The Dawn of Unified Payments

In an era where instant gratification is the norm and digital experiences define customer expectations, financial institutions face unprecedented pressure to evolve their payment infrastructure. Traditionally, high-value payments have operated on separate, distinct rails: Wire transfers, the long-standing workhorse for interbank and large corporate transactions, and Real-Time Payments (RTP), a more recent innovation enabling instant settlement and rich data exchange.

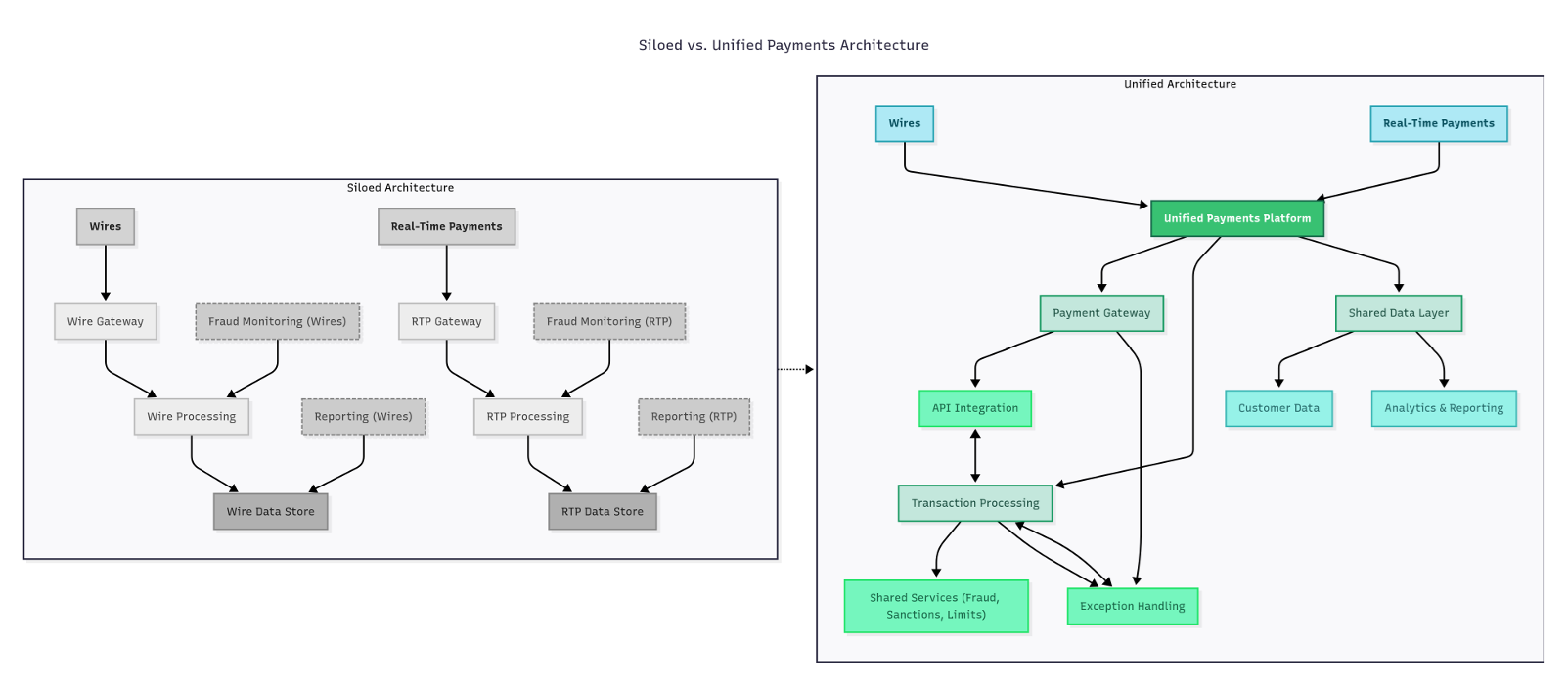

But the fragmented, siloed approach of the past is no longer sustainable. With the accelerating pace of digital commerce and increasing regulatory scrutiny, banks are now exploring a transformative path: building unified platforms that seamlessly support both wires and RTP. This shift isn’t just about efficiency; it’s about unlocking new levels of agility, resilience, and customer-centric innovation. This article outlines a modern, platform-centric approach to designing such an infrastructure, drawing insights from real-world modernization efforts across the industry.

