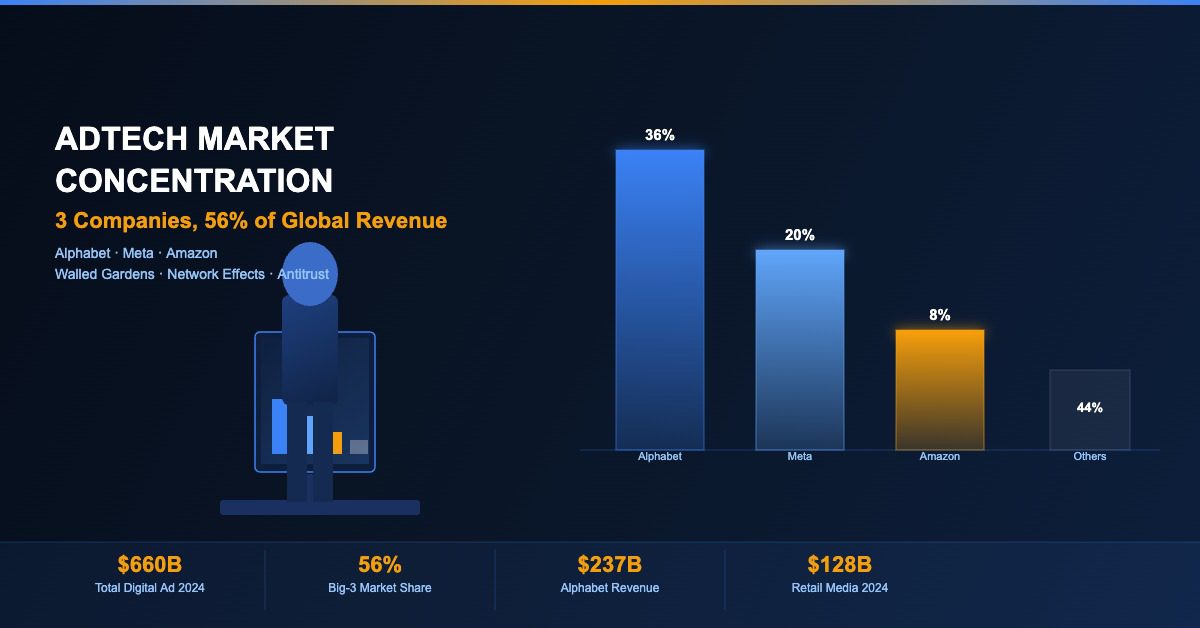

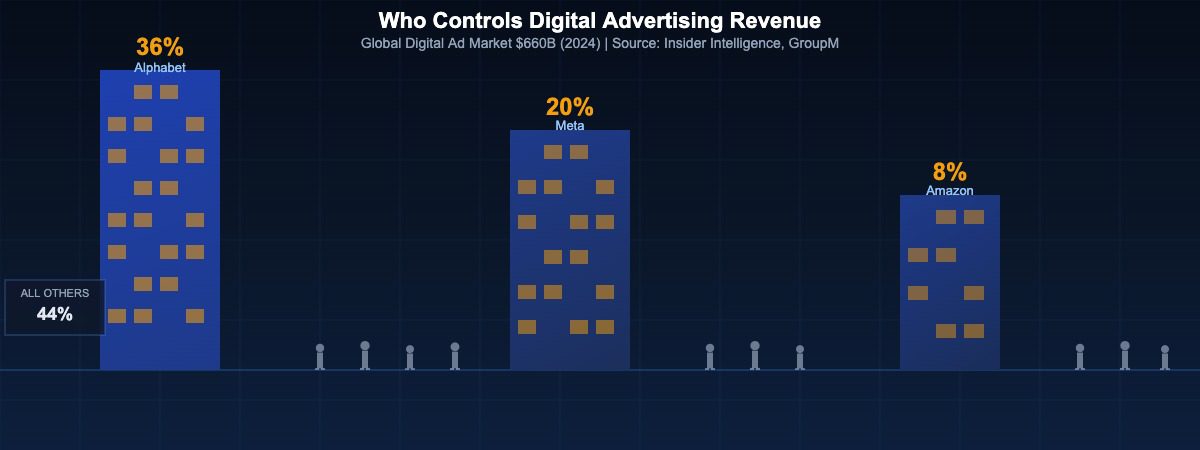

Digital advertising has produced one of the most concentrated market structures in the history of media. Three companies, Alphabet (Google’s parent), Meta, and Amazon, collectively captured approximately 56 per cent of global digital advertising revenue in 2024, according to analysis from Insider Intelligence and GroupM’s global advertising forecast. In absolute terms, this translates to roughly $370 billion of an estimated $660 billion total digital advertising market flowing to three technology companies headquartered within a 50-mile radius of each other in the United States.

