading to situations where a brand is paying to target programmatic display ads at existing high-value customers. According to research by Forrester, organisations with integrated AdTech and MarTech data architectures demonstrate 23 per cent higher return on advertising spend than those operating the two stacks in isolation.

The rise of the chief marketing technology officer (CMTO) as a distinct organisational role reflects growing awareness that neither the traditional CMO nor the CTO adequately bridges the two domains. Companies including Unilever, Procter and Gamble, and L’Oreal have invested in dedicated marketing technology leadership that spans the AdTech and MarTech boundary.

Vendor consolidation is also reshaping the landscape. Adobe’s acquisition of Marketo, Salesforce’s development of its Advertising Studio product, and Oracle’s construction of its Marketing Cloud by combining BlueKai (a DMP) with Eloqua (a marketing automation platform) all reflect vendor strategies to capture spend on both sides of the boundary by offering integrated suites that eliminate the organisational seam between the two domains.

Implications for Technology Buyers

For practitioners making technology investment decisions, the AdTech and MarTech distinction provides a useful framework for evaluating vendor claims and aligning technology choices with business objectives.

Technology described as solving a paid media problem, whether in audience targeting, media buying, ad serving, or programmatic optimisation, falls within the AdTech category and should be evaluated on its ability to improve media efficiency and targeting precision within the context of a broader media strategy. The relevant benchmarks are CPM, viewability, brand safety, and return on ad spend.

Technology described as improving the management of owned customer relationships, automating marketing workflows, or analysing first-party data falls within the MarTech category and should be evaluated on its ability to improve customer lifetime value, conversion rates within owned channels, and marketing operational efficiency. The relevant benchmarks are email open rates, customer retention metrics, and cost per acquired customer through owned channels.

Technology that bridges the two categories, particularly CDPs and clean room solutions, requires evaluation frameworks that account for both dimensions. These tools derive their value precisely from the integration they enable between first-party data assets and paid media activation, and should be assessed on their ability to improve performance across both owned and paid channels simultaneously.

The distinction between AdTech and MarTech will continue to evolve as data regulation, platform dynamics, and technology architecture shift. But the underlying commercial logic that separates the two categories, paid media economics on one side and owned channel software on the other, remains the most reliable guide for practitioners navigating a vendor landscape that has every commercial incentive to obscure it.

Related reading: AdTech Market Concentration | Programmatic Advertising and RTB | Attribution Technology in AdTech | Privacy-Preserving Advertising

According to CoinGecko’s 2024 annual crypto report, total cryptocurrency market capitalisation exceeded $3.5 trillion by the end of 2024, reflecting renewed institutional interest following spot ETF approvals in the United States.

Data from Chainalysis’s 2024 Global Crypto Adoption Index shows that emerging markets in South and Southeast Asia continue to lead grassroots cryptocurrency adoption, driven by remittance use cases and limited access to traditional banking services.