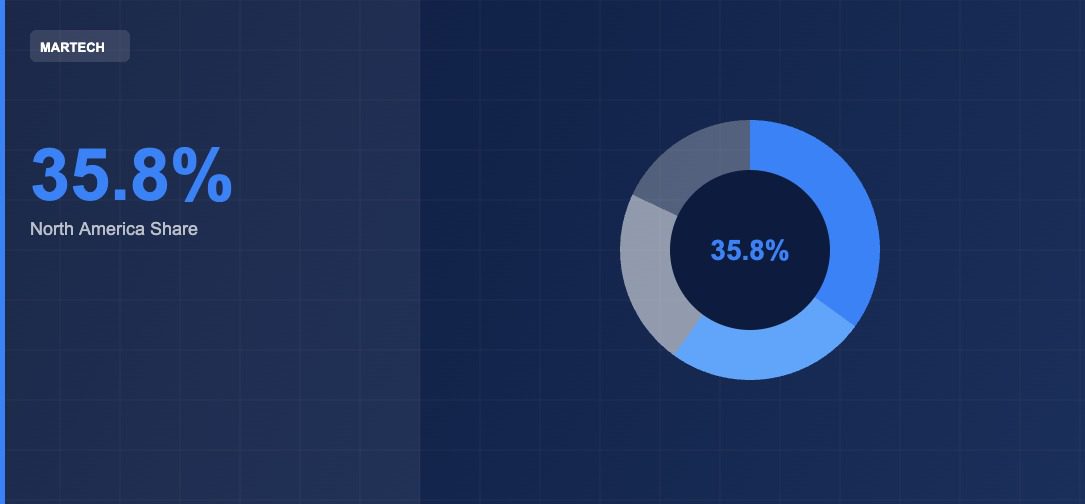

In any global industry, the question of where leadership is concentrated tells you a great deal about where the industry came from and, often, where it is going. North America accounts for more than 35.8 percent of the global MarTech market, according to Grand View Research, making it the dominant region in an industry worth approximately $589.14 billion in 2025. That position of leadership did not emerge from geography alone. It was built through a specific combination of technology infrastructure, capital availability, enterprise sophistication, and market scale that has compounded over more than two decades of digital marketing development.

Understanding why North America holds that position is genuinely useful for any organisation operating in the global MarTech market. It explains where the most influential platforms are built, where the most significant innovation is funded, and where the standards that the rest of the world often adopts are established. It also points to where the most interesting competitive dynamics are playing out as other regions begin to close the gap.

The global MarTech market is projected to grow at a compound annual growth rate of approximately 19.9 percent between 2025 and 2034, according to Grand View Research. North America will remain central to that growth while simultaneously seeing its proportional share shift as Asia-Pacific and other regions expand rapidly from a lower base.

For more coverage on related topics, explore our dedicated section on technology news.

Market analysis from Grand View Research projects that technology-driven market segments will continue expanding at compound annual growth rates between 15 and 25 percent through the end of the decade.

According to Deloitte’s industry outlook, more than 60 percent of large enterprises now allocate dedicated budgets to digital transformation initiatives, up from 35 percent in 2020.

The Foundations of North American MarTech Leadership

North America’s position in the global MarTech market was built on foundations that are structural rather than coincidental. The United States is home to the world’s largest digital advertising market, the highest concentration of enterprise marketing organisations, and a venture capital ecosystem that has consistently identified and funded marketing technology innovation at scale. These three factors are self-reinforcing. Large advertising markets create demand for better tools. Sophisticated enterprise buyers create the commercial environment that allows platforms to grow quickly. Abundant capital allows promising platforms to invest in product development and international expansion before they would otherwise be able to.

The platform leaders that have emerged from this environment are globally significant. Salesforce, headquartered in San Francisco, reported total revenue of approximately $34.9 billion in fiscal year 2024 and operates the world’s most widely adopted CRM platform. Adobe, also headquartered in San Jose, reported Digital Experience segment revenue of approximately $5.3 billion in fiscal year 2024, according to the company’s annual report. HubSpot, based in Cambridge, Massachusetts, reported full-year 2024 revenue of approximately $2.6 billion with over 230,000 customers worldwide, according to its investor relations filings. These companies did not simply grow in North America. They defined categories, established integration standards, and created the ecosystem frameworks within which thousands of other MarTech products operate globally.

The AppExchange ecosystem built by Salesforce, the integration marketplace built around Adobe’s Experience Cloud, and the HubSpot App Marketplace are each examples of how North American platform leaders have created network effects that extend their influence well beyond their own products. Every third-party tool that integrates with these platforms reinforces the centrality of the North American platforms to the global ecosystem.

How Artificial Intelligence Is Extending North American MarTech Dominance

The emergence of enterprise artificial intelligence as a core component of marketing technology has, at least in the short term, further concentrated innovation in North America. The major AI research organisations, the largest foundation model providers, and the most significant AI infrastructure companies are predominantly headquartered in the United States. That proximity creates advantages for North American MarTech platforms in accessing, integrating, and commercialising AI capabilities.