This concentration is not accidental. It is the product of deliberate platform architecture, network effects, first-party data advantages, and vertical integration across the full advertising value chain. Understanding how this concentration emerged, what sustains it, and where regulatory and competitive pressure may reshape it is essential context for anyone operating within the wider AdTech ecosystem.

The Architecture of Dominance

Alphabet’s advertising revenue, which reached $237 billion in 2024 according to the company’s own financial disclosures, is generated across a vertically integrated stack that few rivals can replicate. Google Search captures intent at the moment of highest commercial value, delivering text ads to users actively seeking products and services. YouTube provides the world’s largest video advertising environment, reaching over 2.7 billion monthly logged-in users. Google Display Network, operating through DoubleClick’s successor infrastructure (now Google Ad Manager), connects advertisers to millions of publisher websites through programmatic channels. Google’s demand-side platform (DV360) and ad server (Campaign Manager 360) sit at the top of the buy-side stack, while Google Ad Manager dominates publisher ad serving.

The consequence is that an advertiser can run an entire campaign, from upper-funnel awareness through YouTube to lower-funnel conversion through Search, entirely within Google’s ecosystem, measured by Google’s attribution tools, optimised by Google’s machine learning, and reported through Google’s dashboards. Each additional dollar of spend deepens the signal advantage Google accrues, making its targeting and measurement capabilities progressively more accurate relative to smaller rivals.

Meta’s advertising business, generating approximately $135 billion in 2024 revenue, operates a different but equally formidable architecture. Facebook and Instagram together reach approximately 3.2 billion daily active users, providing reach that few other advertising environments can match. Meta’s social graph, accumulated over two decades, enables audience targeting based on social connections, expressed interests, and behavioural patterns that are simply unavailable in other environments. WhatsApp Business and Messenger are adding click-to-message advertising formats that extend Meta’s commercial surface area further.

Amazon’s advertising business, which crossed $50 billion in annual revenue in 2024, occupies a structurally unique position. Amazon Advertising’s core advantage is proximity to purchase. Sponsored Products, Sponsored Brands, and Sponsored Display placements appear directly within the commerce journey of shoppers with demonstrably high purchase intent. Amazon’s measurement proposition, grounded in actual transaction data from its retail operations rather than probabilistic attribution, provides a level of outcome verification that pure-play digital advertising platforms cannot match.

Why Concentration Has Proved Durable

Several structural factors have sustained this three-player concentration despite years of regulatory scrutiny and the presence of well-resourced competitors.

First, data network effects compound over time. Each additional user interaction on Google Search, YouTube, or Instagram generates signal that improves the targeting and measurement capabilities of the platform’s advertising products. A brand with 15 years of conversion data flowing into Google’s performance algorithms has built a positional advantage that cannot be easily replicated by switching to a competitor with a shorter data history.

Second, the walled garden model actively resists interoperability. Each of the three dominant platforms operates as a closed ecosystem in which advertiser data, audience data, and measurement data remain proprietary. Advertisers who invest in building campaign history, creative libraries, and audience segments within Google’s ecosystem face meaningful switching costs when considering moving budget to alternative environments. This friction benefits incumbents disproportionately.

Third, the full-funnel coverage offered by Google and Meta reduces the operational complexity of multi-platform planning for smaller advertisers. A small business with a limited marketing team can achieve measurable results by running Google Search and Meta campaigns without engaging the complexity of programmatic buying, publisher negotiations, or specialist ad technology vendors. This simplicity advantage reinforces the platform duopoly for the long tail of advertising spend, even as large sophisticated advertisers diversify their media mix.

