Since the beginning of the fourth quarter, the significant increase in Bitcoin has driven a strong rise in the overall crypto market. This wave of hot money pushing up Bitcoin seems to have abandoned the iron rule of “frying the new instead of the old” in the past, and many L1 old brand public chain tokens have rebounded strongly.

As an essential public chain sector in every bull market, veteran public chain tokens have also ushered in spring.

The Spring of Legacy L1 Public Chain Tokens

Ethereum has gradually retreated behind the scenes and started a “rent collection” business. Although in the eyes of most people, L2 will be the main storyline of the new bull market, this does not mean that the old L1 public chains will withdraw from the historical stage. The recent significant rise in a series of L1 tokens seems to indicate that they will also usher in spring.

Source: CoinGecko

Source: CoinGecko

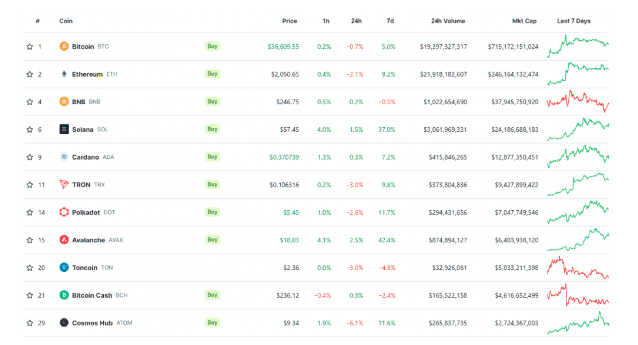

Since the beginning of this year, the most eye-catching increase has been in Solana, the first tier of the public chain in the previous bull market.

Thanks to its strategy of “valuing ecosystem more than technology,” Solana has chosen a more centralized technology solution, relying on a large number of incentive measures to attract numerous developers and users. This year, Solana has emerged from the quagmire of FTX with a dazzling performance of nearly 5-fold increase, and the currency price has reached its highest record in 14 months.

And other “Ethereum assassins” are also unwilling to fall behind. After a six-month period of bottoming out and silence, they have recently started a strong upward trend.

Japan’s established public chain giant ADA has seen a growth rate of over 60% since October, while QTUM and ONT with average ecosystem development also received over 60% growth returns. In the previous bull market, celebrity FLOW and FTM have recorded a growth rate of over 80% in the past month.

The more eye-catching ones are MATIC, NEAR, and AVAX, which have seen a 100% increase in the past month and a half, second only to SOL.

In addition, the long-standing public chain NEO, which had been dormant for a long time, also received over 100% returns due to the Korean hype.

Overfall Rebound or Value Return?

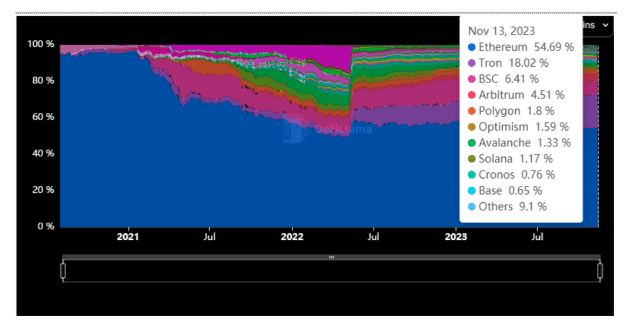

As the oldest public chain project, Ethereum carries most of the ecosystem applications in the current crypto world. According to DefiLlama data, the current TVL on the Ethereum chain reaches $25.258b, accounting for 54.84% of all public links.

But an intriguing trend is that the market share of Ethereum is gradually decreasing. As shown in the figure below, in addition to some L2 filling the squeeze on Ethereum market share, many L1 public chain projects are also experiencing “old trees blooming new flowers.” Is the rise of these public chain tokens due to the overflow effect of Bitcoin funds, or is their potential truly gaining market recognition?

Source: DefiLlama

As the L1 public chain of POS mechanism launched in 2017, Cardano (ADA) has always been known for its unique technical concept, with its consensus algorithm Ouroboros and programming language Hashkell significantly superior to most projects on the same track. Since entering 2023, despite the temporary decline in coin prices, Cardano developers have been improving multi chain solutions such as Hydra Head and Milkomeda C1 side chains.

As of the writing date, Cardano currently has 146 applications and projects running on its network, and the number of projects under construction has climbed to 1280.

Another background that needs to be explained is that one of the biggest technical issues faced by public chains is capacity expansion. Monomer chains attempt to improve performance by adjusting block sizes, but still cannot avoid drawbacks such as on-chain congestion, high gas fees, and excessive centralization. The modularization of the consensus layer is represented by Cosmos’ Tendermint and Polkadot‘s Substrate. The technological development of these modular networks will effectively compensate for the shortcomings of Rollup and provide more imaginative space for ecosystem composability.

Of course, Cosmos will mainly focus on the technology upgrade of IBC in 2022, but there has been no substantial progress in inter chain accounts and security measures, as well as the value capture capability of Cosmos Hub. This will also become an important task for activating the value of its tokens in 2023-2024.