Why a Unified Platform Now? The Imperative for Change

Imagine managing two separate kitchens for different types of meals – one for quick snacks and another for elaborate dinners. While both serve food, their distinct operations, equipment, and workflows lead to duplication, higher costs, and often, slower service. This mirrors the challenge faced by many financial institutions today:

Challenges of the Siloed Status Quo:

- Operational Inefficiencies: Wires and RTP often run on disparate, legacy systems, leading to duplicated efforts in reconciliation, fraud monitoring, and reporting. This results in higher operational costs and manual interventions.

- Rigid Architectures: Older systems are notoriously inflexible, hindering rapid innovation and making it difficult to adapt to new payment schemes or evolving customer demands.

- Compliance Complexity & Risk: Maintaining separate regulatory and compliance frameworks for each rail adds immense complexity and increases the risk of inconsistencies or oversights.

- Poor Customer Experience: Fragmented back-end processes can lead to disjointed experiences for customers, who increasingly expect real-time visibility and consistent service across all payment types.

The Strategic Advantages of a Unified Approach:

Adopting a unified payment platform transforms these challenges into strategic advantages. It’s about centralizing the “brain” of payments, enabling:

- Shared Orchestration and Operations: A single system for monitoring, reporting, and routing payments across rails dramatically reduces operational overhead.

- Enhanced Fraud & Risk Management: Centralized services for fraud monitoring, limits management, and sanctions screening provide a holistic view of transactions, leading to more robust and real-time risk detection. A single view of all transactions allows for more sophisticated fraud detection algorithms and real-time intervention, protecting both the bank and its customers.

