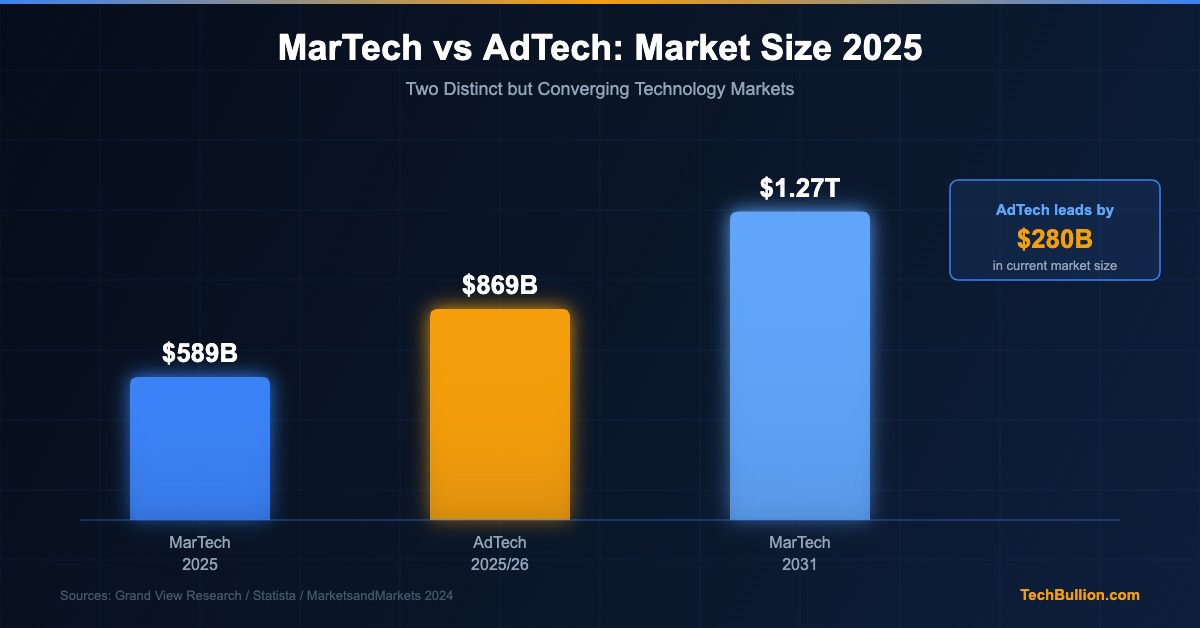

Two of the most consequential technology sectors in modern business are marketing technology (MarTech) and advertising technology (AdTech). Though they are frequently discussed in the same breath, they represent distinct markets, serve different functions, and operate on different commercial models. In 2025, the global MarTech market stands at approximately $589 billion, while the AdTech market is valued at around $869 billion. Understanding the difference between them – and why it matters – is essential for any business navigating the modern digital economy.

Defining the Two Markets

MarTech refers to the software and tools that marketing teams use to plan, execute, manage, and measure their marketing activities. It encompasses a vast range of capabilities including customer relationship management (CRM), email automation, content management, social media scheduling, analytics platforms, and customer data platforms (CDPs). The defining characteristic of MarTech is that it supports the internal operations of a marketing organisation.

AdTech, by contrast, is the infrastructure that enables the buying and selling of advertising at scale. It includes demand-side platforms (DSPs), supply-side platforms (SSPs), ad exchanges, data management platforms (DMPs), and programmatic advertising systems. AdTech sits between advertisers and publishers, facilitating the automated trading of digital ad inventory across display, video, mobile, and connected television channels.

According to Grand View Research, the global MarTech market was valued at $589.14 billion in 2025, with projections pointing to a compound annual growth rate of around 19.9 percent through 2034. The AdTech market, as estimated by MarketsandMarkets and other analysts, is currently valued at approximately $869 billion, making it the larger of the two markets in absolute terms for the current period.

Why AdTech Currently Leads on Market Size

The size disparity between AdTech and MarTech comes down to the sheer volume of money flowing through programmatic advertising channels. Global digital advertising spend exceeded $600 billion in 2024, according to Statista, with the majority routed through automated AdTech systems. Every impression traded, every bid placed, and every ad served runs through an AdTech stack. The sheer transactional volume creates enormous market value.