Multi chain networks built on the same development framework and modular tools are still ongoing, such as BNB Chain, Avalanche, and others actively implementing EVM’s L2 solution in the bear market.

The roadmap for the sharding public chain Near, which focuses on wireless scalability, is mainly to release the second sharding protocol Phase2 in 2023 and deliver the third sharding Phase3 in 2024. Currently, there is still a distance from its proposed goal of transitioning from layer1 blockchain to a blockchain operating system.

The old Fantom ecosystem mainly relies on AC’s personal charm and the diversion of ready-made products. After the return of AC, Dapp Gas monetization plan was launched to reduce the FTM destruction rate, and substantial progress was made in virtual machines (FVMs).

Avalanche, which focuses on enterprise collaboration, is also constantly building in the bear market. The official team launched the high-performance virtual machine network HyperSDK this year, released the launch pad AvaCloud for developers to deploy and extend codeless blockchain, and collaborated with multiple Web2 and Web3 institutions, focusing on the metaverse and gaming fields.

Ethereum side chain Polygon is vigorously promoting the Polygon2.0 plan. Polygon 2.0 is actually an upgrade plan announced by Polygon in June this year, which includes four aspects: Polygon PoS upgrade, technology architecture upgrade, token economy update, and governance mechanism upgrade. It aims to become a unified network composed of L2 chains supported by ZK technology. Thanks to its rich technical and practical reserves, Polygon zkEVM has accelerated its adoption and is currently ranked seventh in the ZK solution.

Although the rise of the old brand public chain NEO (GAS) has been hyped by South Korea, its fundamentals themselves are not without merit. Since the NEO team shifted from a single governance mechanism to a strong incentive model, the production and distribution of GAS tokens have become more reasonable; According to its founder Da Hongfei, NEO is also creating a side chain that can resist Miner Extractable Value (MEV) attacks and is compatible with Ethereum Virtual Machines (EVMs). The NEO side chain will be released by the end of 2023.

GateChain is a new generation public chain funded by Gate.io that focuses on user asset security and decentralized transactions. Its innovative online hot insurance account and supporting transaction model design provide secure clearing protection. This chain has continued to implement the mainnet Gas model this year, greatly increasing the value of token GT under the GT fee burning mechanism.

Solana, on the other hand, has begun to return to the audience’s perspective by accelerating technological upgrades and organizing hacking activities. We have already written a separate article on our Blog to discuss it, and we will not go into detail here.

Old Brand Public Chains Are Recovering, But Sustained Development Still Takes Time

In fact, looking back at the past, it is not difficult to find that the reason why the competition in the public chain track is becoming increasingly fierce is that it serves as the infrastructure and underlying demand for the crypto industry.

From 2020 to 2021, various ecosystem sectors such as DeFi, NFT, DAO, Social, and other sectors experienced fluctuations, and the market chain operations were exceptionally active. Due to the huge demand for Ethereum blockspace, many investors and users flocked to the new L1 (Alt L1) with higher capacity and lower costs, which brought huge value enhancement to the L1 public chain at that time.

But as the market turns into a bear market, many established public chains will also reveal their many drawbacks. Entering the bear market of 2022, BNB Chain was deeply questioned about centralization, NEAR’s stablecoin plan was aborted, Avalanche was exposed to a vicious competition scandal, Harmony almost collapsed due to the hacking incident, and Fantom fell to the altar due to the departure of its founder and insufficient ecosystem.

New things always develop and improve in twists and turns. Faced with the constantly approaching Ethereum Rollup “new forces,” the high-performance and low-cost narrative of the old L1 players is clearly no longer tenable. The new L1 public chain is also gradually entering the market, and the existing ecosystem projects are severely homogenized and crowded, requiring new narratives to compete for market share.

In my opinion, in addition to focusing on compatibility with the second layer of Ethereum in technology, the old brand public chain also needs to comprehensively integrate ecosystem resources and marketing capabilities. It can be said that future competition will shift from simple technological optima to unique and differentiated ecosystem circles.

In fact, in the previous round of the bull market, this phenomenon has already begun to emerge, and the vigorous development of many new fields has led to the construction of competitive barriers for vertical public chains targeting segmented fields in the market. For example, Solana launched a revolutionary solution for state compression in the second quarter of this year, which can reduce NFT storage costs by 2400-24000 times. For example, Polymeresh, which specializes in serving compliant asset RWA tracks, has gained a foothold in their respective fields.

Source: POLYMESH

In summary, the logic behind the surge of veteran L1 players is not as simple as the overflow of Bitcoin funds. Their own technology and ecosystem construction also play an important role.

Indeed, each public chain has its own different considerations and choices in the new competitive dimension, and the slightly FOMO market has also given new valuations, but there is not much time left for everyone.

The short-term rise is not the end, and clear direction planning, evolution and upgrading of technical solutions, as well as the construction of ecosystem applications, will increasingly test the comprehensive capabilities of veteran L1 public chains.