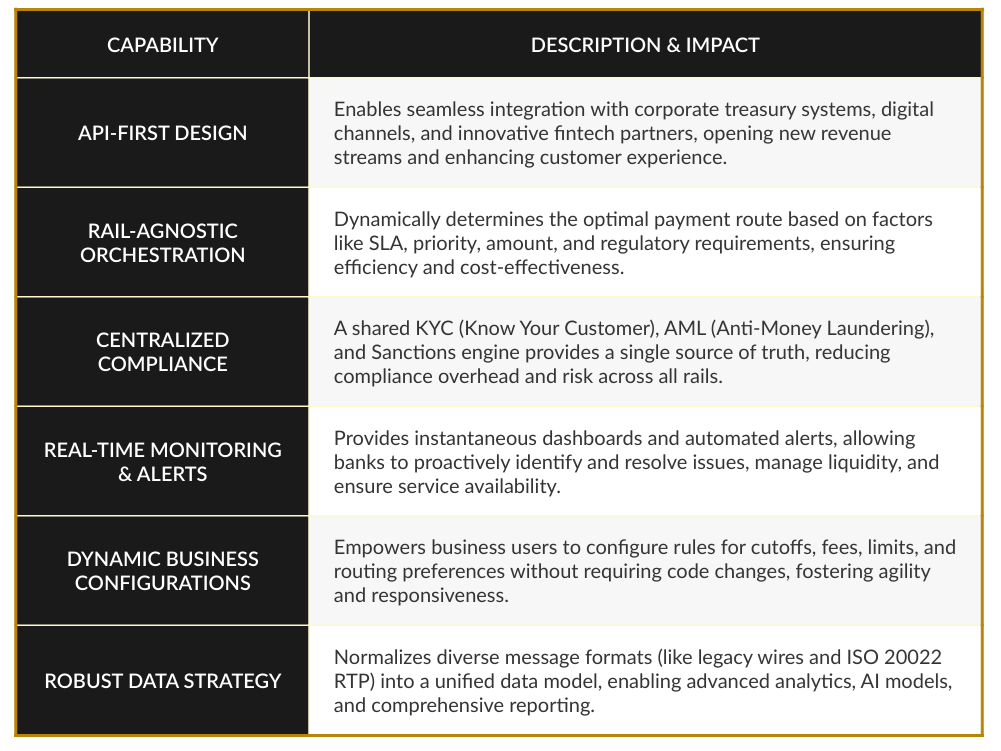

- Faster Innovation & Integration: Easier integration with digital channels, corporate treasury systems, and external fintech partners allows banks to launch new products and services more quickly, opening new revenue streams.

- Simplified Compliance: A single source of truth for compliance reporting and audit trails significantly reduces regulatory burden and risk. With regulators increasingly focused on transparency and efficiency, this is a critical advantage.

- Cost Efficiencies: Consolidating infrastructure, reducing manual processes, and optimizing resource utilization directly translate to significant cost savings. Some financial institutions have reported up to a 20% reduction in operational costs after consolidating payment rails.

