The way businesses handle payments is changing from year to year. The days when the transaction was just a step in the buying process are gone. Now it’s highly connected with business operations, customer experiences, and financial management. Open Finance and API integration are the twin forces setting the future of payments. These technologies are not only powering efficiency and automation but also unlocking new revenue streams, improving security, and enabling real-time financial decision-making.

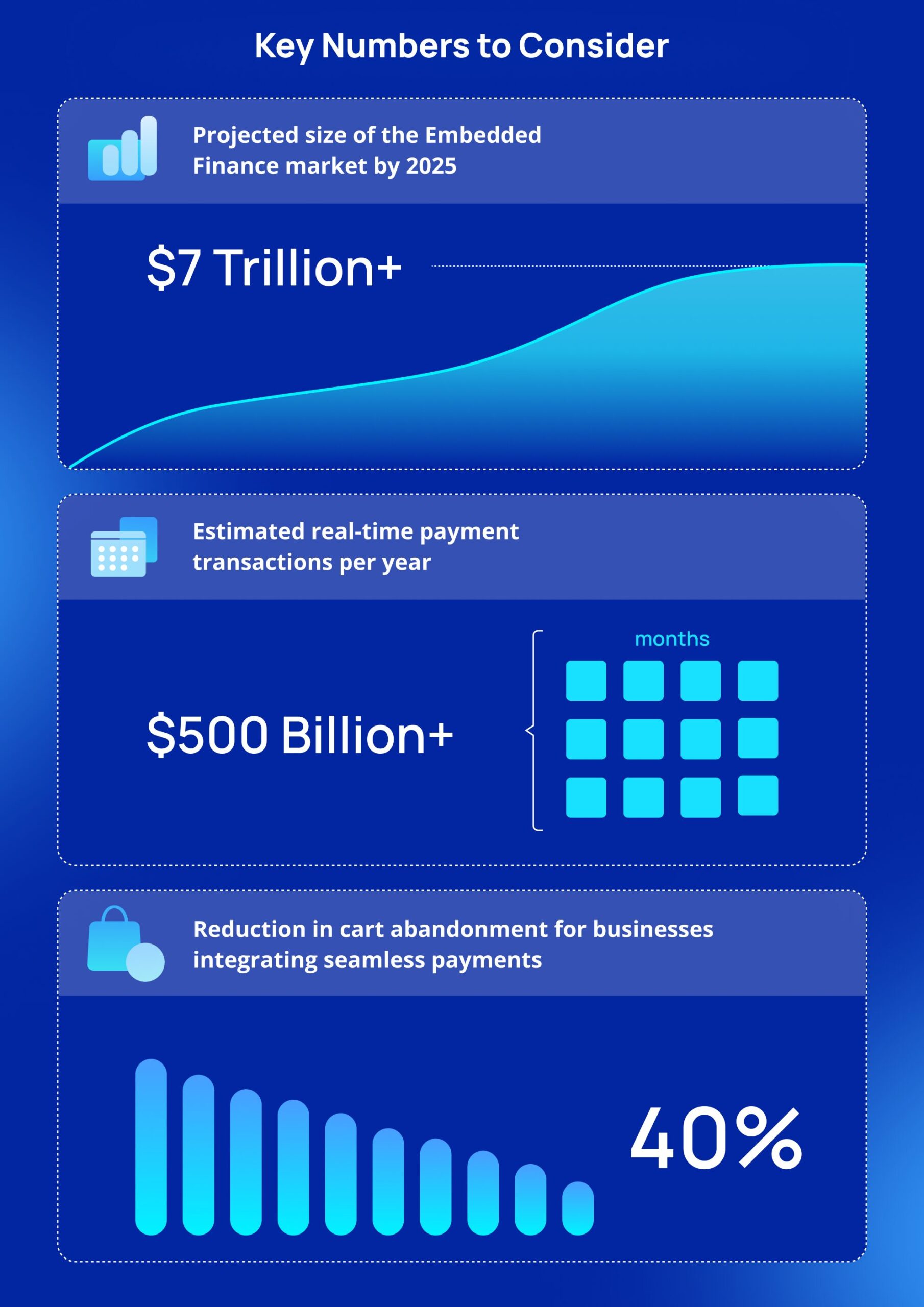

The Open Finance market is expected to reach $150 billion by 2027, with over 500 billion real-time payment transactions annually. Embedded finance, where payments, lending, and financial services are natively embedded into platforms, will process over $7 trillion in transactions by 2026. In this article we will discover what Open Finance is, how API integration works and why our business should focus on them to make the payments work properly and ensure the operational growth.