MarTech, while growing rapidly, tends to be software-as-a-service based and measured by subscription revenues and platform fees rather than the pass-through economics of advertising spend. This means that even though MarTech underpins the strategy and execution of marketing at thousands of companies, its revenue footprint is structurally smaller than AdTech’s at this stage.

However, the gap is closing. The MarTech market is projected to reach $1.27 trillion by 2031, a trajectory that will eventually surpass AdTech valuations if growth rates are sustained. The 19.9 percent CAGR driving MarTech reflects the accelerating enterprise investment in owned marketing infrastructure.

The Operational Distinction

Perhaps the clearest way to understand the difference between the two markets is through their relationship to customer data and media. MarTech primarily works with first-party data – the toolset brands use to understand and communicate with their own customers. A company’s CRM system, its email marketing platform, its website analytics: these are all MarTech tools operating on data the brand itself has collected with customer consent.

AdTech traditionally relies heavily on third-party data and cookie-based tracking to serve targeted advertisements to audiences across the open web. This model is undergoing significant disruption as a result of browser-level privacy changes, the deprecation of third-party cookies, and tightening data protection regulation in markets including Europe and California.

This regulatory pressure is one reason why MarTech is growing faster than AdTech at a percentage level. As brands are forced to reduce their reliance on third-party data, investment in first-party data infrastructure – squarely within the MarTech domain – becomes a strategic priority. The 15,000-plus tool MarTech ecosystem reflects the breadth of investment in this direction.

Convergence and Overlap

The boundaries between MarTech and AdTech are increasingly blurring. Large platform businesses such as Google, Meta, and Amazon operate technology stacks that span both categories. This convergence is producing a new category sometimes referred to as MadTech, shorthand for the integration of marketing and advertising technology into unified platforms. According to research from the Interactive Advertising Bureau, more than 60 percent of enterprise marketers are now actively pursuing integrated MarTech and AdTech stacks rather than maintaining separate vendor relationships.

The rise of AI-driven marketing tools is accelerating this convergence further. Machine learning capabilities that were once exclusive to large AdTech platforms – real-time bidding optimisation, audience segmentation, predictive analytics – are now being embedded directly into MarTech platforms, eroding the historical technological distinction.

Investment Flows and the Enterprise Perspective

From an enterprise investment perspective, the MarTech and AdTech markets attract different types of capital and serve different budget holders. MarTech spending typically sits within the CMO’s direct budget as a capital expenditure on software infrastructure. AdTech spend is largely variable, tied to media budgets, and often managed through agencies or trading desks.

According to Gartner’s CMO Spend Survey, marketing technology accounted for around 26 percent of total marketing budgets in 2024, the largest single budget category. This confirms MarTech as the dominant cost line within marketing operations, separate from and additional to media spend channelled through AdTech. The 80 percent of decision-makers expecting MarTech budget increases signals continued strong enterprise commitment to the owned technology stack.

Regional Dynamics

Both markets are disproportionately concentrated in North America, which accounts for the largest share of global spending in each case. As documented in analysis of the 35.8 percent North American MarTech market share, the region’s dominance reflects the depth of enterprise digital marketing maturity in the United States. Asia Pacific is the fastest-growing region for both markets, driven by the rapid digitalisation of commerce in China, India, and South-East Asia.

The Path to $1 Trillion for MarTech

The future of MarTech through 2034 points clearly towards the $1 trillion milestone. At a 19.9 percent CAGR, the MarTech market is on course to cross that threshold by 2028 to 2029. By 2034, projections suggest a market value exceeding $2.9 trillion, which would comfortably exceed any current AdTech projection by a significant margin.

This trajectory reflects a fundamental shift in how brands think about marketing investment. The era of renting attention through paid advertising is giving way to an era of owning infrastructure for direct customer relationships. MarTech is the technology layer that makes that ownership possible. For businesses evaluating their technology strategy, understanding the distinction between these two markets informs where to allocate budget, which vendors to partner with, and how to structure marketing operations for a world in which first-party data and owned channels become the primary competitive differentiators.

Data from Statista’s digital market outlook shows that global digital spending continues to grow at double-digit rates, with mobile channels accounting for an increasingly dominant share of total transactions.

PwC’s analysis of financial services trends through 2025 highlights the convergence of technology and media as a defining dynamic, with data-driven personalisation becoming the primary competitive differentiator.