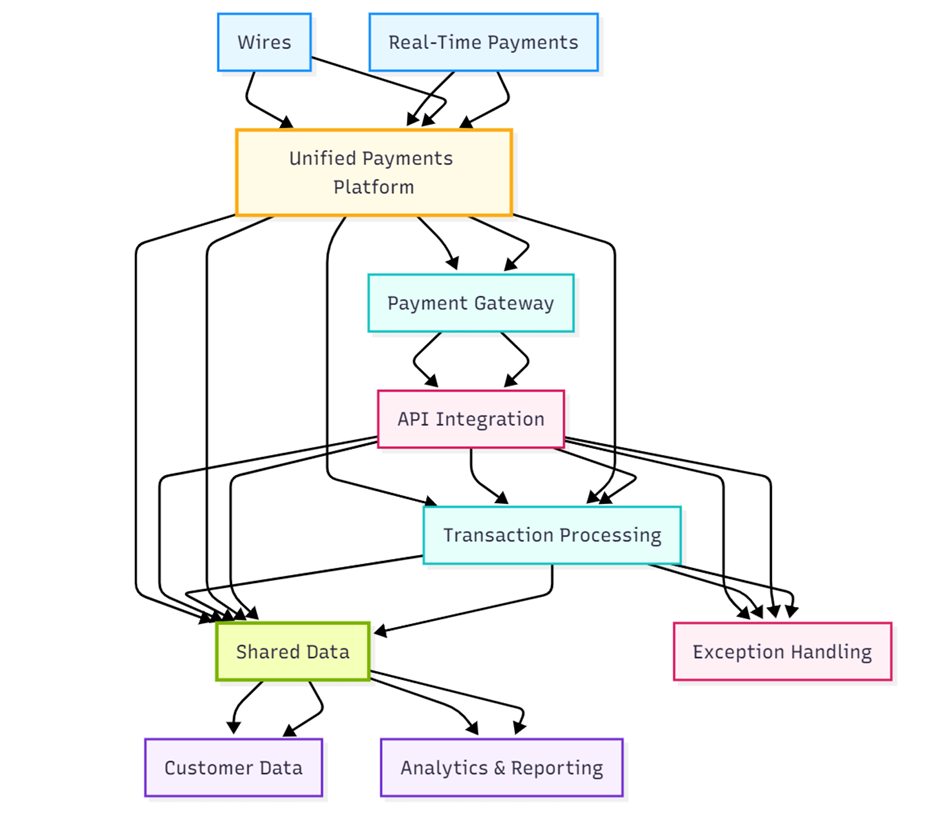

Siloed vs. Unified Payments Architecture

Core Architectural Principles: Building the Foundation

A modern, unified payment platform isn’t just a bigger system; it’s built on fundamental shifts in architectural thinking:

Platform Thinking:

Instead of viewing wires and RTP as standalone applications, they are treated as services exposed via robust APIs. This means the platform is:

- Composable: Built from interchangeable, modular components (e.g., a shared routing engine, a common settlement service). This modularity allows banks to be nimble and adapt to future payment types like FedNow or new ISO 20022 mandates without rebuilding from scratch.

