In four of the past five years, Bitcoin has been the top-performing asset globally — and often by a wide margin. In 2020, 2023, and 2024 alone, Bitcoin delivered triple-digit returns, helping it rack up a staggering 956% gain over the past five years. Yet one company — Strategy (NASDAQ: MSTR), formerly MicroStrategy — has done just that. Despite Bitcoin’s legendary run, Strategy has quietly outpaced it, delivering a 2,758% return over the same period. In 2025, while Bitcoin has struggled to break out, Strategy stock is already up 20%. That raises a bold question: is Strategy now the better buy?

How Strategy Stock Beat Bitcoin by 3x — and What Happens Next

Until early 2024, Strategy’s stock and Bitcoin moved in lockstep. But then something changed. As Bitcoin ETFs began trading, Strategy started to decouple. Investors were given three clear choices: buy Bitcoin directly, buy it through an ETF, or buy exposure via Strategy — the self-described Bitcoin Treasury Company.

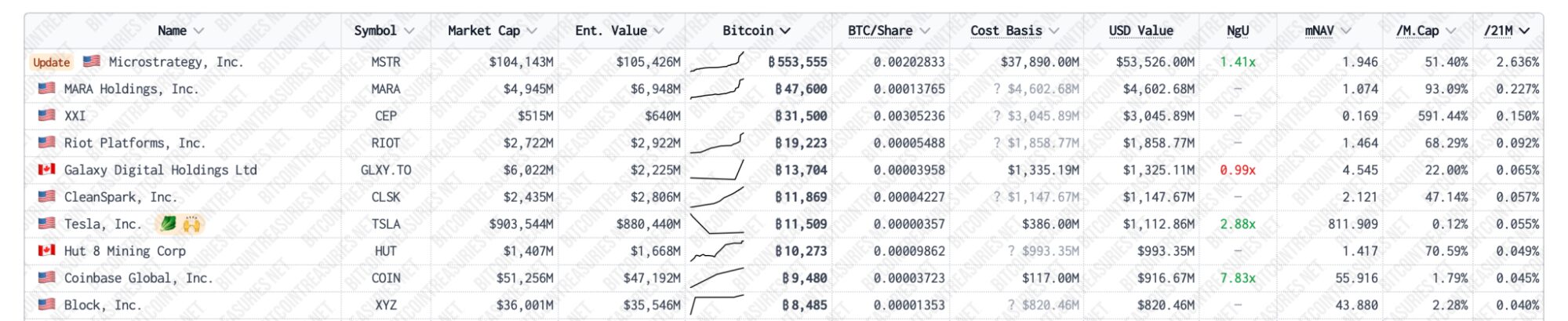

The timing of that divergence is telling. Strategy now holds 553,555 BTC on its balance sheet, worth approximately $52 billion at current prices. That’s more than the US government and far beyond any other corporate holder. The firm’s rebrand from MicroStrategy to “Strategy” in 2025 wasn’t just cosmetic. Its core business now revolves around a single goal: acquiring and holding more Bitcoin. And it’s doing so with unmatched creativity — leveraging debt, equity, and even software revenue to fund its Bitcoin play.

In effect, Strategy has become a proxy for Bitcoin — a stock that mimics BTC price movements while offering the added liquidity, custody, and tax treatment of a US-listed equity. For many investors, this is a feature, not a bug.

So why the premium? If Strategy’s Bitcoin is worth $52 billion, why is the company’s market cap closer to $100 billion?

Part of the answer is that Strategy still technically operates a software business, even if it runs at a loss. That’s non-zero value, and some investors still factor it in. But the larger explanation may be forward-looking. Investors seem to be pricing in significant upside for the company’s Bitcoin holdings — in other words, betting that BTC doubles over the next year. Given Bitcoin’s track record of triple-digit returns, it’s not a wild assumption.

Then there’s Michael Saylor. The company’s founder and executive chairman has become Bitcoin’s most vocal corporate advocate, and his strategic vision — or evangelism, depending on your view — commands investor loyalty. Saylor has consistently found ways to raise capital and acquire more Bitcoin, regardless of price. To some, that’s conviction. To others, it’s risk with a capital R.

There’s a catch, of course. Strategy’s business model works as long as Bitcoin keeps rising — not gradually, but aggressively. If BTC stalls or declines, Strategy risks becoming overleveraged, overpriced, or both. Without a profitable operating business to fall back on, the firm becomes a pure bet on Bitcoin’s continued ascent.

That helps explain why Strategy is actively promoting it. From media appearances to policy advocacy, Saylor’s team is doing everything they can to draw new capital into the Bitcoin ecosystem. Because the more demand there is for BTC, the more justified their $100 billion valuation becomes.

Whether that’s brilliance or bravado depends on your view of the market. But one thing is clear: Strategy is no longer just riding Bitcoin’s coattails. It’s redefining how investors gain exposure to the world’s most volatile — and possibly most valuable — asset.