The Challengers: Who Is Gaining Ground

While the three-company concentration remains dominant, several players are eroding the margin at the edges. TikTok’s advertising revenue reached an estimated $18 billion globally in 2024, growing faster than any other major platform. Its algorithm-driven content distribution model has attracted younger demographics and created a category of short-form video advertising that Google and Meta have had to respond to rather than lead.

Retail media represents the most significant structural challenge to the Google-Meta duopoly among large advertisers. Walmart Connect, Kroger Precision Marketing, Instacart Ads, and dozens of retailer-owned advertising networks have redirected meaningful budget from performance marketing channels by offering closed-loop attribution grounded in actual purchase data. The Trade Desk’s estimate that retail media will account for approximately 20 per cent of global digital advertising by 2027 suggests the disruption to existing platform share is ongoing.

Connected television is creating another front of competition. Streaming services including Netflix, Disney+, and Paramount+ have launched advertising-supported tiers that attract premium CPMs. CTV inventory sits largely outside Google and Meta’s direct control, creating demand for programmatic buying infrastructure through The Trade Desk, Magnite, FreeWheel, and other independent technology vendors.

Microsoft Advertising, benefiting from its Bing integration and LinkedIn’s B2B targeting capabilities, has maintained a stable if modest share of search and professional advertising budgets. Microsoft’s integration of OpenAI’s technology into Bing and its advertising platform has created new attention and some incremental share gain in search, though Google’s search dominance has proved resilient even against this technological challenge.

Regulatory Pressure and Its Limits

The concentration in digital advertising has attracted sustained regulatory attention across multiple jurisdictions. The US Department of Justice’s antitrust case against Google, which went to trial in 2024, focused specifically on Google’s dominance in search advertising and the self-reinforcing nature of its distribution agreements with browser makers and device manufacturers. The court’s findings and any remedies will have significant implications for the competitive landscape.

The European Union’s Digital Markets Act, which entered full enforcement in 2024, designates Alphabet, Meta, and Amazon as “gatekeepers” subject to interoperability, data access, and fair trading obligations. The DMA’s requirement that gatekeepers allow third-party ad tech vendors access to their platforms’ data and functionality on equivalent terms to their own services is specifically targeted at the vertical integration advantage that sustains platform dominance.

The UK’s Competition and Markets Authority has been perhaps the most active regulator in the digital advertising space, publishing comprehensive market studies in 2020 and 2023 that detailed the mechanisms of platform dominance and proposing structural remedies including separation of buy-side and sell-side tools, interoperability requirements, and enhanced data portability obligations.

Whether regulatory intervention can meaningfully reshape a market structure built on network effects and data advantages accumulated over two decades remains an open question. Historical precedent from telecommunications and other network industries suggests that regulation can constrain the most extreme competitive abuses without fundamentally altering the underlying concentration dynamics. Nonetheless, the scale and sophistication of current regulatory activity represents the most serious structural challenge the dominant platforms have faced.

Implications for the Wider AdTech Ecosystem

For independent AdTech vendors, the concentration dynamic creates both constraint and opportunity. The constraint is direct: every dollar that flows into Google’s or Meta’s walled gardens is a dollar that does not flow through the open programmatic ecosystem that independent DSPs, SSPs, data vendors, and measurement companies depend on. The Trade Desk’s revenue growth, which reached approximately $2.4 billion in 2024, reflects the resilience of demand for independent buying infrastructure, but the total available market for independent AdTech is definitionally bounded by what the dominant platforms leave outside their walls.

The opportunity lies in the spaces the dominant platforms cannot or choose not to serve well: CTV inventory, retail media enablement, privacy-compliant measurement, omnichannel identity resolution, and the growing mid-market segment of advertisers who find platform-native tools inadequate for their sophistication needs. Independent AdTech companies that build genuine capability in these spaces, rather than competing directly with platform products, are finding sustainable commercial positioning even within a highly concentrated market.

The concentration in digital advertising is a structural feature of the market rather than a temporary condition. Understanding its origins, its mechanisms, and the competitive and regulatory forces that are slowly reshaping it is foundational to any serious engagement with the AdTech industry’s future trajectory.

Related reading: Programmatic Advertising and RTB | DSP Market Analysis | Attribution Technology in AdTech | Privacy-Preserving Advertising

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.