- Extensible: Designed to easily incorporate future payment rails, new regulations, or innovative use cases.

Event-Driven Architecture:

Every significant event in a payment’s lifecycle—from initiation and validation to approval and posting—is captured as a distinct event. This enables:

- Real-time Observability: Instant insights into payment statuses and potential bottlenecks.

- Decoupled Services: Components operate independently, enhancing scalability, resilience, and reducing single points of failure.

Cloud-Ready Infrastructure:

Leveraging cloud capabilities is pivotal for the agility and scalability required for real-time operations:

- Containerized Services: Allows for dynamic scaling up or down based on transaction volumes.

- CI/CD Pipelines: Enables rapid, automated deployment of new features and updates.

- Enhanced Resilience: Distributed architecture across multiple availability zones and regions ensures 24×7 uptime, a critical requirement for RTP.

Key Components of a Modern Payments Platform

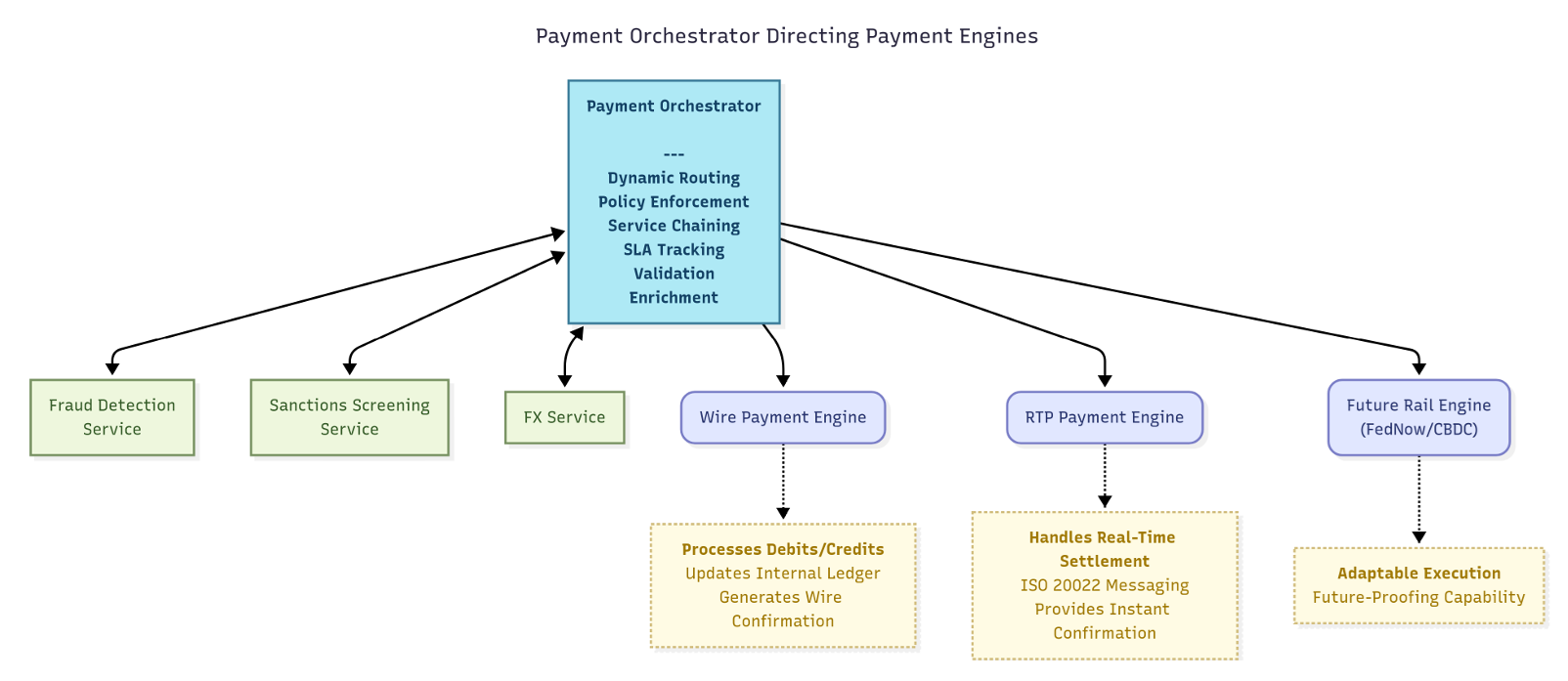

The Brains Behind the Operations: Payment Orchestrator vs. Payment Engine

At the heart of this unified approach lies a sophisticated interplay between two critical yet distinct components: the Payment Orchestrator and the Payment Engine. Though often used interchangeably, they serve very different strategic purposes:

Payment Orchestrator:

Think of the Orchestrator as the conductor of the payment ecosystem. It controls the entire flow of a payment from initiation to final settlement. Its intelligence allows it to make dynamic, real-time decisions:

- Which payment rail is optimal (RTP for speed, Wire for specific cutoffs)?

- When to split or combine payments?

- What compliance rules and business logic to apply?

It performs critical functions like validation, enrichment, intelligent routing, retries, Service Level Agreement (SLA) tracking, and chaining various services (e.g., fraud detection, sanctions screening, foreign exchange).

Payment Engine:

In contrast, the Payment Engine is the instrument – it handles the core execution and settlement for a specific payment rail. It’s tightly coupled with the clearing mechanisms of that rail (e.g., a dedicated wire engine or an RTP engine). Its responsibilities include maintaining ledgers, processing debits and credits, and generating confirmations for its particular payment type.

This distinction is crucial: the Orchestrator provides the strategic oversight and agility, while the Engines handle the operational specifics of each rail, allowing for flexible integration and future-proofing.

Key Capabilities for a Future-Ready Platform

A truly unified payment platform delivers a comprehensive suite of capabilities designed for efficiency, compliance, and innovation:

Navigating the Roadblocks: Challenges and Solutions

While the benefits of a unified platform are clear, the transition is not without its complexities. However, these challenges are surmountable with strategic planning, advanced technology, and strong organizational alignment:

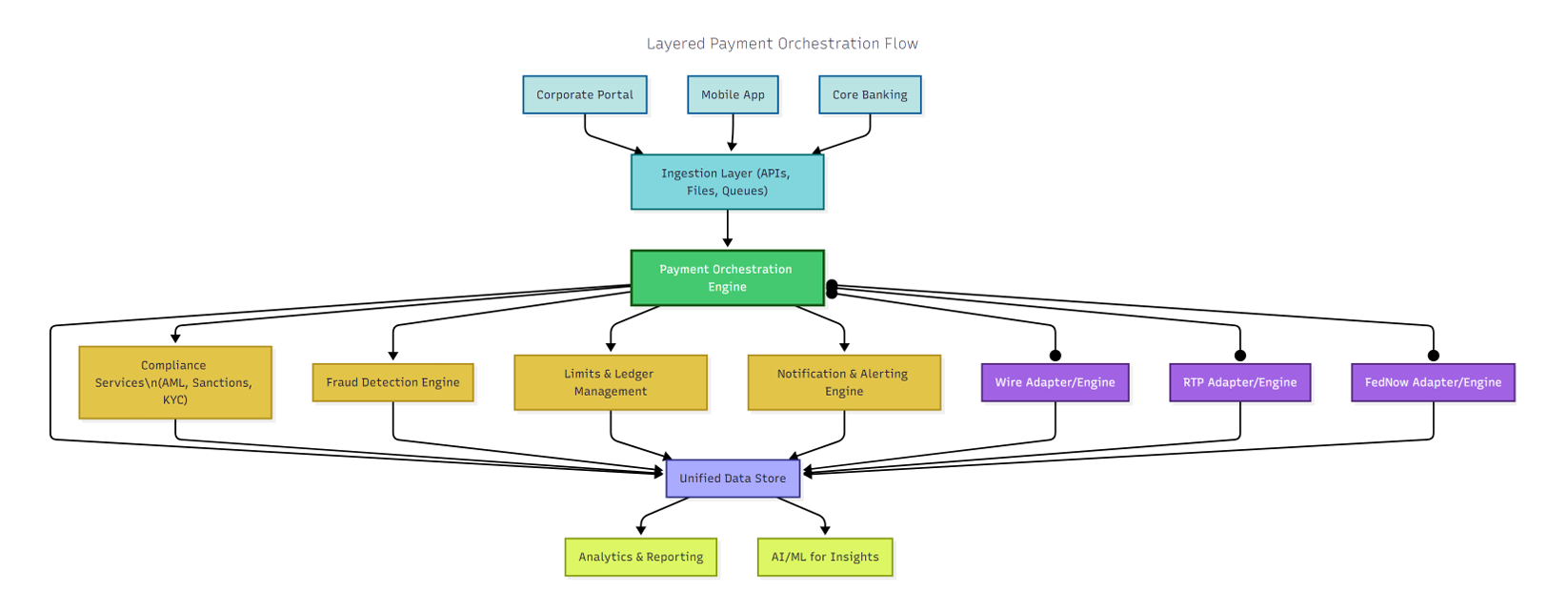

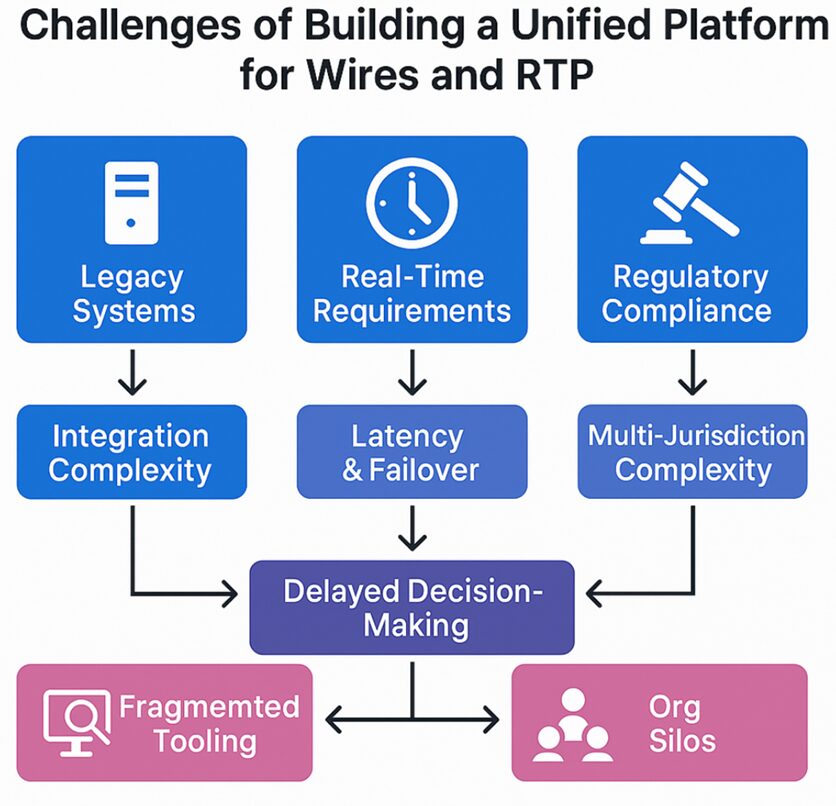

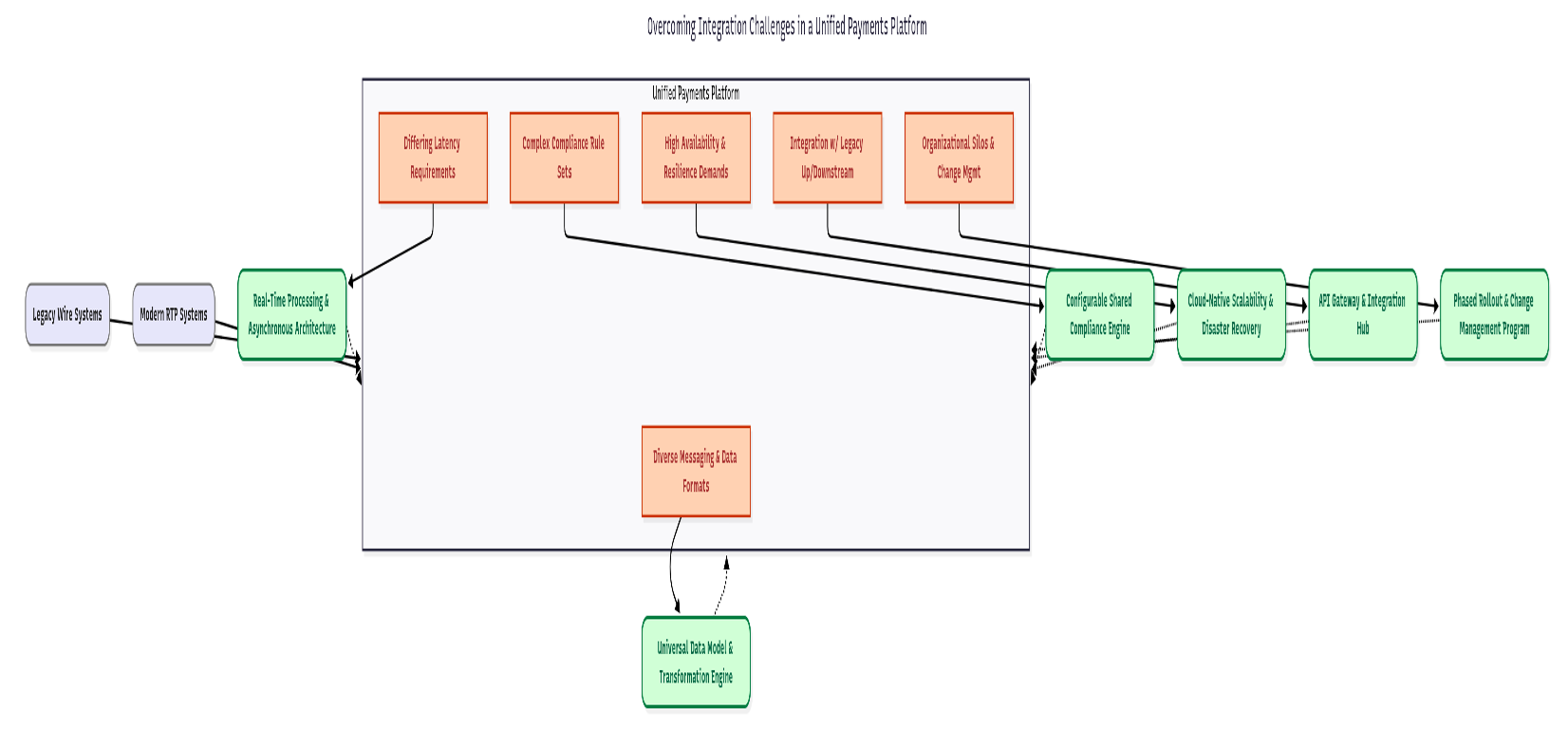

Diverse Message Standards:

Wires typically use legacy formats (e.g., Fedwire, CHIPS), while RTP follows the richer ISO 20022-based structured messaging.