From Open Banking to Open Finance

The history of Open Finance began with Open Banking, a regulatory mandate that allowed third-party providers to access customers’ banking data with permission and make payments through APIs. Open Banking was restricted, however, it only worked for bank accounts and payments. Now, Open Finance has built upon this concept, opening data-sharing to a broader range of financial services. Consumers and businesses can now connect and share financial data on:

- Payments, including recurring payments and transaction history;

- Lending, with credit scores and loan applications;

- Investments, trading history and portfolio management;

- Insurance, as well as policy information, claims processing;

- Pensions & Retirement Funds with projected payouts, contributions.

This helps businesses to collect a full, real-time view of their financial status, in turn yielding better decisions and frictionless transactions. Rather than making payments, loans, or insurance separate products, companies can integrate these natively into their platforms.

One of the key enablers of Open Finance is API integration. APIs or Application Programming Interfaces are the digital backbone connecting businesses, financial institutions, and fintech services in real time. Standard interfaces allow for secure, real-time data exchange, which makes transactions compliant, reliable, and fast.

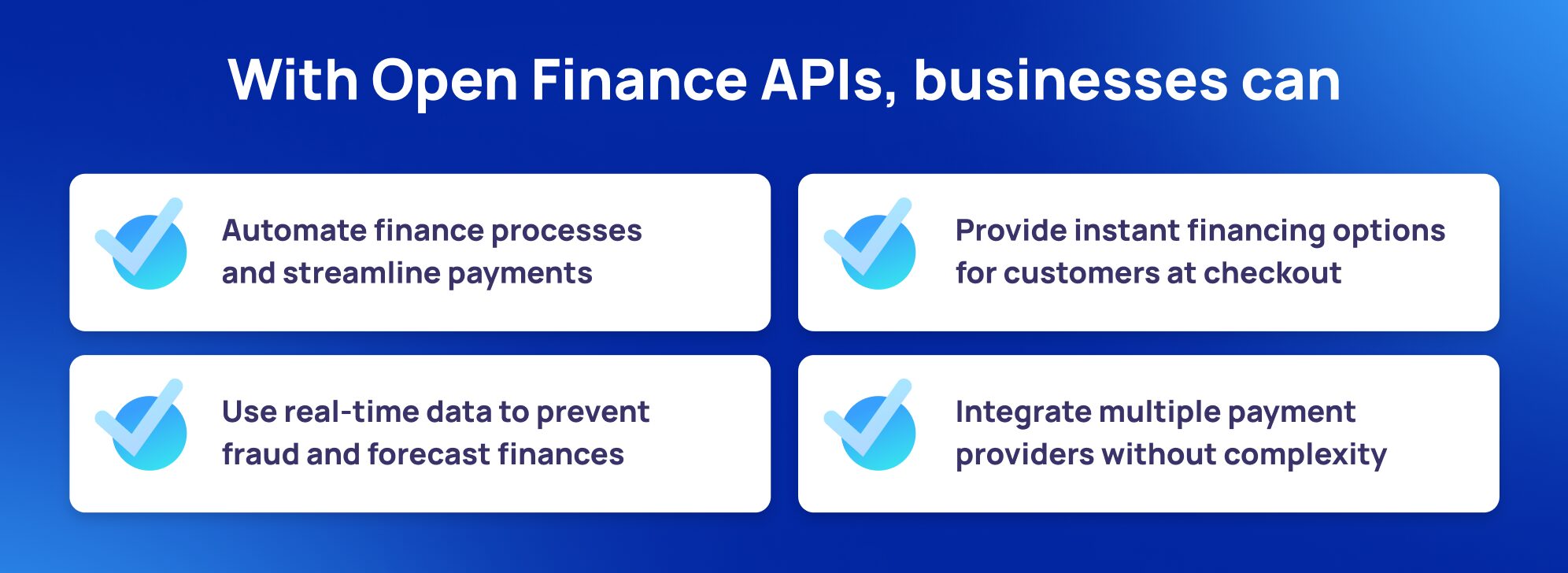

With Open Finance APIs, businesses can:

- Automate finance processes and payments;

- Offer customers instant financing options at checkout;

- Use real-time transactional data for fraud prevention and financial forecasting;

- Integrate with several payment providers without complex integrations.

APIs and Payment Gateways

In the past, a payment integration was a time and resource-consuming process of creating a custom-built link between merchants, banks, and processors. Deferred settlements, lofty transaction fees, and a fractured payment experience were the typical outcomes.

Payment gateways powered by APIs have eliminated these inefficiencies, offering businesses real-time settlements, lower costs, and seamless customer experiences. APIs now enable:

- Real-time payments, with minimal use of costly card networks

- Automated reconciliation, eliminating manual financial reporting errors

- Multi-currency payments, allowing businesses to grow globally without payment limitations

This increases purchasing volume, boosts sales, and improves customer retention. Meanwhile, SaaS vendors can feature automated financing and billing functionality, which enables businesses to forecast cash flow and manage subscriptions efficiently. This automation equals better liquidity management and reduced reliance on manual invoicing.

Open Finance & Business

The combination of Open Finance and API-based payment technologies is changing the way in which businesses operate, process payments, and engage with customers at its very essence. Payment systems are being transformed, from mere minimum business requirements to a method of creating growth, as financial systems go digital and increasingly converge. By 2025, the global embedded finance market is expected to reach over $7 trillion and real-time payment transactions will have risen to over $ 500 billion annually.

Invisible Payments

Payment is being invisibly embedded within platforms, in real-time, and frictionless, requiring as little effort on the user’s part. In-app payment, one-click checkout, or biometric login are some of the ways in which consumers are now expecting seamless financial interactions. For businesses, this shift means higher conversion and customer retention. Businesses that embed payments within their platforms can eliminate friction, streamline the buying process, and lower cart abandonment rates by as much as 40%.

Real-Time Settlements & Multi-Currency Transactions

Real-time settlements powered by APIs enable businesses to be paid in real time, improving cash flow and financial flexibility. It matters especially to cross-border companies, subscription businesses, and gig platforms that rely on immediate access to receipts. In addition, the support of several currencies is not a luxury but a necessity. Instead of cutting into high foreign exchange fees and slow global transfers, companies can use real-time FX rates and direct global transfers via API integrations. This minimises currency conversion risk, saves money, and accelerates cross-border transfers.

Banking-as-a-Service& Payment Monetisation

Open Finance is developing new business models in total. With Banking-as-a-Service, companies can offer their own financial services without having to establish a bank.

With the incorporation of white-label solutions such as payment gateways and digital wallets, businesses can develop new business models and improve interactions with customers. BaaS will grow to more than $70 billion by 2030 with businesses across the spectrum from retail to SaaS leveraging embedded financial products.

Super Apps & API-Driven Financial Ecologies

By bringing together payment, banking, lending, and money management under one seamless experience, super apps foster user stickiness, raise engagement, and capture incremental revenue streams from financials. With more than 50% of mobile phone owners to use super apps for payments as early as 2027, companies that position API-driven financial services are future-proof. For example, a social media platform integrating API-enabled payment, peer-to-peer lending, and financial planning functions can translate user behavior into profit-making financial transactions, reducing dependency on traditional ad income.

Conclusion

By 2025, the businesses embracing Open Finance and API-based payments will be at the advantage. Payments will no longer be a standalone function, but embedded deeply into financial ecosystems, enabling customer experiences that are enriched, costs that are reduced, and new revenues that are attainable. However, many companies are forgetting about one nuance – technical complexity of payments. Here is our tip: having a reliable payment processing partner in this way is a smart strategy to easily integrate, customise and use the full potential of Open Finance features for your business.