In the fast-paced world of global tech and business, the conversation often revolves around disruption, scalability, and risk. However, recent volatility in the global job market—marked by layoffs in major tech sectors and the rise of the gig economy—has shifted the focus back to a fundamental concept: financial security.

While Silicon Valley champions the “move fast and break things” ethos, the Nordic region, specifically Denmark, has championed a different approach known as “Flexicurity.” This model combines the flexibility of a dynamic labor market with the security of a robust social safety net. At the heart of this system lies the unique concept of the “A-kasse” (Unemployment Insurance Fund).

As the insurance and financial sectors undergo digital transformation, understanding how these traditional safety nets are being modernized and made accessible through digital platforms is crucial for modern workforce planning.

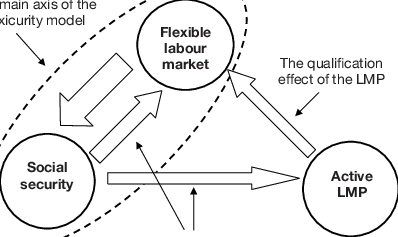

Understanding the Flexicurity Model

To understand the Danish insurance landscape, one must first understand the macroeconomic environment. Denmark consistently ranks among the best countries for business, largely due to its Flexicurity model.

- Flexibility:Employers can hire and fire relatively easily, allowing businesses to adapt quickly to market changes without being bogged down by heavy litigation or excessive redundancy costs.

- Security:Employees are protected not by job guarantees, but by a state-supported, member-based insurance system that provides a high level of income compensation if they lose their jobs.

- Active Labor Market Policy:There is a strong focus on retraining and education to get unemployed individuals back into the workforce.

This triad creates a dynamic economy where risk-taking is encouraged because the personal cost of failure is mitigated. For the fintech and startup sectors, this is an ideal ecosystem.

The Unique Role of the “A-kasse”

Unlike many other countries where unemployment insurance is solely a government tax-funded affair, the Danish system relies on A-kasser (plural for A-kasse). These are private associations, often loosely affiliated with trade unions, though they are legally distinct entities.

Membership is voluntary. If a worker chooses not to pay into an A-kasse, they rely solely on basic social welfare (Kontanthjælp), which is significantly lower and comes with stricter asset limitations.

The A-kasse system is a prime example of a decentralized financial safety net. It requires active participation and financial planning from the individual. However, with over 20 different interdisciplinary and niche-specific funds available, the market can be complex. This is where the intersection of traditional welfare and modern digital tools becomes apparent.

The Digitalization of Insurance Transparency

In the past, selecting an unemployment fund was often a matter of tradition—you joined the fund associated with your specific trade or the one your colleagues used. Today, the landscape is different. The workforce is more fluid; a marketing manager might work in a tech startup today and a heavy industry firm tomorrow.

This fluidity has driven a demand for transparency and digital comparison tools. Much like the Fintech revolution demystified stock trading and banking fees, new digital platforms are demystifying the Danish social safety net.

Consumers are no longer satisfied with opaque fee structures or generic service offerings. They want to compare administrative costs, member benefits (such as legal aid or salary insurance), and Trustpilot scores.

This is where specialized comparison resources have become essential infrastructure. For instance, on platforms like akassefokus.dk, where you can read about Danish A-kasser, users are able to navigate the nuances of these funds. These platforms aggregate data regarding pricing, member satisfaction, and specific eligibility requirements, transforming a complex bureaucratic decision into a streamlined consumer choice.

This shift represents a broader trend in “Insurtech”: the move away from selling insurance through fear and confusion, and toward selling it through clarity and data empowerment.

Why Financial Literacy Matters for the Modern Workforce

For expats, remote workers, and international businesses operating in Denmark, understanding this system is vital. The “A-kasse” is not just about unemployment benefits; it is often the gateway to early retirement schemes and supplementary salary insurance.

In a high-tax economy, optimizing which deductible fees you pay and ensuring you are in the correct insurance category is a key part of personal finance.

- Salary Insurance (Lønsikring):Many A-kasser offer supplementary insurance that covers up to 80-90% of your salary. In a volatile tech market, this product is seeing a surge in popularity.

- Legal and Career Support:Beyond the payout, these funds often act as career coaches, providing CV reviews and legal advice regarding employment contracts—services that would cost thousands if purchased privately.

The Future of Safety Nets

As we look toward the future, the Danish model offers valuable lessons. The combination of private administration (via the A-kasse) and public regulation allows for a system that is both human-centric and economically viable.

However, the system relies heavily on digitization to remain efficient. The integration of government databases with private insurance funds allows for seamless payouts and fraud prevention. The next step, currently underway, is the better integration of user-facing platforms that allow consumers to switch, compare, and manage their memberships with the same ease as managing a Netflix subscription.

Conclusion

The narrative of the modern economy is often dominated by algorithms and AI, but the foundation remains human stability. The Danish A-kasse system serves as a fascinating case study in how semi-private institutions can uphold a national economy.

For the consumer, the key lies in utilizing the digital tools available to cut through the noise. Whether through Fintech apps or dedicated comparison portals, the ability to make informed decisions about one’s financial safety net is the ultimate form of security in an unpredictable world.