Salesforce’s Agentforce, launched in late 2024, generated more than 1,000 deals within weeks according to CEO Marc Benioff’s public commentary, demonstrating how quickly enterprise AI marketing capabilities can reach commercial scale when built on established platform infrastructure. Adobe’s Firefly generative AI models surpassed 6.5 billion generated images by early 2024, according to an Adobe press release, with the technology integrated throughout the Experience Cloud suite that enterprise marketers globally use daily. HubSpot’s Breeze AI suite, launched in 2024, extended AI capabilities to content creation and marketing automation for its global customer base, according to the company’s 2024 investor relations filings.

McKinsey’s Global Institute estimated that marketing and sales represent the business function with the highest potential value from generative AI, identifying between $0.8 trillion and $1.2 trillion in annual value creation across industries, according to its 2023 report The Economic Potential of Generative AI. The North American platforms best positioned to capture that value are the ones already embedded in the marketing operations of the world’s largest organisations.

Europe’s Distinct Approach and Its Influence on the Global Market

Europe represents the second-largest MarTech market globally, and its approach to marketing technology is meaningfully different from North America’s in ways that have influenced the entire industry. The European Union’s General Data Protection Regulation created a regulatory environment that has driven significant investment in consent management platforms, privacy-compliant data infrastructure, and first-party data strategies. Rather than constraining the European MarTech market, this regulatory pressure has generated an entire category of compliance-driven marketing technology that is now considered best practice globally.

European enterprise marketing organisations have, in many cases, built more sophisticated first-party data infrastructure than their North American counterparts, precisely because the regulatory environment required it earlier. The privacy-first approach to marketing data that is increasingly necessary everywhere was pioneered, in large part, by European compliance requirements. This has positioned European marketing organisations well for the privacy-first era that Apple’s App Tracking Transparency framework and Google’s cookie deprecation work have accelerated across all markets.

Asia-Pacific’s Rapid Expansion and What It Means for Global Share

Asia-Pacific is the fastest-growing region in the global MarTech market, according to Grand View Research. The region’s growth is driven by a combination of rapidly expanding digital consumer populations, rising enterprise marketing sophistication, and the emergence of regionally significant MarTech platforms that address the specific needs of Asian markets.

India has produced globally recognised marketing technology platforms including MoEngage and CleverTap, both of which have successfully expanded into international markets. MoEngage, founded in Bangalore, serves customers across Asia, the Middle East, Europe, and the Americas with a mobile-first customer engagement platform. CleverTap, similarly founded in India, has built a global presence in mobile marketing automation. These companies demonstrate that world-class marketing technology is being built and scaled from outside North America and that the competitive landscape of the global MarTech market is genuinely global.

Southeast Asia represents significant upside. Indonesia, Vietnam, Thailand, and the Philippines are all experiencing rapid growth in digital commerce and mobile internet adoption. The marketing technology platforms most relevant to these markets differ in meaningful ways from those designed for North American enterprise buyers, which has created space for regionally focused innovation that will add to the global ecosystem count and the global market value simultaneously.

What North America’s Market Leadership Means for Global MarTech Strategy

For organisations anywhere in the world building or procuring marketing technology, North America’s 35.8 percent market share has practical implications. The standards that North American platforms set tend to become global standards. The integration protocols that North American platforms support tend to become the ones that third-party vendors prioritise. The AI capabilities that North American platforms commercialise first tend to become the expectations that marketing organisations in other regions develop over the subsequent two to three years.

This does not mean that global organisations should simply adopt North American platforms wholesale. It means that understanding the North American MarTech landscape, including where it is innovating, what problems it is solving, and where it has limitations, is useful market intelligence for any organisation building a serious marketing technology capability.

Approximately 80 percent of marketing technology decision-makers globally expect their budgets to increase over the next three to five years, according to McKinsey research published in 2024. The $589 billion global market that is growing toward $1.27 trillion by 2031 will continue to be shaped in important ways by North American innovation. The organisations that understand that dynamic are better equipped to navigate the landscape, wherever they are based and wherever their customers are.

North American Leadership Will Evolve but Not Disappear

North America’s 35.8 percent share of the global MarTech market will likely decline proportionally as Asia-Pacific and other regions grow faster from a lower base. That is a mathematical consequence of differential growth rates, not a sign of weakness. The absolute size of the North American MarTech market will continue to grow significantly even as other regions grow faster. North American platform leaders will continue to invest in AI, expand internationally, and set the integration and data standards that define how the global ecosystem operates.

The more interesting evolution to watch is whether the next generation of globally significant MarTech platforms emerges from outside North America. The evidence from India, and the early signals from Southeast Asia and Latin America, suggests that it will. The global MarTech landscape of 2031 will be more distributed in its innovation geography than the landscape of 2025. That broader distribution of innovation is a sign of a market maturing in the healthiest possible way, with more participants, more diversity of approach, and more value created for marketing organisations around the world.