Solution: Requires robust data transformation and normalization layers within the platform to create a common internal data model that gracefully handles both.

Latency Expectations:

RTP demands sub-second processing and response times, whereas wire systems historically tolerate longer durations.

Solution: The unified system must be architected for the stricter RTP standard, utilizing real time processing, asynchronous messaging, and highly scalable cloud-native components.

Compliance Complexity:

RTP and wire transfers have distinct compliance requirements.

Solution: A shared compliance engine must be highly configurable to support different screening cadences, thresholds, and transaction types for each rail, providing a unified yet adaptable framework.

High Availability and Resilience:

24×7 uptime is a must for RTP.

Solution: The unified platform must meet the stricter standard of continuous availability, with active-active architectures, robust disaster recovery plans, and comprehensive resilience testing simulating outages and failed settlements.

Governance and Stakeholder Buy-In:

Merging teams, workflows, and SLAs from different payment rails requires significant cultural and operational transformation within the bank.

Solution: Requires strong executive sponsorship, clear communication, and robust change management programs to align product, operations, compliance, and technology teams.

Integration with Upstream and Downstream Systems:

Treasury portals, fraud systems, general ledger, and customer servicing systems often have wire- or RTP-specific logic that must be re-worked for compatibility.

Solution: An API-first approach and clear integration strategy are essential, allowing for phased migration and co-existence where necessary.

Migration Complexity:

Moving from legacy platforms to a unified system often involves coexistence for an extended period.

Solution: Requires robust reconciliation tools, dual-processing strategies, and a meticulous, phased rollout plan to minimize disruption.

Overcoming Integration Challenges in a Unified Payments Platform

Implementation Considerations: A Path Forward

For financial institutions embarking on this journey, several practical considerations are paramount:

Vendor vs. Build Strategy:

Carefully choose a core engine (whether a commercial vendor solution or an open-source framework) that allows for deep customization and extensibility to meet unique business needs.

Phased Rollout:

Embrace a phased approach to transition from legacy platforms, prioritizing high-impact areas or new payment products first to build momentum and learn. Pilot programs with specific use cases can provide valuable insights.

Talent & Training:

Invest in upskilling internal teams to manage and operate these modern, cloud-native, and API-driven platforms.

Resilience Testing:

Beyond standard testing, rigorously simulate outages across zones, failed settlements, and high-volume stress scenarios to validate the platform’s robustness.

Strategic Change Management:

This is as much an organizational transformation as a technological one. Aligning product, operations, compliance, and technology teams from the outset is crucial for a smooth transition.

Conclusion: A Resilient, Intelligent, and Future Ready Payments Ecosystem

The future of high-value payments lies in breaking down the artificial silos between wire and RTP. By adopting a platform approach—built on modern architectural principles like composability, event-driven processing, and cloud-readiness—banks can unlock unprecedented efficiencies, innovate faster, and meet ever-evolving regulatory and customer demands more effectively.

This journey requires both technical rigor and strategic alignment, but the outcome is transformative: a resilient, intelligent, and future-ready payments platform that positions financial institutions at the forefront of the digital economy. This isn’t merely an infrastructure upgrade; it’s a fundamental shift that empowers banks to offer seamless, real time services, enhancing their competitive edge and fostering a more dynamic and efficient global financial landscape. The time for unified payments is now.

About the Author

Abhishek Gupta is a senior technology leader with over 20 years of industry experience, currently serving as Senior Vice President at Bank of America. He is an expert in wire payments and real-time payment systems, with a strong focus on modernizing legacy infrastructure. Abhishek has successfully led large-scale initiatives such as ISO 20022 adoption, cloud migration, and API-first architecture implementation. His work is dedicated to building scalable, secure, and interoperable platforms that enable the future of digital banking.